We have just held our Annual Investor Conferences in Madrid and Barcelona, with more than 1,750 unitholders attending and 7,000 others streaming the events.

For the third year in a row, I would like to start by thanking our investors on behalf of the entire Cobas Asset Management team. Our sincerest thanks for trusting in, and being a part of, our company. Even if the markets have not yet recognised the value we see in our portfolios and have not, for now, given us the returns we expect.

For those of you who could not come to the recent conferences in Madrid and Barcelona, we would like to give you a brief summary of what we discussed. And if you have the time, I would recommend watching the video on our YouTube channel. In either case, the important thing is for you to take home the basic ideas we sought to convey.

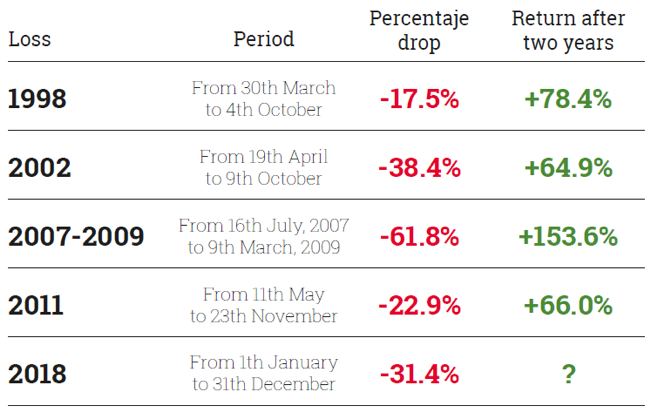

The first message I want to highlight is one of calm, since we have sustained losses this big under other similar situations. Everything that happened in 2018 has happened to us before. Perhaps the previous situation that most resembles this was in 2011, not because of the scale of the decline, which was large, but because of the error in valuation we made in CIR/Cofide, in which 7% of the fund was invested.

We have gone over the sharpest falls in our investments in our more than 30 years of managing investors’ money and we can safely say that after a storm comes a calm. The following table presents the sharpest falls and ensuing recoveries:

The second message I want to convey is one of optimism, even after a challenging year that saw Cobas Asset Management register an extremely negative performance, undermined mainly by two companies, Aryzta (-11.7%) and Teekay (-5.7%). Accordingly, we reviewed our portfolios.

In our international portfolio, the most significant figures are the 138% upside potential of the current net asset value and that it is a portfolio with a P/E ratio of 7.2x.

The portfolio is distributed in five blocks that account for 78% of the securities making up that strategy:

Shipping (25%). Although we had never invested in this sector, it’s where we have the highest concentration. This is because we started by analysing one company, and found that throughout the industry value chain, there were others in which we could invest and we ended up taking positions in 13-14 related companies.

In half of these companies, we made the investment because – although they are now on the downside of the cycle – they all have long-term contracts (13-year average). Therefore, we do not believe we are taking on the risk of the cycle, rather the risk is that counterparties will not pay their contracts, but as we have often said, those counterparties are sound companies.

The other half can be considered companies that have no competitive advantage (like long-term contracts), but where we believe there is a mismatch between supply and demand. As supply and demand begin to even out, these companies’ financial positions will become more attractive.

Commodities (11%). When we speak about commodities, we refer mainly to fertilisers and oil, which are now at their lowest prices of the past 10-15 years. At these prices, no one will increase capacity or operate new mines.

Automotive (11%). We know this sector well because of our investments in the past, and now we are taking advantage of the poor share performance of recent years to re-enter. It is not easy to know the precise reason for this performance, as it is likely due to the economic cycle of the United States, the restructuring of the sector or technology disruption. But we can see that many of these companies have net cash and an upbeat outlook for the future.

United Kingdom (16%). We have taken advantage of falls by the stock market and the pound sterling to enter a market that is now the most discredited among global investors.

Asia (15%). We are extremely fortunate to work with Mingkun Chan, our analyst in Asia (with the assistance of Hwi Soo Cha, our new analyst, since last summer). Being there in person enables us to gain great insight into the Asian part of our companies and, thanks to Mingkun’s more than 10 years of experience working with us, we are ready if an investment opportunity arises.

Of the 12 Asian companies in our portfolio, 11 are family-controlled, and 10 boast a net cash position.

In our Iberian portfolio, the most significant figures are the 85% upside potential of the current net asset value and its P/E ratio of 8.5x.

It should be noted that during the year, we have managed to increase our target value, even with good gains in the portfolio and even though, as noted on many occasions, for us it is more complicated to generate value in Spain and Portugal due to the small number of stocks in the two markets.

Another significant change in the Iberian portfolio is that we have amended the fund prospectus to have the capacity to invest in companies whose assets are in Spain, even if they are not listed here.

In our large company portfolio, the most significant figures are the 83% upside potential of the current net asset value and that it has a P/E ratio of 8.7x.

It has surprised us to be able to find so much upside potential in large companies, as the larger they are, the more difficult it is to find mismatches between price and value, given that they are followed by many analysts.

Many of the stocks are the same as the ones in the international portfolio, but more than 14.5% of the portfolio is invested in three pharmaceutical companies, where some coincide with a major worldwide investor known to all.

Our commitments

We have several commitments to society, and while we spend 99% of our time managing Cobas’ funds, we keep 1% for projects we have spearheaded, and which have now taken on a life of their own.

Our commitment, through Value School, was to spread financial culture. And little by little we are achieving this: they have a community of 50,000 investors, which we hope will increase to 100,000 next year!

Meanwhile, Cobas AM donates a sizeable portion of its income to social benefit work, helping development and impact investing through the Open Value Foundation.

To conclude, I just want to highlight the three key ideas we wish to convey:

- We have suffered sharp falls before, in some cases, like 2011, due to mistakes.

- Experience shows that we have recovered afterwards.

- We believe we have a portfolio with considerable discounts, trading at an average of around 7.2x normalised earnings.

Did you find this useful?

- |