To say that the Spanish public pension system is facing a serious problem is nothing new. The issue has been on the table for Spanish politicians for decades. In fact, in 1985, the first reform was carried out to avoid it from going bankrupt. However, all that has been done since hasn’t been enough to tackle a problem that’s already a reality, and one that’s rarely talked about.

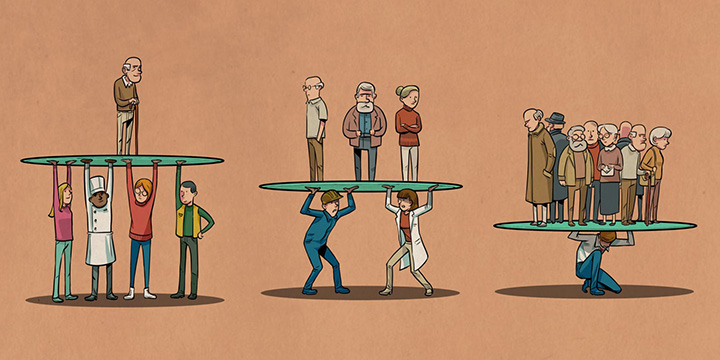

Public pensions in Spain today are unsustainable. Firstly, there are more and more pensioners and the number of workers is not increasing at the same rate, as a result of an inversion of the Spanish population pyramid. Nor does it help that Spain has one of the lowest fertility rates in the world for developed countries, 1.2 children per woman of childbearing age.

And the figures for Spain are undoubtedly worrying to say the least, especially since the number of people of working age is going to fall over the next few decades and the number of pensioners is going to rise. It’s estimated that in 2050 there will be approximately one worker for every pensioner.

I should add that the Spanish welfare system is one of the most generous of all OECD countries: its replacement ratio is one of the highest, at around 70% of the last contributed salary.

But in order to fully understand the existing problem, it’s necessary to know how the public pension system works in Spain. It’s a distributive system, which means that the contributors, i.e. today’s workers, are the ones who pay the pensions of those who have retired. In other words, when a worker contributes, they are not “saving” this money for the future, since this money is used to pay the pensioners in the same month.

The real problem this poses for Spain is that pensions are slowly “eating up” public spending. In fact, over the last decade, spending on pensions has grown by more than 50%, leaving a large hole in the finances of the social security system.

Therefore, faced with this very uncertain situation in which we find ourselves, I dare say that it’s essential to, firstly, make society very aware of this issue and, secondly, for those who haven’t already done so, to start worrying about their own future. In this case, to start saving for retirement, and what better way to accomplish this than by investing in individual pension plans.

But is this financial product really that well known? Do you know what their main characteristics are or what their advantages are?

The first thing that must be clear is that pension plans are an investment vehicle that, thanks to their tax benefits, help the investor to plan their retirement in a complementary way so that they can maintain their purchasing power. It’s not a strange product: In Spain, pension plans have accumulated assets of 111,827 million euros, according to data from Inverco at the end of June.

As is the case with mutual funds, the investor is able to transfer pension plans from one manager to another without being taxed and they have the substantial tax benefit of the investor being able to deduct the annual amount contributed in their tax return.

Of course, the amount of the investor’s deduction will depend on two factors: the annual contribution made and the tax rate it’s subject to. Currently, the maximum legal contribution allowed will be 8,000 euros per year or 30% of net earnings from work and economic activities, whichever is lower, although the current government plans to reduce this amount to 2,000 euros per year. For example, on average, an investor with a marginal rate of 25% will be able to deduct up to 250 euros per year for every 1000 contributed.

In this way, taxes are deferred until the time of redemption. In other words, it will be at that time when all the contributions made and the profits obtained will have to be declared as earned income, charging it to the general tax base and adding it to the rest of the income obtained.

Interestingly, when it comes to redemption, we have to consider which of the three possible ways is best to do so: in the form of capital, income or in a mixed way. In addition, I should mention the special measures in light of the current situation caused by COVID-19, as pension plans may be redeemed in certain circumstances such as being in a legal situation of unemployment as a result of an ERTE (Temporary Redundancy Plan) due to the health crisis, or those employers who own establishments that have been closed to the public, among others.

Although I insist, with good planning, the tax savings gained during the life of the product will give us the possibility to invest more capital and therefore benefit from higher returns in the long term. Especially if we decide to reinvest the tax savings we have gained. In this way, pension plans become a very attractive option to ensure our retirement.

Pension Plans or Mutual Funds?

Initially, it can be difficult to decide which product is more beneficial as an investment saving instrument for the future, a mutual fund or a pension plan, as each individual has different circumstances that will lead them to choose one or the other.

It’s important to understand the different characteristics that each product has, mainly regarding tax, before deciding. And so, we can make the most appropriate decision depending on our personal circumstances. Of course, we at the Cobas Asset Management Investor Relations Team are here to answer any questions you may have.

Although pension plans are products designed for retirement that have good tax benefits, it’s also true that they have some limitations. For example, they can only start to be redeemed after ten years from the initial contribution, unless a specific event occurs, such as serious illness, long-term unemployment, work-related disability or the death of the investor.

However, it’s not often that we see examples of good long-term pension plan management in general. This is at least what the figures show. The average return of this type of product over 20 years is around 2% per year, mainly due to the conservative nature of most investments in fixed income, which also suffer from very high fees for the returns they obtain.

At Cobas Asset Management we stand by our strong belief in equities. There are many times when we’ve stated that it’s the most profitable asset in the long term; believing, as long as the investor’s profile is suitable, that it’s the best way to invest, covering all the long-term investment characteristics and with patience.

With regard to pension plans, at Cobas Asset Management we offer two types with which we try to adjust to the investor’s profile, being faithful to our Value Investing principles: Cobas Global PP, with a 100% Equity portfolio, and Cobas Mixto Global PP, which corresponds to 75% Equity and 25% Fixed Income.

Before my conclusion, I’d like to end with a numerical example of capital obtained at retirement having contributed 8,000 euros per year to a pension plan.

Assuming a retirement age of 67 and investing in Equities with an annual target return of 10%, you would obtain the following capital:

If you’re 30: €2,640,316

If you’re 40: €968,800

If you’re 50: €324,358

It’s therefore clear that the sooner we put our savings to work, the stronger the ripple effect will be.

In short, don’t put off until tomorrow what you can do today. Preparing for our retirement now will give us a lot of peace of mind to deal with our future.

Did you find this useful?

- |