It’s very common to hear that young people will no longer have state pensions, and that even their parents are unlikely to have them either. With this type of prediction, it’s better not to speculate and the most sensible thing to do is to take precautions to avoid the worst-case scenario. In other words, saving and investing to ensure a comfortable future.

I’ve been working for almost a year now and I’m trying to carry on with the lessons I’ve been taught at home, where saving was always an essential part of my upbringing. But saving is the first step, you also have to make the decision to invest, either to study a master’s degree, pay the deposit for your future home or to have a pension further down the line.

When most people think of pension plans, they think of old age, of retirement. But as always, for a tree to provide us with a pleasant shady spot on which to rest, it must first be planted, then watered and fertilised throughout its life so that it grows continuously.

The same goes for our pension. Every month, the State takes a part of our salary to pay for current pensions, as the system works in a “contributory” way. Of course, the system will work as long as there are more workers than pensioners. However, it remains to be seen what will happen in the near future, as Spain’s population pyramid is changing, and the upper part may become larger than the lower part.

We must therefore begin to think that many of us will have pensions thanks to that individual process of saving and investing for many years in advance. We can’t just hope that year after year the State will transfer that income to us, which it is currently collecting from workers.

Depending on which friend I talk to about this, they tell me one thing or another. Some say that in the long run we are all dead, “that I know what’ll happen in the future and what’ll happen in 20, 30 or 40 years with Spanish pensions”. Others, on the other hand, agree with me and are aware of the need to save for a rainy day.

In order not to fall prey to a confirmation bias, I’ll try to explain why it’s imperative to save and invest and why doing so through a pension plan is so worthwhile, despite the fact that we all know that our journey in the world has an end.

