At Christmas time, Santa Claus and the Three Kings are usually very generous to my very lucky children, aged 6 and 8. They have an incredible time both at home and at their grandparents’ house. And they end up with a ‘reasonable’ sum to put towards making their dreams, or part of them, come true. My wife and I, like many other parents, also make the most of the occasion to give them equipment for after-school activities, for example. Although I must say that the best gifts they received last Christmas, in their opinion, were some little packs of frightful figurines with horrible names that cost around two EUR each. So far, we’re just a normal family.

What makes us a little different to other parents is that we allocate a small part of our budget every year to the investment funds that we opened for them not long after they were born. And even though it is not much, we believe it is the best gift we can give them.

Firstly, we are providing them with funds they can use when they are older and wiser to fulfil some of their dreams, such as taking a big trip, studying at a university far away or, in the best-case scenario, leave invested for a better-quality retirement. It will be their decision at the end of the day.

It may initially seem that the amount invested will not contribute significantly to such ambitious goals, but surprisingly it will, as long as we are able to make recurrent contributions, every year, to long-term investment in diverse equity.

A real example

My eldest son, Nicolás, was born 8 years ago, in 2011. If we had invested just EUR 100 in the S&P 500, he would now have approximately EUR 236. In other words, we would have multiplied that gift 2.3 times over the 8 years. The S&P 500 is an index based on the stock performance of 500 large companies with global sales listed on the US stock markets. It captures approximately 80% of all capitalisation in its stock market and ensures sufficient diversification. We can invest in it through investment funds or ETF.

But the observant reader will have realised at least two things: one: that we are not taking inflation into account; and two: that we have not considered a long enough period, and that the period considered was also essentially a bull market.

- So, let me then include inflation, which has risen to 7.4% during this period, according to the Spanish Institute of Statistics. In other words, the EUR 100 from 8 years ago are the equivalent of EUR 107 today. And instead of multiplying by 2.3, as it has logically been decreased by this inflation, it should be multiplied by 2.2.

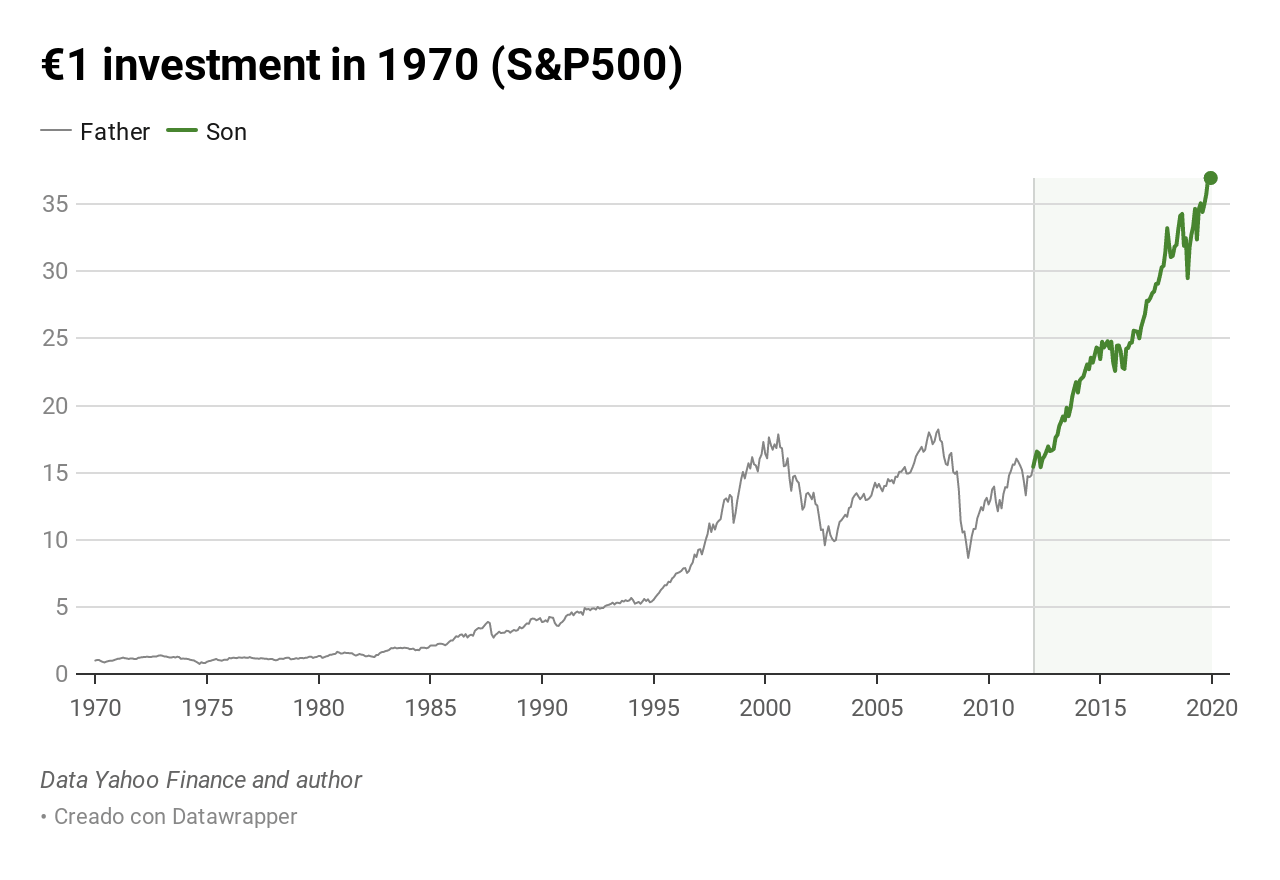

- To analyse the effect of corrections or falls that did not take place during this period, I’m going to create a parallelism with myself. I’m going to imagine that my parents made a contribution of one EUR for my first Christmas, back in 1970. That would have been multiplied more than 36 times today. We must also take into account inflation. According to the Spanish Statistics Institute, prices have multiplied by approximately 23. Adding both of these, the amount my parents would have invested for me when I was born would have been multiplied by 13. In other words, in constant terms, I would now have capital gains of EUR 13.

