The efforts made by many Spanish managers in the area of financial literacy are well known, and Cobas AM is a prime example with its bold Value School initiative. Perhaps the seed for this initiative stemmed from the Annual Investment Conferences, pioneered by Francisco García Paramés while he worked at Bestinver and which fortunately continues today. Before, investors who placed their trust in the skills of an active manager were asked to do too much, yet offered little explanation and even fewer practical recommendations in return.

The quarterly reports required by law and the annual investors conferences have gone a long way to filling that gap. Cobas AM even publishes a monthly newsletter. After the steep falls by stock markets in the fourth quarter of last year, with several of our investment funds hit particularly hard, these efforts seem to be paying off.

Now, instead of taking what’s left of their assets and running, investors are staying in and those who are in a position to do so now are increasing their holdings, at least here. This all means that the fiduciary relationship between managers and unitholders is heading the right way, because if we start by trusting managers to take care of our money and achieve good returns, there would be no reason and make no sense to ignore their messages now.

The manager-investor bond is not sporadic but ongoing, and achieves its maximum expression not in periods of bonanza but at times of turbulence. Anyone who has read “Investing for the long term” by F.G. Paramés himself, and any other classic works by renowned investors, such as Peter Lynch, will have reached the conclusion that deciding how we behave in relation to our investments is as important or more so than deciding what, how much, when, where and – as the case may be – with whom we invest.

So with the margin of error implied by all general rules, when the management company urges investors to take a long-term view of stock market investments, to contribute money regularly, not to divest in the midst of stock market turbulence and to invest more money, if possible, when the market falls and funds suffer, it is a good idea for investors-unitholders to listen and act accordingly.

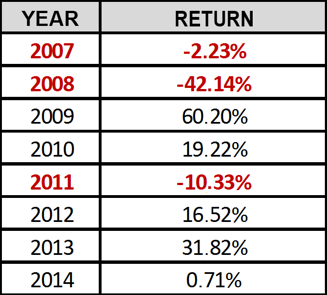

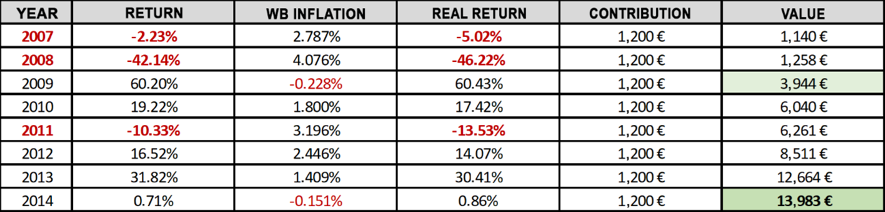

Let’s take, as an example, nominal returns, net of commissions and expenses, obtained by FG Paramés with Bestinfond during the eight erratic years between 2007 and 2014:

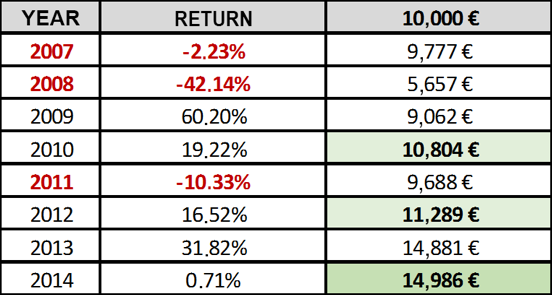

As illustrated, anyone who started investing for the first time in 2007-2008 received a unpleasant surprise. They had been told that value investing was something else! Even so, in spite of the three years in the red – particularly 2008 – how would investors who had invested €10,000 in early 2007 have fared?

Maybe not as badly as it may appear at first sight. By the end of 2010, only two years after the terrible recession of 2008, they would have recovered their money without any further setbacks. And also by the end of 2012. Although it may seem obvious, when managers recommend not to sell after a bearish year, they are not doing so gratuitously, as it is in the ruins of the bear markets where the seeds are sown for the green shoots that offset losses and offer gains. In this first example, the investor would have obtained a total return of 49.86%, and a 5.19% compound annual return.

