Do you know how your mind fails you when you invest? Do you know that your emotions and impulses can play adverse tricks on you when you invest? What lies behind the fears and phantoms that grip us when we invest?

Why are markets so volatile? Why does a share suddenly plunge and then soar although it seems nothing out of the ordinary has happened? Why do we sometimes paint a black picture of the future, and then suddenly we are euphoric within a short space of time?

I feel sure these questions have occurred not only to the readers of this blog, but also to all savers at some point during their investment lifespan.

In the investment world, emotions influence the decisions we take. This is something we see on a constant basis at Cobas when we work closely alongside our investors.

Being familiar with and managing the emotions and impulses we all have can determine the yield we bring in as investors. Emotions we can make a distinction between, depending on the phase our investment process has reached.

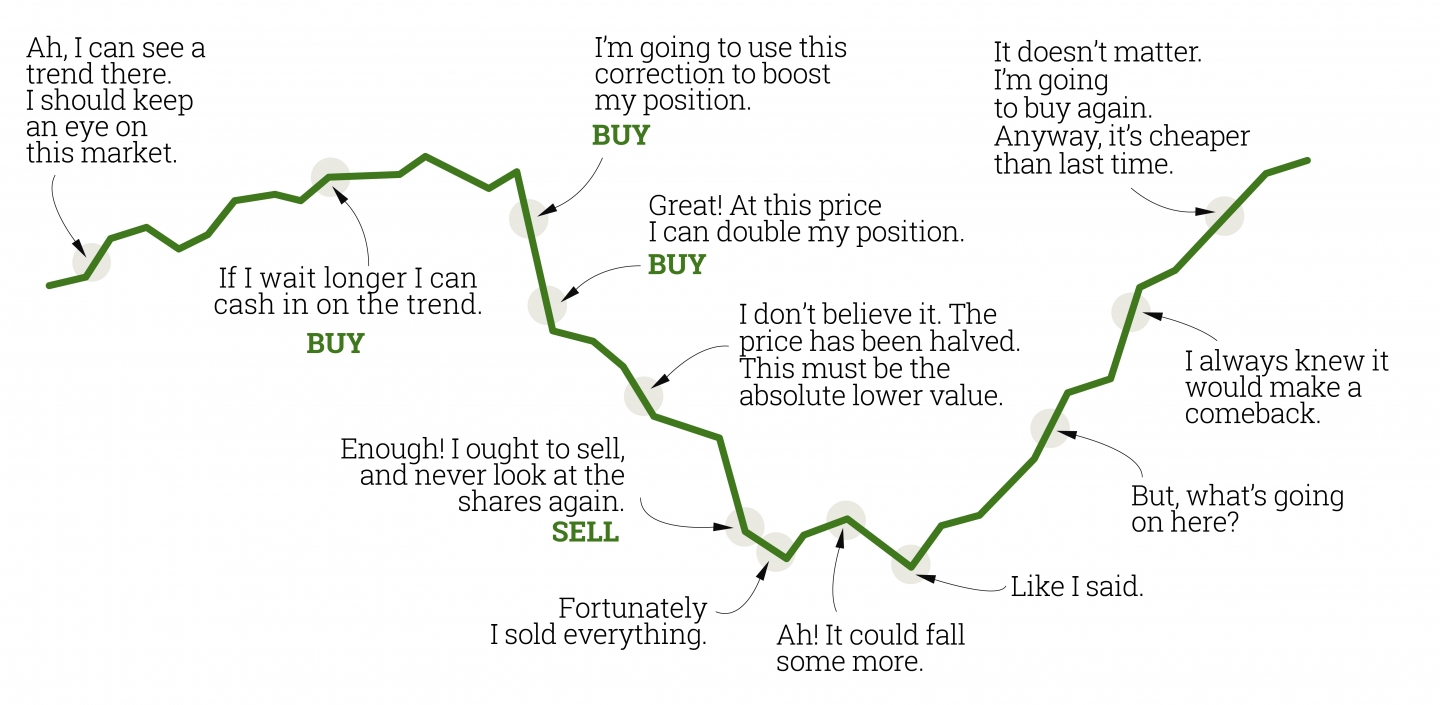

Here it is essential to have some knowledge of the investor’s emotional curve, which explains such commonplace situations as, for example, why investors under the influence of fear or pessimism abandon their investments at the worst possible time. We could say that suddenly we are overcome by the emotion of wishing to take flight, sell out or escape.

