We know that every day more money flows towards ETFs, passive and quantitative management (with or without AI) of portfolios. This increase in the volume of passive management reduces the efficiency of the markets, which allows Investors (in capital letters) to make the most of these inefficiencies and find value at a good price. Unfortunately, the majority of those buying and selling on the Markets are not looking for value but rather profits, (sic) which are usually found in a cyclical and reckless manner between loss and loss. They are not looking for good businesses to buy, but rather winning tickers on which to bet. And for this they use ephemeral crystal balls that they discard one after the other when the future makes a fool of them.

In addition, active management does not manage to exceed the Markets in more than 8 out of every 10 cases. In this awful statistic gets even worse when we extend the investment period. All of which contributes to increasing the inefficiencies on the markets, which a good “value” manager (they do exist) makes the most of in the long term. The key for the investor is obvious, knowing how to choose this scarce percentage of active fund managers that exceed their reference indices in a clear and sustained manner throughout the years.

Then, from among this scarce percentage of brilliant active fund managers, we can select nuances, according to the taste or circumstances of the investor: Deep value, value, long only, L/S long bias, etc… But always exceeding their indices with relatively concentrated and local portfolios and fund managers, given that diversification and distance are inversely proportional to the knowledge of the businesses in which one is investing.

This exhaustive knowledge of the businesses in which one invests is the basis upon which the results over the years are based. It is not enough to study the accounting balances published periodically by the companies (many active fund managers usually restrict themselves to this, at the very most). It is necessary to travel, to get to know the companies in situ, their directors, facilities, suppliers, competition, local market and customers, etc.

There is a group of star fund managers that have shone above the rest for decades

It is with this in mind that a few decades ago we realised that, as investors and fund managers of our own and customers’ assets, we would be much more efficient specialising in the selection of fund managers and funds than in the selection of stock in which to invest. Because no matter how capable our team is, it is impossible to reach the degree of knowledge that these select few fund managers possess, whose teams constantly travel personally visiting directors and corporate facilities throughout the year.

This select group of staff and managers that have shone above the rest for decades, possess teams comprising dozens of analysts, including some with private jets that allow them to pay regular personal visits to the companies and the management teams in which they invest their money and that of their investors. Thus, they regularly compare their business plans, future strategies and all types of corporate decisions, which go far beyond the painstaking study of the balance sheets carried out at the fund manager’s headquarters.

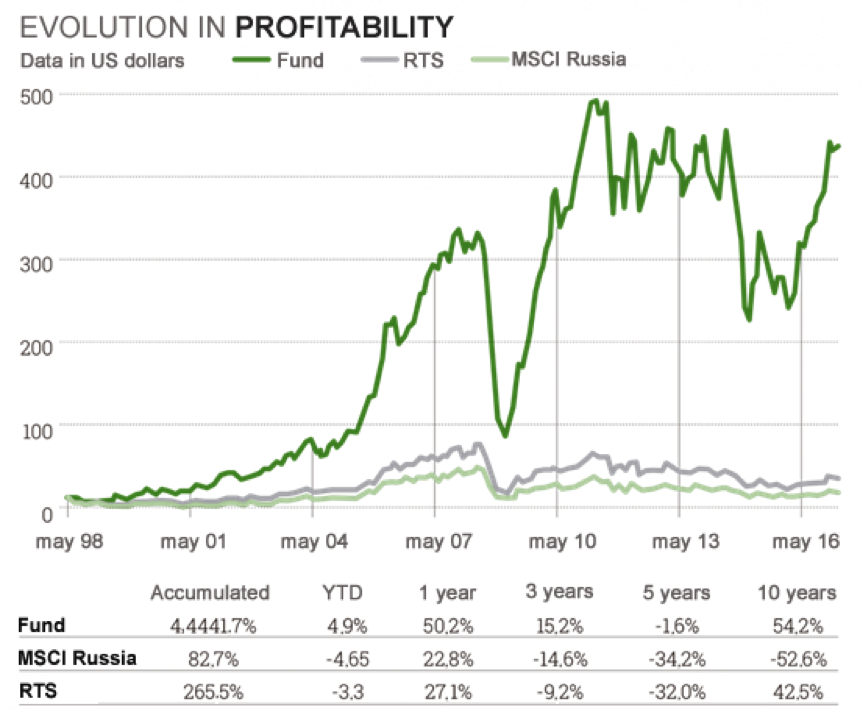

So that the readers can have some idea of the size of what we are discussing, a certain fund manager that we have in our portfolio made 2,200 personal visits to different companies last year (not including telephone calls). This is a normal part of their prospecting activities and exhaustive study of the businesses in which they are, or may be, shareholders through their investment funds. Below you can see a sample of the returns of the funds where their “value” fund managers have been achieving extraordinary alphas, in a consistent manner for over a decade and in extreme markets such as Russia (where logically they have been finding greater inefficiencies and volatilities that can be taken advantage of than in fully developed markets):

But the difficulty of finding these fund managers in the sea of active management, normally sold by private banking, is what causes many investors to throw themselves into the arms of passive management, tired of paying management fees to not even equal the reference index. Unfortunately it is very difficult to find good fund selectors in the financial sector, whose catalogues of sales are limited to funds registered with the CNMV to whom they pay juicy fees, because they have limited history and management teams that are as changeable as they are anonymous.

Luckily, the recommended funds, with their stable teams with names and surnames and a history of more than 10 years, still place a focus on results, improving in the indices, ETFs and semi-passive or fundamental ETFs, in a consistent and sustained manner.

The correct analysis and assessment of companies is, and should be, an art form. And artists, they do exist, are the reason for the existence of a good fund selector.

Did you find this useful?

- |