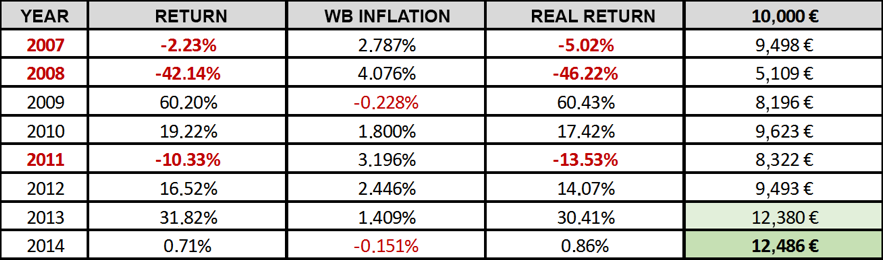

But if there is one recommendation that is repeated constantly by managers when imparting financial advice, especially here at Cobas AM, it is to opt for real assets, such as shares, in order to protect our savings from inflation, which along with taxes is the investor’s worst enemy. If not, just take a look at the previous results in real terms using the annual inflation rate for Spain provided by the World Bank:

The previous €14,986 are really “worth” €12,486, and the real accumulated return is not 49.86% and 5.19% CAGR, but 24.86% and 2.81% respectively, so investors did not recoup their money in real terms in 2010 or 2012, but in 2013; that is, seven long and agonising years after their initial investment.

In the past, we theorised about the benefits of regular contributions in relation to passive management in “The Asymmetric Financial War”, which was successfully presented at the Value School. But this concept is far from being exclusive to indexed management. Another of the managers’ recommendations consists of investing regularly in your funds.

This way, investing is a series of actions over time – a constant process through which the investor’s tendency to hyperactivity can be effectively channelled and controlled. Regulating it avoids compromising all our resources at a bad time, so the investment is automatically tempered in bullish periods and maximised during bear markets. And this procedure ties in nicely with the type of income almost all of us receive, which is periodical and in the form of wages and salaries.

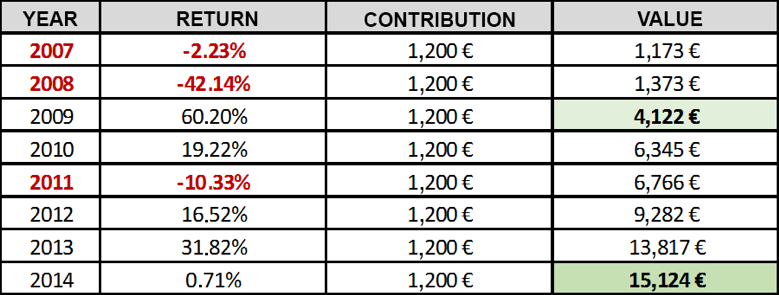

For example, if the previous investor did not have €10,000 in 2007 but was able to save €100 a month which was invested at once at the beginning of each year, the results would be as follows:

Now the investor pays in €9,600 and obtains a total accumulated return of 57.54%, equivalent to a 5.85% CAGR if we count in the entire amount invested since 2007. In this case, an investor wishing to recover their money could do so without any problem right after the end of 2009, as they would have invested €3,600 and would now have €4,122.

In real terms, the situation is also improved compared to the initial one-time investment:

*WB Inflation = World Bank Inflation

The €15,124 is now actually “worth” €13,983, accumulating a total return of 45.66% and a 4.81% CAGR. Here, too, the investor could successfully recoup the initial investment in 2009.

All of this means that the discipline of paying in regularly increases the security of the capital already invested, which is recoverable in shorter periods than in the case of a single initial contribution. If the stock exchange is going through a period of turbulence, regular investments or the average of the monetary cost affords calm and rewards.

