Society seems to be beginning to see the light at the end of the COVID-19 tunnel. A light that began to appear at the beginning of last November, when governments announced the start of the vaccination processes, which are now well underway in practically all of the world’s developed economies.

This light has been taken as a given by the market with a strong asset turnover since those dates, which is leading investors to turn their eyes back to businesses that until now had not enjoyed all the prominence that perhaps, in view of their fundamentals, they deserved. We have been seeing strong rises in commodity prices, in cyclical businesses and in virtually everything where the market expects a recovery thanks to the anticipated pick-up in activity, stemming from the ever-closer end of all the restrictions imposed after the outbreak of the pandemic.

However, this new normality that we are approaching may not be as normal as one might expect. The gradual recovery of economic activity is bringing with it a situation which, although it could be considered to be expected, is no less worrying, and it is that, as we move towards 2021, the upward pressure on the prices of some goods is increasing.

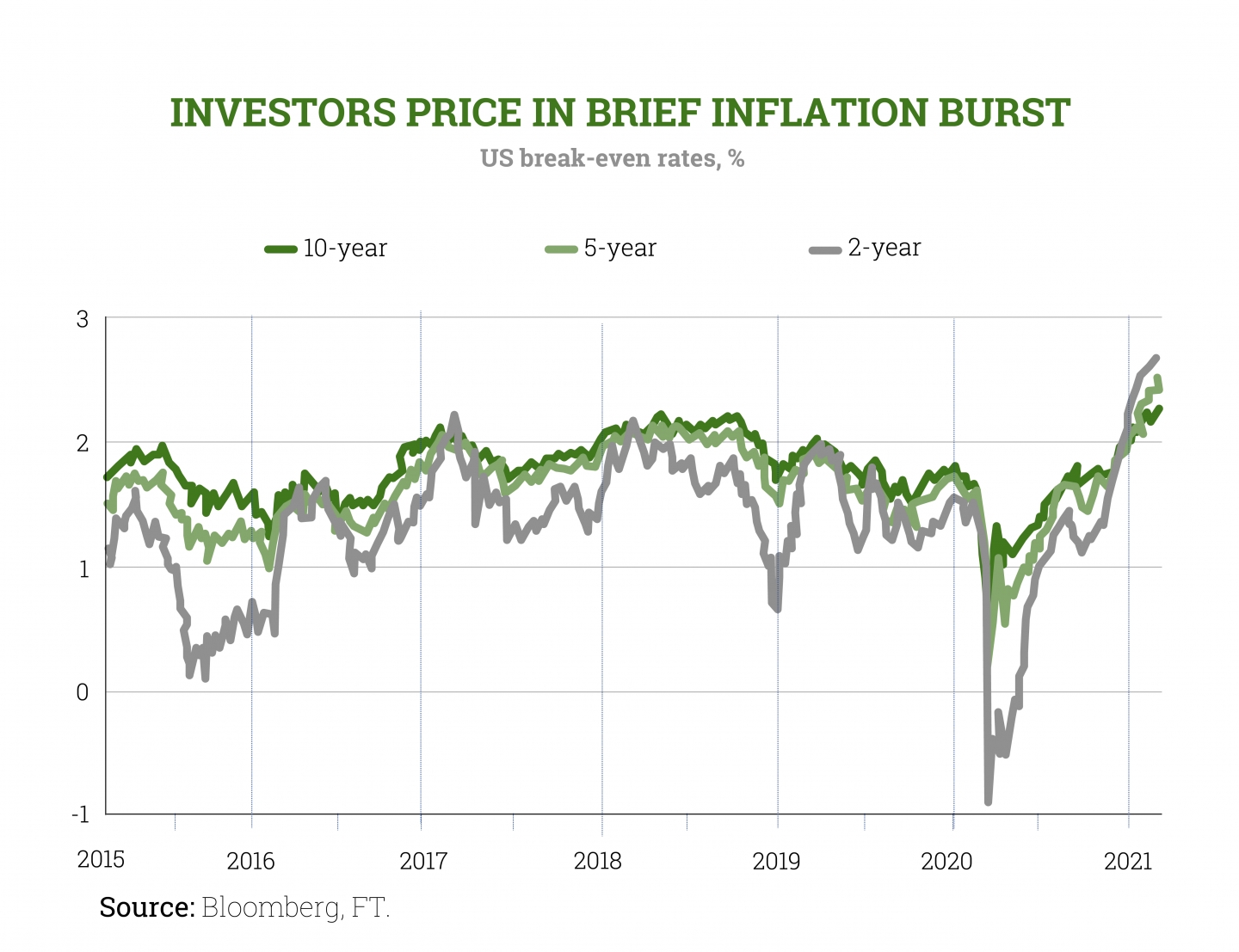

This is evidenced by the latest inflation data presented by the different economies. In the United States, the year-on-year CPI in May rose by 5% (comparable with the same month a year earlier), marking the largest year-on-year increase since August 2008. The core CPI, which excludes food and energy prices, rose by 3.8%. Both figures are above the Federal Reserve’s forecasts. The same is happening in Europe, with better than expected data in recent months, in general in all the continent’s major economies.