It will be observed that the curve indicates various points through which all we investors move:

We experience optimism, great expectations, a kind of joy, when we take the decision to invest, because we believe the operation will go well.

If we see our investment is going well, we will feel enthusiasm, emotion or even euphoria. At this point it is essential to know these are usually the most dangerous times. These are emotions which warn us that a market may have ramped up too quickly or which may bring our guard down. When someone invests in equities they must always be prepared to accept occasional losses due to market volatility.

There are also times when we feel defeated, afraid or discouraged. In these cases throwing in the towel, which is probably what our body tells us to do, is the biggest mistake we can make.

When the investment has been made, we all begin to experience a wide range of emotions, depending on how the market or the fund where we have put our savings develops. This is something that happens to all of us, to a greater or larger extent, and we see this when our investors ask us for help during the bad times.

Behavioural Finance, or Behaviour Finance, explains all this. This is a line of research which is transforming the finance paradigm.

The central basis of the financial theory that has been predominant in recent decades was the hypothesis that the market is efficient and that investors generally act in a rational manner.

In other words, basically these financial theories have focused on how human beings ought to behave, and not on how we actually behave. This means that financial theory has been unable to answer questions as simple as those we have set out here, bringing great misfortune to many investors.

So, by way of an answer to all those questions, what is known as neuroeconomics has emerged, a branch of neuroscience which attempts to explain why we choose certain products instead of others, why we buy something which is more familiar to us, or why we allow ourselves to be influenced so much by the people we know.

In short, behavioural finance sets out to study how human beings actually behave, and not how they ought to behave.

Throughout its development, our brain has developed a number of inclinations which generate distortions, inaccurate judgments and irrational approaches. These are what we know as biases.

A bias is a psychological effect which exerts an enormous influence on our investment process, and which can be identified and isolated by means of various techniques and procedures.

What are the main biases?

- Loss aversion bias which induces us to materialise profits very quickly, in other words to sell as soon as we hit green, and to keep loss-stricken shares even when the prospects are bad.

- The bias of the present which induces us to incur in procrastination on a constant basis, in other words, it induces us to systematically postpone taking the most difficult decisions.

- The confidence bias. We all think we are better than average.

- The retrospective bias, when we tend to remember our successes, but forget the mistakes we made.

- The confirmation bias which makes us focus only on the information which confirms our investment theory.

- The herd effect, which tempts us to imitate the actions and judgments of other people because this gives us security.

- The gregarious effect which goes one step further and usually leads to excessively aggressive manifestations against those who disagree with the majority view.

- The anchoring bias which consists of using the first piece of information we are given as a basis for the rest of our decision-making.

I have listed the principal biases, but there are many more which affect us.

The world of financial psychology is an exciting world, and I encourage you to delve deeper.

We are aware of the importance of behavioural finance, and so at Cobas AM we are working to provide the best possible support for our investors, and the best possible techniques and tools. We will shortly be announcing some new features in this field.

One of our first initiatives was a series of videos with Value School, where we address the world of biases:

https://www.youtube.com/watch?v=jEZRN2wYfR0&list=PLNNPgD3OayokAJYrWiyEPSJebNt_Ch9aK

Value investors must pay close attention to emotional factors when making investment decisions. For a proper application of the value investment, the investment process must not only be rigorous. It is extremely important for them not to let themselves be influenced by the rest of the market, and be capable of going against the flow.

Being a value investor can be difficult, and at times fraught with discomfort at negative short-term returns, but highly satisfying and profitable both intellectually and financially in the long run.

The key is being faithful to our convictions, investing in a logical and simple manner, applying common sense, and being patient to move in on the opportunities afforded us by finance markets.

Lastly, I wish to share two reflections which will bring us closer to success when we invest:

“Equities are the most profitable asset with less risk in the long term”

“Patience is not the ability to wait, but the skill of maintaining a positive attitude while you wait”

Did you find this useful?

- |