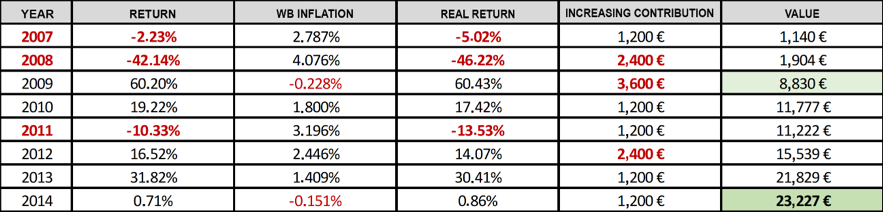

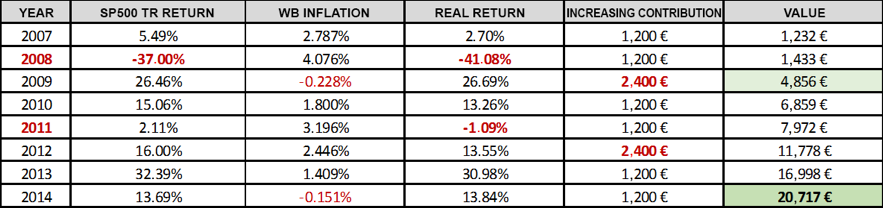

But managers also insist on paying in more money when the market falls, as the lower the share price, the greater the future returns and the lower the risk. Let’s assume that our investor pays in double the usual amount in 2008, after the falls of 2007. That is, instead of €1,200 they invest €2,400. And in 2009, after another poor year, they stubbornly continue investing triple the usual amount, €3,600. Then, in 2011, after the falls of 2010, they invest double the normal, €2,400. Will the managers have been right? Let’s see:

In this case, the investor pays in €14,400, an average of €150 a month rather than €100. In 2014, it amounts to €25,177, a total accumulated return of 74.84%, a CAGR of 7.23%. As we can see, this is better than the previous examples. What’s more, due to the self-imposed obligation of saving more, the investor necessarily has more capital. They can also sell at no loss at the end of 2009 as they will have paid in €7,200 and already have €9,079.

And in real terms?

Once again investors who followed instructions correctly will have come out on top. Their €25,177 is “worth” €23,227, a total accumulated return of 61.3%, and a CAGR of 6.16%. In real money. And what’s more, after 2009, they would have been able to withdraw their money without any reduction in the capital invested, as their €7,200 would be worth €8,830.

