The technological revolution has changed the production model. The economy has moved from agriculture and manufacturing to an industry of intangible assets. Growth companies will be able to grow faster and generate more profits indefinitely. Value investing is dead.

This sounds catastrophic and apocalyptic, but it is what the market has been telling us for the last few years, with the spreads between growth and value companies increasing all the time. So much so that we have experienced the largest historical fall in value stocks relative to growth stocks in the last almost 60 years (-54.8% fall, the second largest being the dotcom bubble in 1998 of -40.6%), and also the most extensive fall in terms of time (13 years and 6 months, almost 4 times longer than the second longest).

We can speak of a two-speed market: On the one hand, sectors to which the bulk of investment has flowed and which trade at very high multiples, and on the other, a group of neglected companies in unpopular or marginalised sectors. In this first group, the greatest exponent is technology companies. In the last 13 years the FANMAGs (Facebook, Apple, Netflix, Microsoft, Amazon and Google) have become so valuable that by mid-2020 they outperformed the market capitalisation of every country in the world except the United States and China.

This narrative rules out that disruptive “new economy” companies will make huge monopoly profits for life, and that the rest of the undervalued “old economy” industries will sink into oblivion and irrelevance. It is clear that some of these “new economy” companies are established, sound businesses with the capacity to generate cash, but there are others, mainly emerging technology companies, that are cash burn machines and their valuations are based on the hope that at some point in the future they will be able to turn losses into profits.

