Dear investor,

Coinciding with the publication of the report on the performance of our funds in the second quarter of 2017, we set out below the main characteristics of our portfolio. During this period European stock markets took a respite following the rises seen in the first three months of the year.

International Portfolio

We are struggling to find sufficient quality companies at attractive prices in our natural environment of Europe, meaning that our position in non-European companies is higher than normal. We also have a somewhat greater focus on companies in the commodities business, especially in some sectors with capital needs, such as maritime transport.

Commodity companies have the added advantage of defending the portfolio particularly effectively against the possible negative consequences of central bank monetary manipulation.

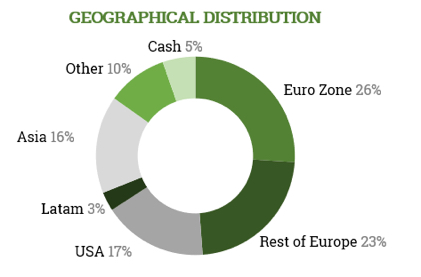

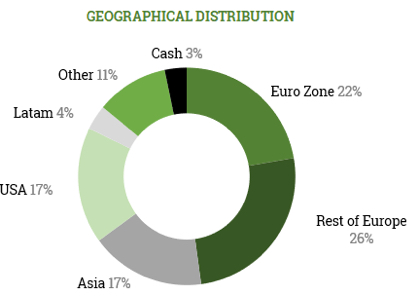

Overall, the geographic distribution of the portfolio has not changed significantly over the quarter, maintaining a strong exposure to companies outside of Europe and the Eurozone.

Dollar hedge

During the first months of the year we suffered an undesirable impact from the depreciation of the dollar and other currencies against the euro. Dollar depreciation against the euro resulted in a loss of 0.8% in the second quarter, while the depreciation of other key currencies (Korean won, Swiss franc and pound Sterling) led to a 1.3% loss.

We were conscious of this risk in January when we took the decision to invest 25% of the portfolio in the dollar area despite the strong currency. The potential upside for stocks in this area compensated the possible currency depreciation.

We were aware of this risk because we know that currency movements remain anchored to Purchasing Power Parity (PPP) over the long-term. The PPP for the dollar/euro is around 1.25-1.30 which serves as a magnet; currencies tend not to stray from this range for long periods.

This is why at the start of the year, in light of the attractive opportunities in the dollar area, we decided to hedge this risk. This decision was made on the basis of three unusual circumstances:

- A very high portfolio exposure to the dollar without a natural hedge (i.e. when a company benefits from currency depreciation), with businesses – such as maritime transport – denominated in dollars.

- The dollar was at a 15-year high in January, at 1.05 against the euro.

- Relatively affordable hedging costs thanks to the low interest rate environment.

We first hedged the dollar back in 1999 when it was trading at parity with the euro and at the time we also had very significant positions in this currency. But the regulator demanded we implement control measures which were not in our possession and we were forced to unwind the hedge, with clients bearing the brunt of the depreciation in the following years.

We are currently in a similar position, with a significant dollar investment in companies without a natural hedge. Unfortunately, due to technical/legal reasons we were only able to set up the hedges at the end of May, suffering a 1.3% loss as the dollar fell from 1.05 on 1 January to 1.11.

This is ultimately an exceptional situation for us and the hedge will end once we reduce our exposure to the dollar or when it closes in on its PPP anchor; meanwhile, the exposure remains covered.

However, it is not our intention to cover investments in other currencies.

Our exposure to the Swiss franc and Korean won relate to global companies with a natural hedge, who stand to gain from a depreciation of their currencies. Meanwhile the British pound might be somewhat undervalued in PPP terms relative to the Euro, making it unreasonable to assume the cost of hedging, especially as it is close to a 30-year low.

The remaining currencies have a low weight, which is why we will not be hedging them.

Iberian Portfolio

The Iberian portfolio includes some new stocks for us, various of which are focused on the Spanish real estate sector. It is a welcome development after many years with a bearish outlook to be able to be optimistic regarding the economic and real estate cycle in Spain, which is why we have invested in some companies well placed to make the most of it.