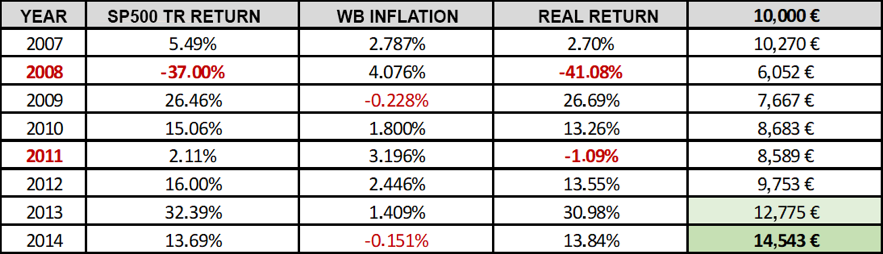

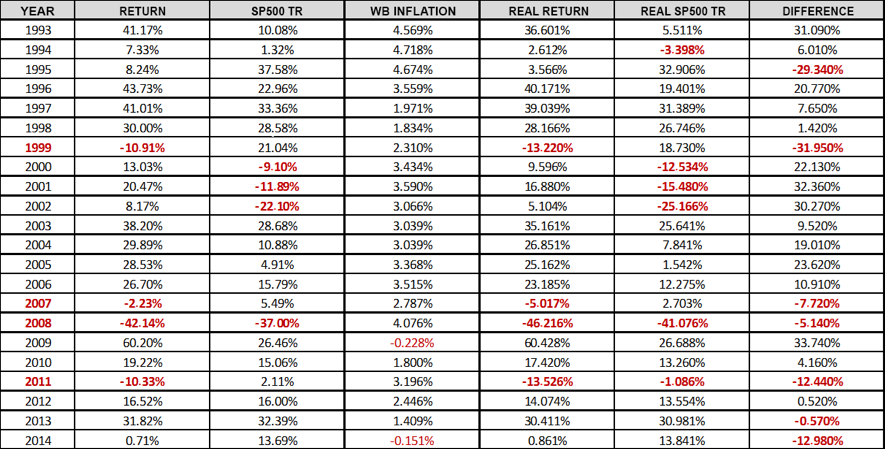

So, what would have happened to the investor tied to a benchmark index, with no guide at all except their own judgement, such as for example the SP500 TOTAL RETURN in real terms, after discounting Spanish inflation.

If we look at the example of the initial amount invested, the SP500 TR wins, as it achieves a total accumulated return of 45.43%, a CAGR of 4.79% compared to FGP’s 2.81%, although here too the investment cannot be recovered until after the end of 2013:

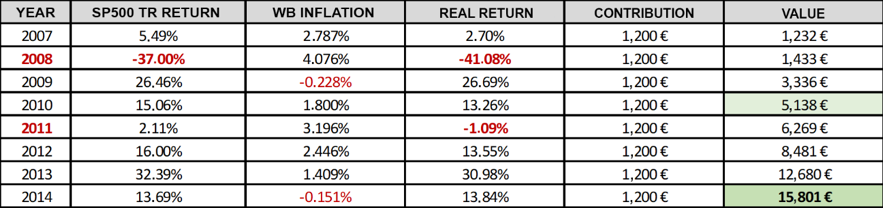

For an investment averaged over time, the balance is once again in favour of SP500 TR, which achieves 64.6% and a CAGR of 6.43%, compared to 45.66% and a 4.81% CAGR from the leader of Cobas AM. However, investors would not have been able to recover their money at the end of 2009, needing to wait one more year until 2010:

By investing more when the stock market falls, the SP500 also offers better results, with a total accumulated return of 72.64%, a CAGR of 7.06%, compared to FGP’s 61.3% and 6.16% CAGR. In this case, too, investors can recover their 2009 investment, but only barely:

However, the comparison is incomplete and unfair, because it overlooks the “currency effect”, brokerage costs and the tax withholding on dividends, whereas both factors are already discounted from FGP’s returns and they are stated in euros. The performance of the SP500 TR between 2009 and 2014 is above the long-run average of between 9%-11% nominal (6%-7% real). Nonetheless, this is a perfect example of the title and content of this post, and which – in our humble opinion – we recommend not to forget and to observe rigorously.

Indeed, another observation-recommendation that is a “house speciality” is to focus on the long term, because it can be said without any question that successful active management requires the blessings of compound interest to offer consistent results, and that these results inevitably involve periods of time in which indexes outperform managers.