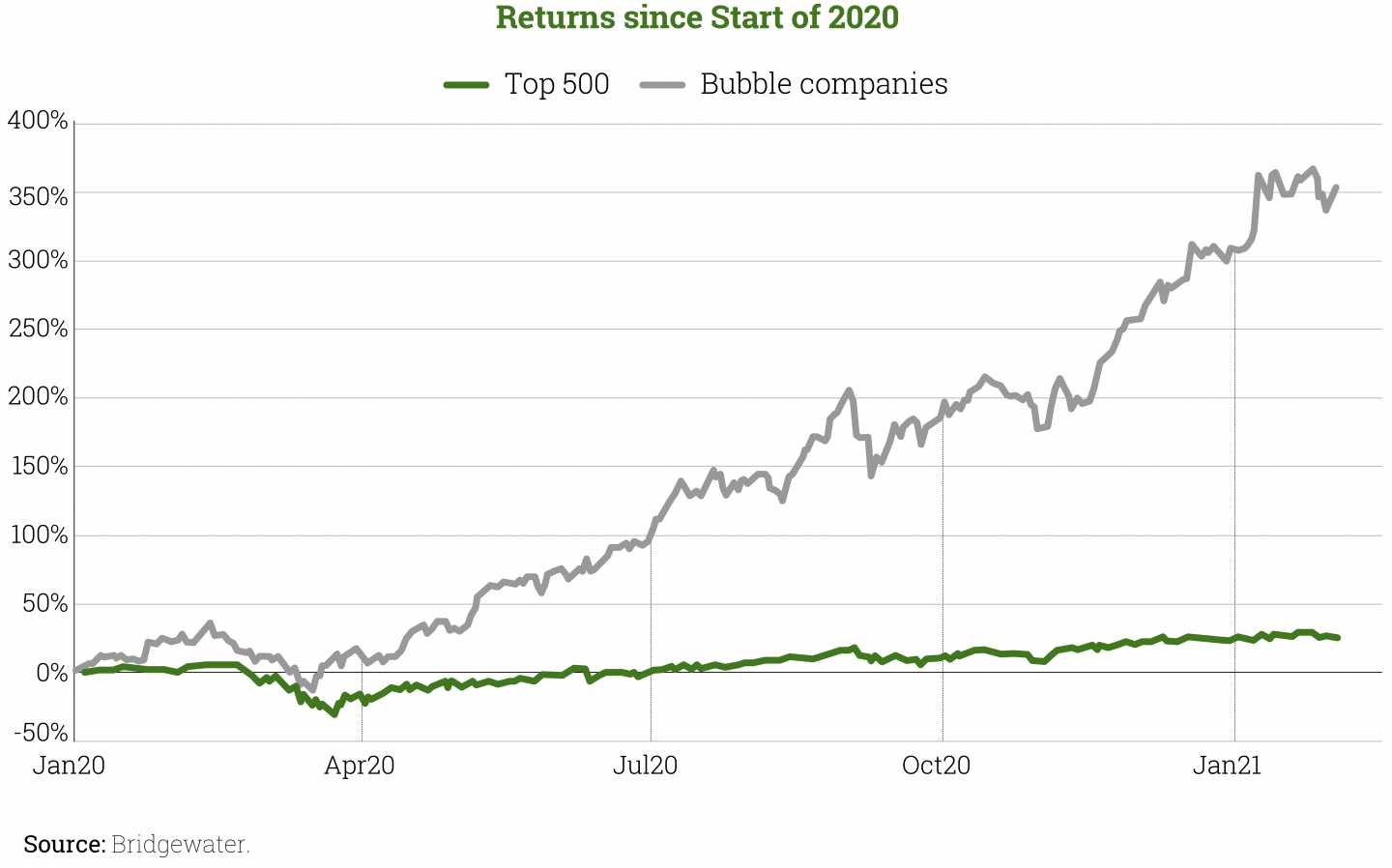

This two-speed market is reminiscent of two market bubbles: To that of the Nifty-Fifty in the early 1970s (You can find more information on the Cobas blog “Are there good and bad stocks?” by Verónica Llera https://www.cobasam.com/es/existen-acciones-buenas-y-acciones-malas/) and the dotcom bubble. The current dispersion can be seen in the following chart from Bridgewater, which shows the return obtained by the companies they classify as being in bubble territory relative to their basket of 500 “top” companies:

As can be seen, the spread between the two over the last year is enormous. Is it possible that in the space of a year the prospects of certain companies can change so much in relation to the rest to justify such a de-correlation? As investors this should set alarm bells ringing. In the current environment of uncertainty and social-political turmoil, being part of this bubble could be disastrous for our wallets. It should be borne in mind that in crisis situations or stressed environments, solvency and profitability become decisive elements for the survival of companies.

The American asset manager Verdad Capital, in its quantitative study How to Maximize Return during Market Panics (Daniel Rasmussen), analyses market crises by asset class since 1970 and concludes that in times of crisis:

- Cheap stocks outperform expensive ones in times of uncertainty.

- The best investment opportunities come from low volume sales by frightened investors.

- Companies that generate net cash, less dependent on the markets, will perform better than those with negative cash flows.

- In terms of leverage, results in the model are dispersed and therefore it can be both good and bad.