“Thinking in the short/medium term, we can say that the inflation figures should not be surprising.

The pandemic has altered the production and consumption of various goods. For example, in the early stages of the pandemic, car manufacturers reduced their orders for semiconductors. As car orders pick up, semiconductor manufacturers, always working to optimise inventory numbers, are falling behind in producing enough chips to meet all the demand. That is, because of the impossibility of producing enough devices, the size of a coin and possibly costing no more than a few tens of euros in the total cost of a vehicle, we are seeing higher prices for both new and second-hand cars.

The semiconductor shortage is expected to be resolved (by 2022), car production will return to normal and supply and demand in the car market will return to pre-pandemic equilibrium.

Another example would be the price of timber in the US. The demand for new housing, driven by low interest rates, and the increase in remodelling, fuelled by the inability to consume services and the obligation to stay at home during the last few quarters, have strongly boosted the demand for timber. At the same time, social distancing rules in American sawmills have reduced supply, so lumber prices have soared by more than 300%, driving up the cost of houses by tens of thousands of dollars.

High timber prices will encourage sawmills to hire more employees or to run triple shifts. Increased supply will meet demand and timber prices will stabilise at pre-pandemic levels in a relatively short period of time. That is the beauty of capitalism!

“High prices are cured by high prices”.

These are just two examples, but we are seeing such processes in countless production, supply and transport chains.

Therefore, if only these supply-demand mismatches are taken into account when assessing the current inflation data, it seems reasonable to assume that this is a transitory event.

Moreover, we must take into account the base effect, which implies that the inflation data we are seeing these months are conditioned by the very low point that these same data reached just a year ago, at the height of the pandemic.

But forget about the supply and demand mismatches caused by the pandemic, which seems to be what central banks are relying on when claiming that they are not worried about inflation and consider it to be transitory.

“Let’s think about the value of money”.

If the supply of vintage cars were as plentiful as the supply of modern low-end cars, the price of vintage cars (i.e. the trade-off between vintage cars and money) would change considerably. In that case, we could acquire a vintage car at much less sacrifice than is required today.

Similarly, if the quantity of money increases, the purchasing power of the monetary unit decreases and, therefore, the quantity of goods and/or services that can be obtained for one unit of that money will also decrease.