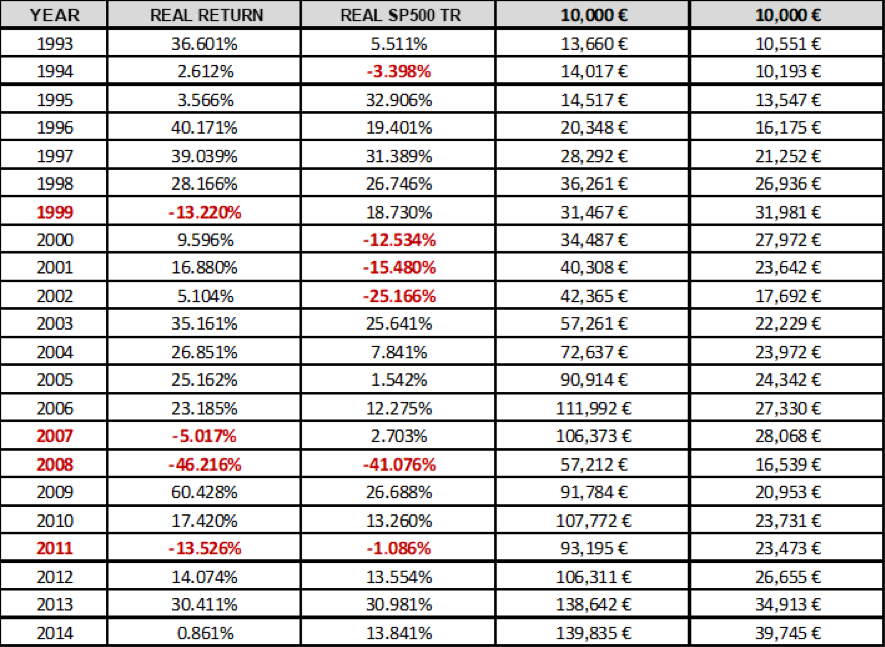

Let’s look with hindsight in light of the annual performance in real terms obtained by FGP and SP500 TR during the 22 years between 1993 and 2014:

As we can see, the balance is tipped significantly in favour of the active management practiced by F.G. Paramés, and although there are seven years where the SP500 TR outperformed, most are concentrated in the 2007-2014 period. Even so, €10,000 with FGP would become €139,835 in real terms, offering a total accumulated return of 1,298% and a 12.74% CAGR compared to 297% and 6.47% respectively for the SP500 TR, which achieves €39,745 in real terms, and from which we would still need to subtract tax withholding, dividends, and fees and commissions:

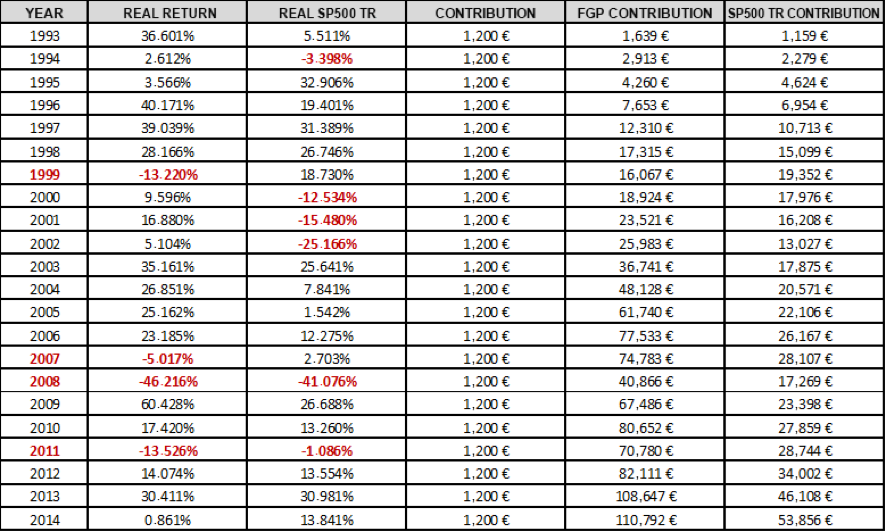

If the investment had been averaged annual at a rate of €1,200 each year, it would also far outperform FGP, as after a contribution of €26,400 the investor would have €110,792 in real terms, 320% accumulated and a 6.74% CAGR compared to €53,586 for the SP500 TR, 104% accumulated and 3.29% CAGR.

It is true that past performance does not guarantee future returns. But it is no less true that constant and continuing results over sufficiently significant periods of time indicate that active management is being practiced in a virtuous way. Indexation to the SP500 TR produces good results and would be hard to beat for most active managers. However, when active management is done well, there’s no comparison.

If these results can be achieved by following the long list of recommendations described in this post and constantly reiterated by the managers, even in the case of long periods of low returns for the more significant indexes and even greater volatilities, we believe that the conclusion points firmly to the advisability of investors following the advice of their manager, to whom they are bound by a relation of trust.

That is, listen and act. Listen to the manager and act accordingly.

Did you find this useful?

- |