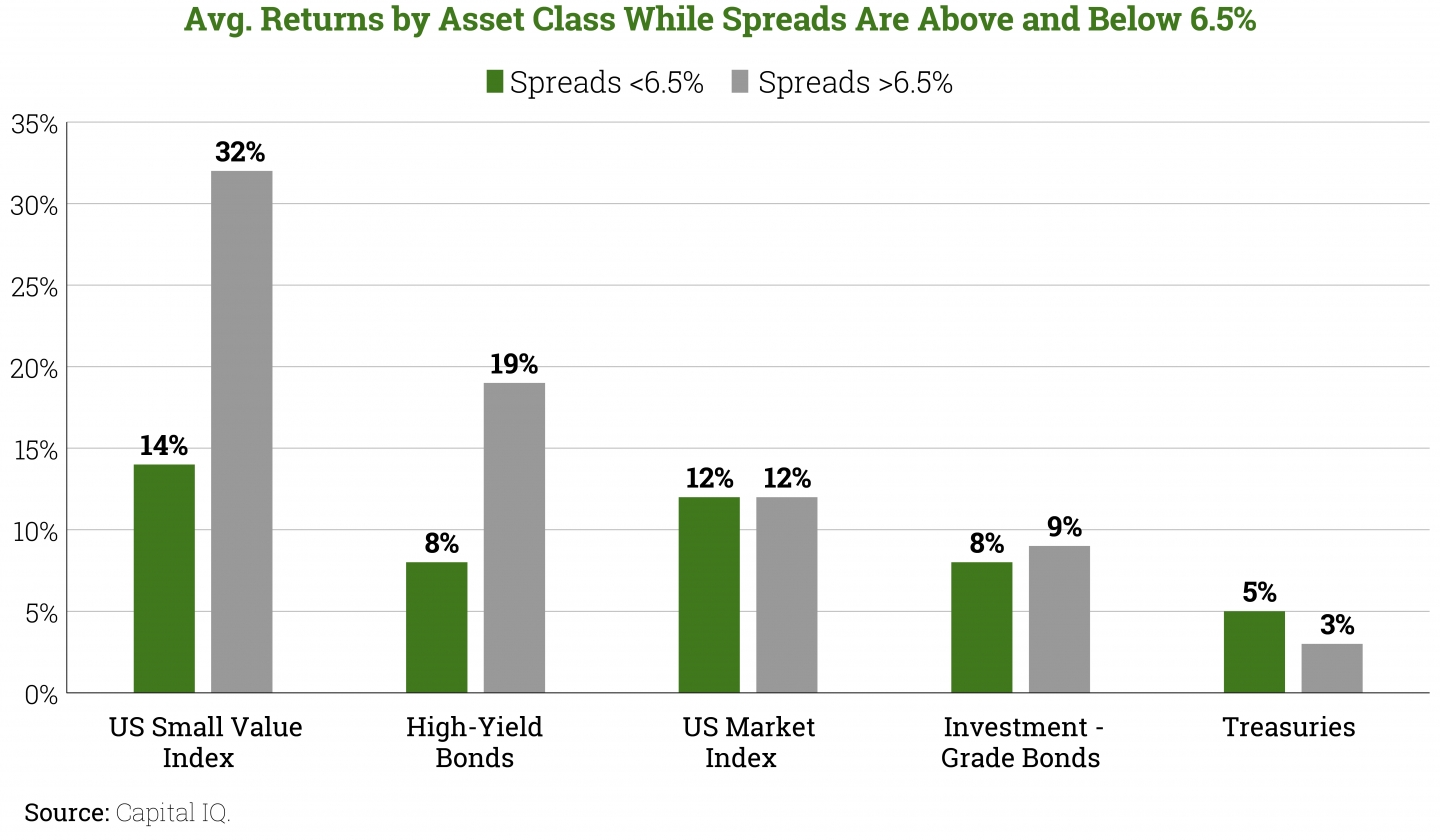

The following graph from the same study compares returns by asset type in two different scenarios: Investing within three months of the spread between high yield bonds and US treasuries exceeding the 6.5% spread (Spread > 6.5%, defined as a crisis period) and in a calm market environment (Spreads > 6.5%)

As can be seen, small-cap value companies not only outperform other assets in normal market conditions, but their returns soar after market corrections. This is because in times of market panic, credit and investment slows, increasing default rates, ultimately causing weak, cash-strapped, investment-intensive companies to suffer or be driven into extinction. Conversely, companies with good businesses and healthy balance sheets are strengthened by this reduced dependence on the capital markets to continue their activity.

Several conclusions can be drawn from this situation analysis:

- Polarisation and bubble creation has happened in the past and will happen in the future. The market is efficient in the long run and eventually adjusts.

- There is a polarised market in which some sectors are very expensive and others very cheap.

- Just because a company is cheap does not mean that the business is bad and vice versa.

- Investing in cheap, cash-generative companies increases the chances of better returns over the long term.

- Historically, after periods of crisis and uncertainty, cheap and cash generative companies outperform other asset classes.

For all these reasons I dare to say that, if buying good businesses at cheap prices is “Value Investing”, it is not that it will never die, but it is arguably the most resilient way to invest.

This past time can be seen as the death of value investing or as the opportunity to access good, cheap deals, which allow us to earn exceptional returns in the future in any market environment. Going against the tide is difficult and the road is sometimes long, but patience pays off.

In the last quarter of 2020 there was a sharp turnaround and for the first time in a long time value companies outperformed growth companies. The spread is still huge, but it may signal the beginning of a market adjustment that will sooner or later have to take place.

Sogyal Rinpoche said that the revolutionary insight of Buddhism is that life and death are in the mind, and nowhere else. So, is “value” dead or has it only died in our minds?

Did you find this useful?

- |