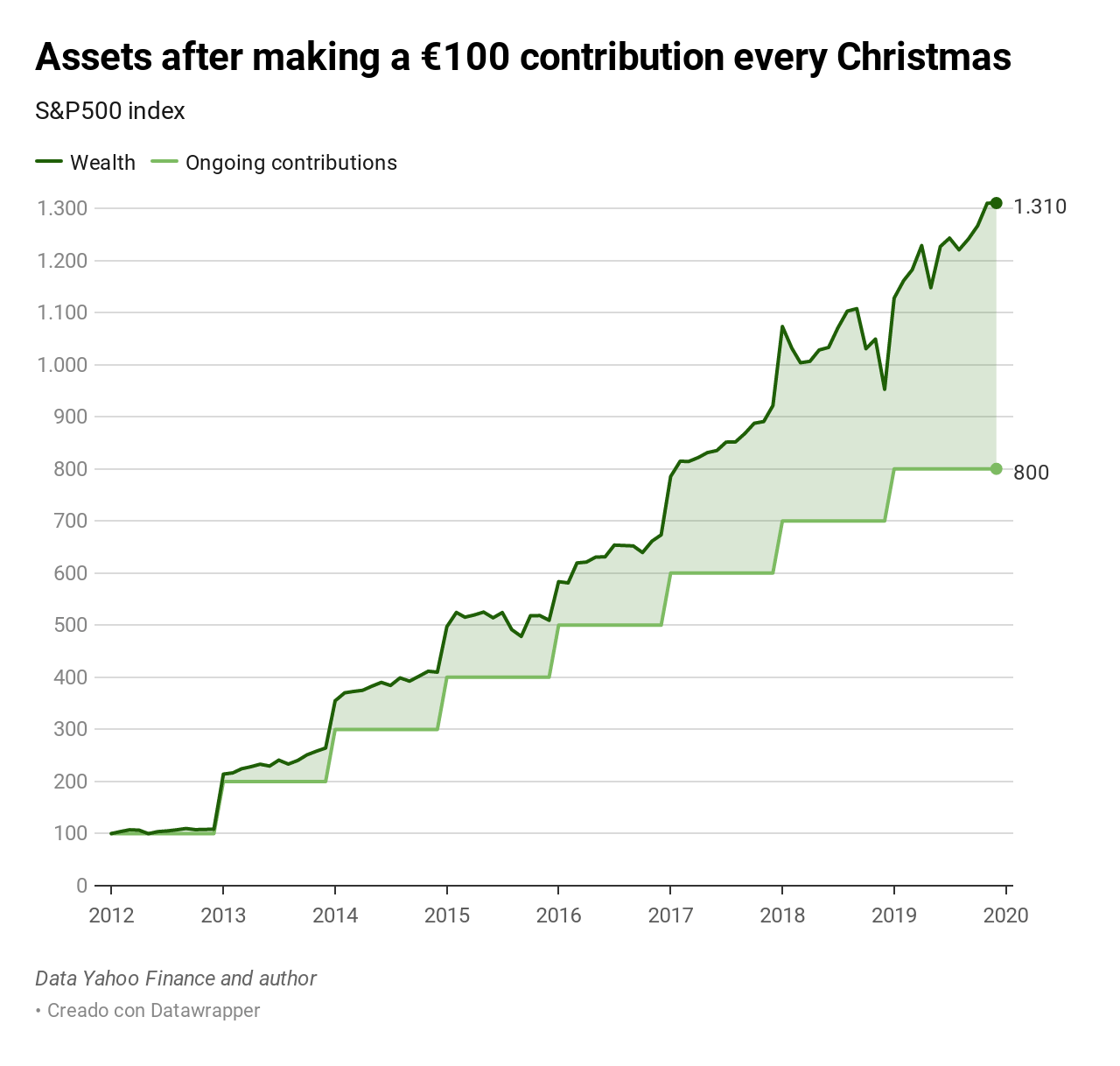

But if, apart from the long period and the diversification, we are constant and we invest part of our budget for gifts every year, the assets we will be leaving our children will notably increase. If, for each of these 8 Christmases, we had invested EUR 100 in the same index, my eldest son would now have EUR 1,300

As our children get older, they will see how their assets are growing. On the one hand, by consuming responsibly, they will be able to generate savings and, on the other, the compound interest will ‘work’ in their favour in the long term to multiply these savings.

Goof financial habits and culture

I feel enormously fortunate to form part of the Value School team and to be able to offer our Value Kids financial education programmes in line with these principles to parents and schools who are interested in them. We have also developed and are selling boardgames that are going to help us work on good habits and conduct with them:

- Memory Value is aimed at smaller children and involves pairing cards. But, unlike classic memory games, where you try to find like cards, here the smallest members of the household have to pair good and bad habits. For example, washing their teeth with the tap running (bad-habit card) and with the tap off (good-habit card).

- Play Value is another card game that aims to strengthen good habits, among older people this time. For example, you will get more points for working hard than for leisure time.

- Be Value is the game for older people. It is about managing to be happy and increase our assets at the same time. At times, it is not easy. Having a child is one of the things that can make us happiest, but it is sure to affect our wallets. We have to save and we might win the game if we invest correctly.

See all of our educational and dissemination activity at www.valueschool.es and at www.valuekids.es

Did you find this useful?

- |