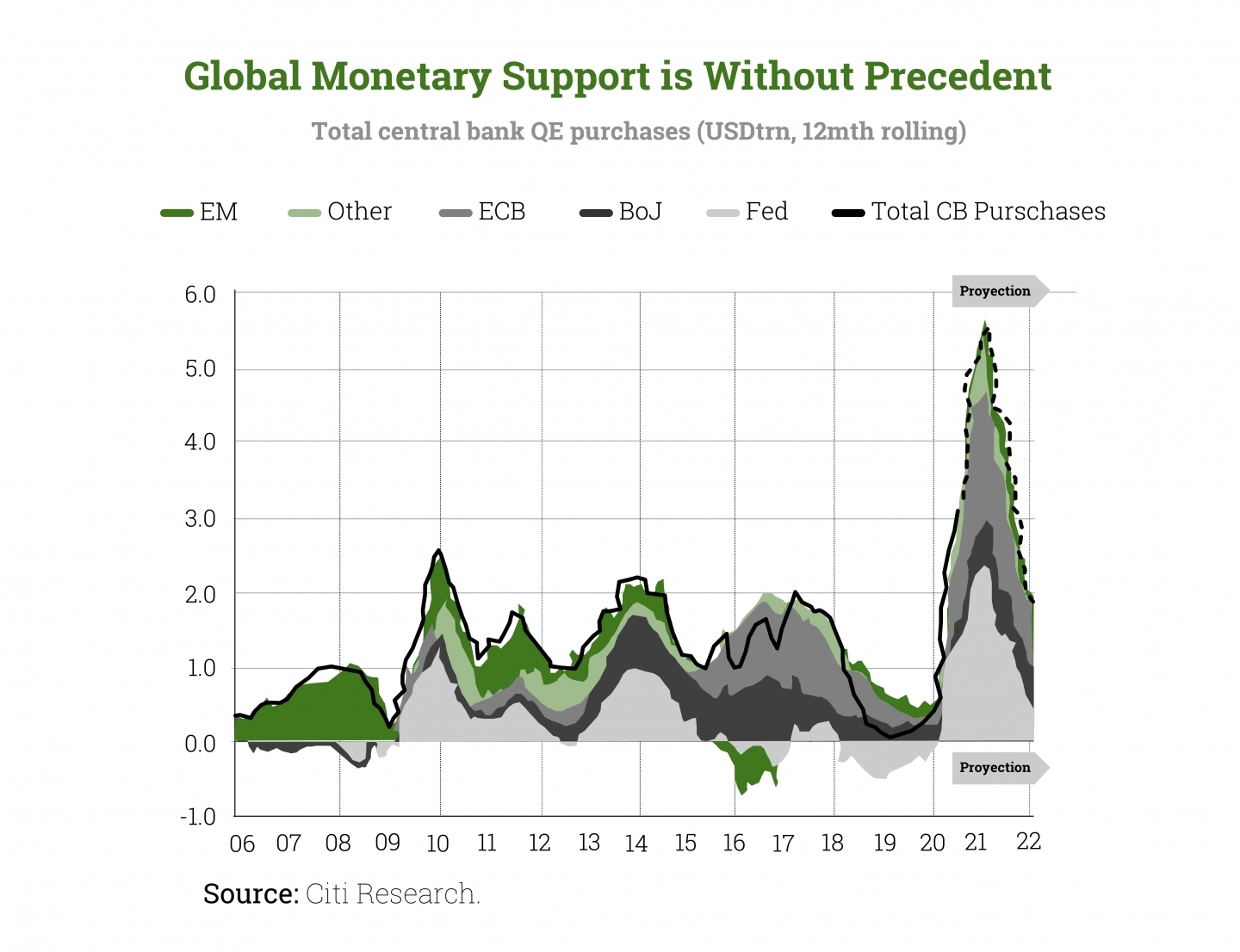

Well. The response of central banks to the Coronavirus crisis has been tremendous. There has been an unprecedented coordinated stimulus in both monetary and public spending policies (which may eventually need the former to finance themselves). This is all taking place in an environment of negative or at best close to zero interest rates.

In other words, we find that in recent years the creation of new money has advanced at probably the most ferocious pace in history and, moreover, that the price of money (i.e. interest rates) is at abnormally low levels which, as I said, have even reached negative territory (i.e. we are paying to lend in some cases).

In short, never in history has there been so much money in the world and never in history has it been so cheap.

Moreover, in this case, much of the new money created has gone directly into the hands of citizens, which has led to companies in the US such as Amazon being forced to raise the minimum hourly wage in order to incentivise workers to work rather than settle for the cheques paid out by the Biden administration.

Likewise, in a country that structurally usually presents a situation of full employment (it is once again close to the level considered to be 4%), the foreseeable increase in demand (let us remember that this crisis has not affected wallets like other past recessions) will possibly mean that companies will have to compete among themselves to hire the human capital necessary to meet this growing demand and, to do so, they will have to offer more attractive conditions than their competitors, via wages.

These two factors will lead to an increase in arguably the largest single item of expenditure in an economy, wages, to which companies will respond by adjusting their prices in order to protect their margins (thus at least partially reducing the real purchasing power of those higher wages).

Wages, unlike timber or semiconductor prices, rarely fall. It is difficult to tell a worker that they are valued less, and it is usually common to tell them that you need less of their time, or that you simply don’t need them. That said, it is conceivable that once the US government stops paying people to do nothing, the labour market will stabilise. However, these new higher wages will remain, so it seems understandable that cost inflation is likely to continue over time.

Returning to the increase in the money supply, it stands to reason that the more money there is in an economy, the lower the value of each unit of money, especially when a significant part of this money is being created by magic, out of thin air, and does not come from the reasonable and healthy process of saving and investment.

For this reason, and taking as a reference the economic theory developed by the economists of the Austrian School of Economics, at Cobas AM we believe that this excessive creation of new printed money by the agents responsible for monetary policy will result in a loss of value of the currency, which will ultimately be reflected in one way or another in the prices of the goods and services that we exchange using this money as currency.