The strong increase in the value of the portfolio over this period limits the portfolio’s potential. We now see upside of 30%, which is historically towards the lower end and tends not to be accompanied by large upward movements.

It goes without saying that we will keep working to increase this upside with new ideas or making the most of market movements. As an example of this, in July we have invested in a company which has suffered a 40% fall in recent months making it worthy of our interest. We hope that similar opportunities will arise.

Our Funds

Cobas Selección F.I.

The fund posted a negative return of -2.24% over the quarter, compared to a 0.68% increase in the benchmark MSCI Europe Net Total Return index.

Assets under management to 30 June amounted to 720.2 million euros, reaching a total of 8,582 shareholders.

Our target value for the Cobas Selección fund is well above its current net asset value of €102.18, with potential upside of over 70%. We have continued to increase the value of the portfolio over the quarter and we expect that this will be reflected over time in its net asset value.

Portfolio

The Cobas Selección fund is our model portfolio, around 90% is invested in the international portfolio and 10% in the Iberian portfolio.

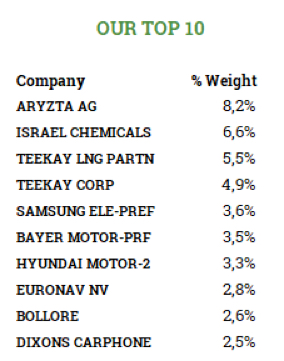

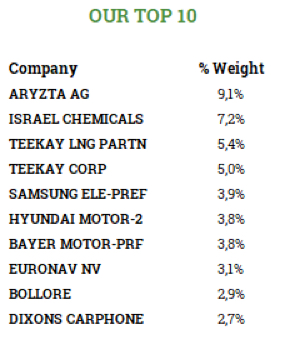

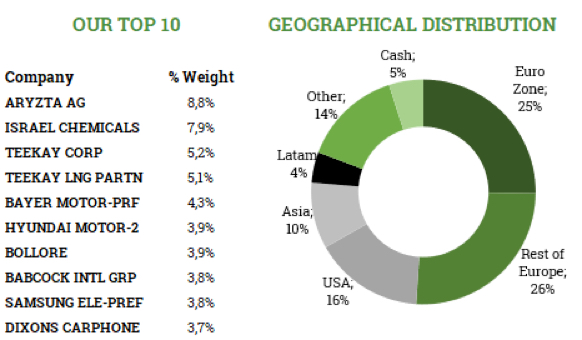

The weights of the main stocks have not changed significantly, with Aryzta, the Teekay group and ICL our top three investment picks, with a combined weight of around 25%.

The geographic distribution has not altered significantly over the quarter either, maintaining a strong exposure to companies outside Europe and the Eurozone.

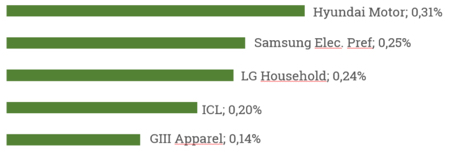

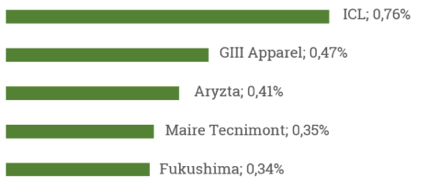

The stocks which contributed most positively to the fund’s performance were:

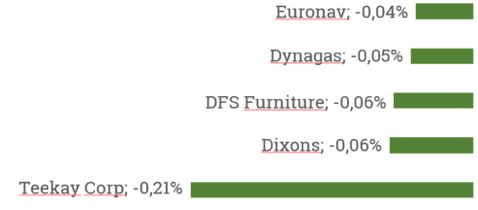

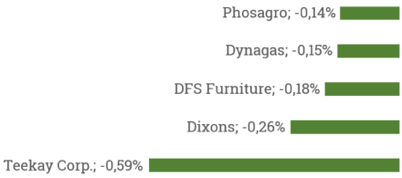

Korean companies, Hyundai Motor and Samsung Electronic, performed particularly well making the largest positive contributions to the fund, despite the negative impact from the Korean won. The companies which weighed most against the portfolio were:

Teekay Corporation inflicted the most damage on the portfolio in the quarter, but we have also taken advantage of the 27% fall in its share price to buy shares on a daily basis. As we have explained elsewhere, we have a very strong belief in the value of Teekay Corporation and its subsidiary TGP and the potential upside.

Indeed, we have increased our exposure in all of these companies that have suffered since we believe they are trading at attractive prices.

The decline in net asset value over this period increases the future potential of the portfolio, given that we have made the most of the declines to increase certain positions. The companies in the portfolio continue to have a very positive outlook, with a potential upside of over 70%, resulting from the attractive prices at which they are trading – P/E ratios of 8 – and their underlying quality, with an average ROCE of 27%.

Cobas Internacional F.I.

We finalised investment in our International portfolio over the second quarter. At the start of June we received authorisation to invest in Korea, meaning that Cobas Internacional was able to replicate our model global portfolio, which we had already invested in the corresponding part of Cobas Selección.

The fund posted a negative return of -3.58% over the quarter, compared to a 0.68% increase in the benchmark MSCI Europe Net Total Return index. Net asset value stood at 98.17 euros per share.

Assets under management to 30 June amounted to 289.9 million euros, with a total of 4,168 shareholders.

The target value for the international portfolio is €173, a long way above its current net asset value, with potential upside of over 70%. We have continued to increase the value of the portfolio over the quarter and we expect that this will be reflected over time in its net asset value.

Portfolio

The weights of the main stocks have not changed significantly, with Aryzta, the Teekay group and ICL our top three investment picks, with a combined weight of over 25%.

Aside from being able to invest in Korea in June, the geographic distribution has not altered significantly over the quarter either, maintaining a strong exposure to companies outside of Europe and the Eurozone.

The largest positive contributions to the portfolio came from:

It is worth noting the contributions from Aryzta and GIII where by purchasing at low points in their share prices, we were able to obtain a positive contribution over the quarter despite a mediocre performance. Our confidence in their value gave us the peace of mind to act on our convictions.

The companies which weighed most against the portfolio were:

As was the case for Cobas Selección, Teekay Corporation inflicted the most damage on the portfolio in the quarter and, as mentioned above, we have taken advantage of the fall to buy shares on a daily basis.

Several stocks dropped out of the portfolio this quarter: Randgold, Casino, Schaeffler and Teekay Tankers. Randgold and Casino performed well, while we found better alternatives to Schaeffler and TNK. In the case of the latter, we prefer to focus our investment on other companies in the group.

The companies in the portfolio continue to have a very positive outlook, with a potential upside of over 70%, resulting from the attractive prices at which they are trading – P/E ratios of 8 – and their underlying quality, with an average ROCE of 29%.

Cobas Iberia F.I.

Cobas Iberia completed its first quarter in operation at the end of June. We have invested the portfolio relatively prudently as Iberian markets performed exceptionally well during the first quarter (the Ibex 35 rose by 11.87% during this quarter). Even so, by the end of April we had invested over 80% and more than 90% by 30 June.

The fund posted a 9.32% return over the quarter compared to a 3.83% increase in the benchmark index composed of 75% I.G.B.M. Total and 25% PSI 20 Total Return. The net asset value of Cobas Iberia stood at €109.31. Nonetheless, we do not expect this exceptional quarterly performance to be repeated on a regular basis.

Assets under management to 30 June amounted to 37.2 million euros, with a total of 1,142 shareholders.