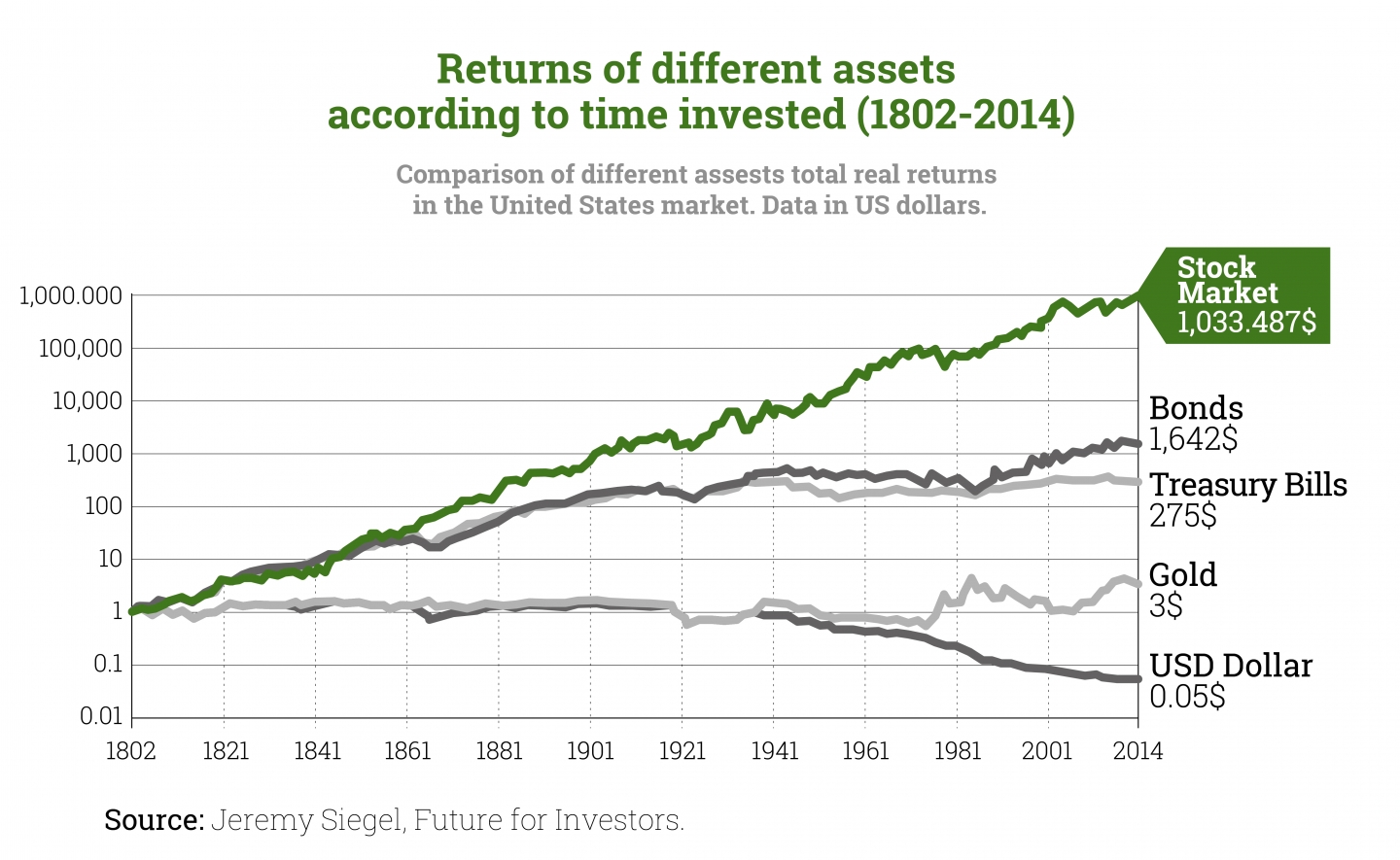

At this point, the question is, how can we protect ourselves? In our view, the best means of protection is to hold real assets.

“Real assets reflect ownership of underlying assets, albeit with greater or lesser immediacy. This asset creates income for the specific service it provides to society.”

The essential characteristics of real assets are: “ownership of the thing”, which can be direct or indirect “shares, for example, are representations of property”, and total or partial “we can own the whole asset or a minimal percentage”; and “variability in the income” generated by the asset. The degree of income variability will depend, firstly, on society’s interest in the product, which will change over time and will be immediately reflected in the price that society is prepared to pay for the good. And, secondly, the producer’s capacity to offer the product at a reasonable cost, because not everyone is in the position to supply efficiently.

The main upshot of owning an asset which fulfils a service demanded by society is that it will sustain its purchasing power reasonably well in any economic environment, so long as society retains an interest in it. Returns on real assets will vary according to numerous factors, but their ability to retain purchasing power reasonably well is irrefutable and crucial.

In short, it is a clear fact that we are seeing inflation today. Given the effects of the pandemic, this seems likely to be transitory, too, and the actions of central banks seem likely to lead to a loss of purchasing power of the currency in the long term, too.

Moral: PROTECT OURSELVES BY INVESTING!

Did you find this useful?

- |