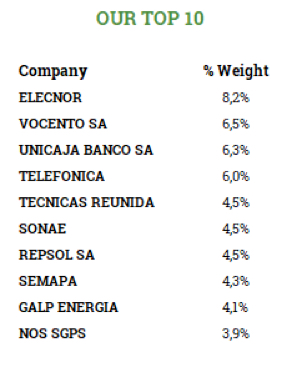

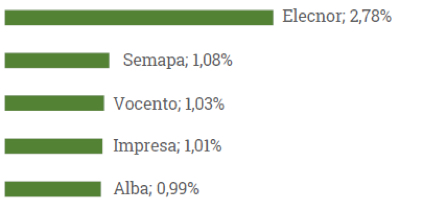

The stocks which contributed most positively to the fund’s performance were:

Elecnor performed particularly positively; a great company with very undervalued assets. We were fortunate to be able to build a significant position over the quarter through purchases of three important blocks.

We have reduced our exposure to some of these stocks, such as the Portuguese company Impresa, which rose by 139% over the quarter.

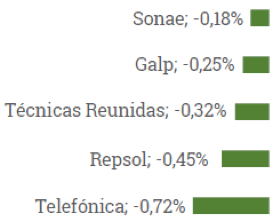

The companies which weighed most against the portfolio were:

The largest negative impact came from Telefónica and oil sector companies. We have increased our exposure to all of them since we believe they are trading at attractive prices.

The strong increase in value of the fund in the last quarter limits the future potential of the portfolio. We currently see potential upside of 30% with a P/E ratio of 9.6 and ROCE of 29%.

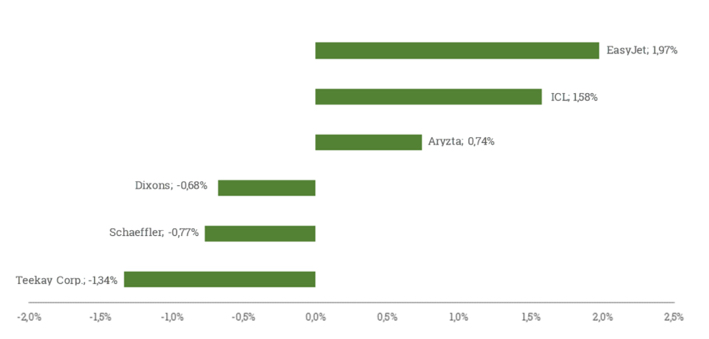

Cobas Grandes Compañías F.I.

This fund holds many of the same stocks as our main International and Iberian portfolios, but it has a global outlook meaning it will always have greater exposure to global markets.

The fund posted a negative return during its first quarter of -2.24%, in line with the -2.45% return achieved by the benchmark MSCI World Net EUR index.

Assets under management to 30 June amounted to 14.2 million euros, with a total of 499 shareholders.

The fund registered a negative performance over the quarter, in line with its benchmark index. Easyjet made the largest positive contribution, while Teekay Corporation was responsible for the biggest negative contribution. As already explained, we took advantage of the falls to increase our positions, given that we expect the stock to perform very well in the future.

Dollar depreciation against the euro resulted in a loss of 1.4% in this quarter, while the depreciation of other key currencies (Korean won, Swiss franc and pound Sterling) led to a 0.6% loss. In line with the other international funds, we have been covering the bulk of the dollar exposure since the end of May.

The companies in the portfolio continue to have a very positive outlook, with a potential upside of over 60%, resulting from the attractive prices at which they are trading – P/E ratios of 8 – and their underlying quality, with an average ROCE of 29%.

Cobas Renta F.I.

The fund posted negative returns of -0.59% over the quarter. The net asset value of Cobas Renta stood at €99.41.

Faced with a backdrop of a financial market where central banks are taking monetary manipulation to the extreme, Cobas Renta has to fight against negative nominal and real interest rates, which hamper efforts to obtain reasonable returns for fixed income investors. Fortunately, our management fee is the lowest on the market, at 0.25%, which provides a degree of relief.

As always, we complement short-term fixed income with a modest investment in equities (up to 15% of assets).

This includes the key companies in Cobas Selección and we hope that over the long-term this will prove sufficient to compensate inflation and our fees, at least maintaining investors’ short-term purchasing power.

Did you find this useful?

- |