Benefits of compound interest

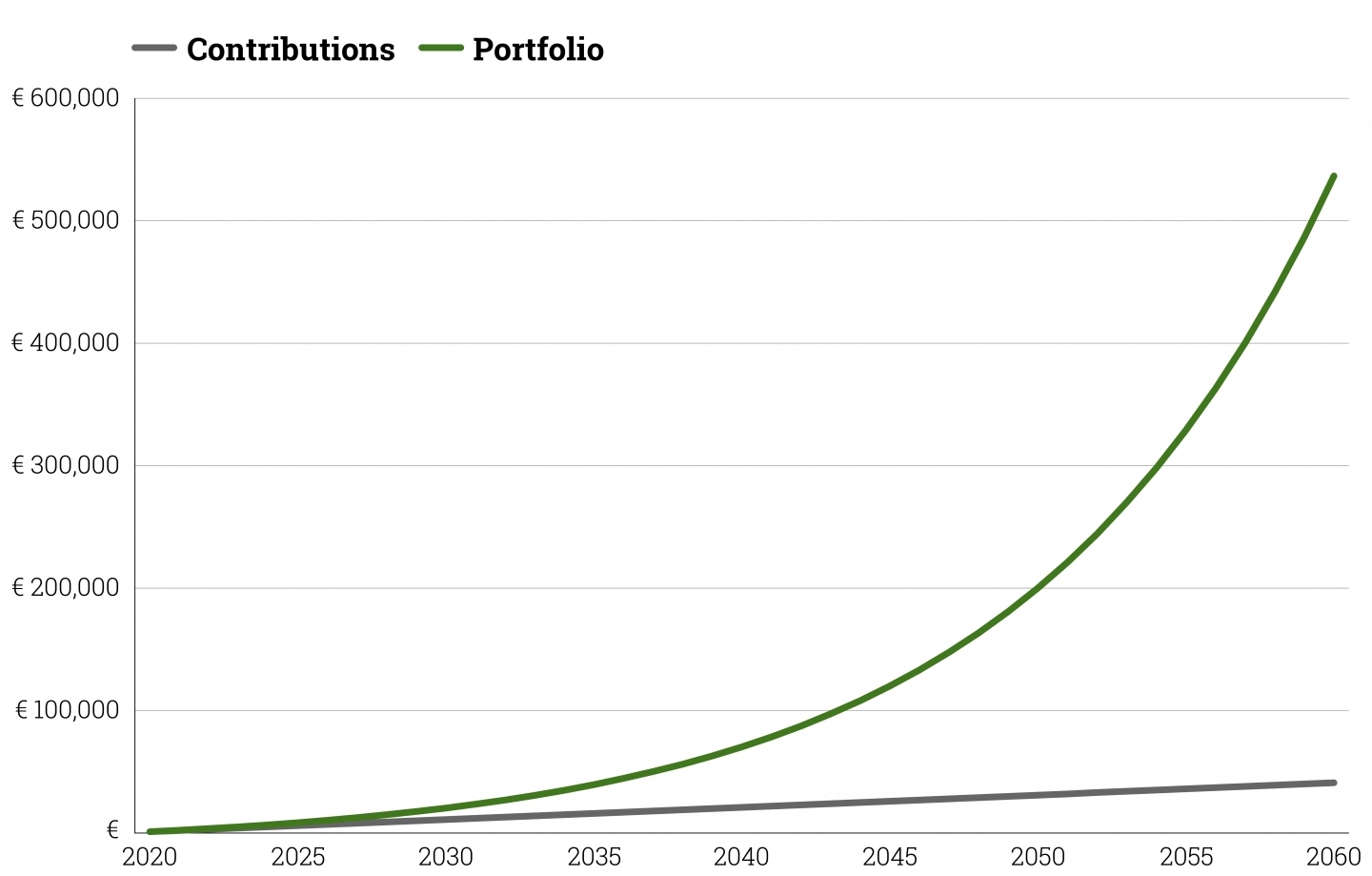

The majority of our readers will be aware of the benefits of compound interest. But it’s important to go over it again. Let’s suppose that a Spanish citizen receives a typical salary, i.e. the average of all salaries in Spain. That’s approximately 18,000 euros gross per year, of which we will have about 16,000 net. Let’s assume that said citizen manages to save 1,000 euros each year of their professional career and, for the sake of simplicity, their salary never goes up.

Let’s now imagine that this citizen is an avid reader of our blogs and a regular follower of Value School, so they have decided to invest in a 100% variable income pension plan. We should remember that it’s the most profitable asset of the last 200 years.

To conclude this imaginary scenario, given that the return has been 10% for that asset class, we’re going to use that return for our average citizen.

As we can see from the graph, after a life of saving and investment, our average citizen will be able to retire with a financial cushion that will allow them to live in peace. They won’t have to worry about whether or not the State can guarantee them a pension, since thanks to many years of sowing, watering and letting it grow continuously, they will be able to pay for their retirement all by themselves.

The consequence of being patient is that the contributions they’ve made will be a small percentage of their capital at the end of the period. The main thing is to let the capital work for you, to be patient and without interrupting the effect of compound interest.

That’s why I’m convinced that starting early is the biggest advantage. It’s also why I encourage everyone to start as soon as possible, because it’s never too late and it’s also not too early to start at a young age.

We could undoubtedly carry out this process of saving and investment using other products available on the market. Investment funds are a great alternative, but they don’t have a number of advantages that pension plans do.

The main advantages include:

Tax benefits, since the contributions made to a pension plan reduce the tax base of the income tax return.

When it comes to redemption, pension plans allow for three options: redemption in the form of capital, in the form of income or both, in a mixed way, as decided by the saver, and according to the specifications of the plan.

The main disadvantage we have to bear in mind is its illiquid nature. This is because it can only be redeemed in certain circumstances. This, of course, is a major drawback if we find ourselves in need of funds. On the contrary, it’s a major advantage for anyone who plans in the right way.

Sometimes we may think about saving to be able to treat ourselves to something in the future that we can’t currently afford. By saving through a pension plan, we know that we can overcome our consumerist tendencies. Not being able to redeem the money without a good reason will ensure that the money will be there for retirement and not be wasted along the way.

However, some of these advantages have been under threat as of late. More specifically, the draft Spanish National Budget for 2021 establishes that the maximum personal income tax deduction for pension plans will be reduced from 8,000 euros to 2,000.

It was certainly very beneficial for all savers and some of them will miss it. But it’s also true that most people didn’t take full advantage of the tax benefit.

In conclusion, I would like to encourage readers that during this final part of the year when compulsive shopping tends to dominate our lives, whether this is down to Black Friday discounts or Christmas approaching, to take the decision to avoid some of these purchases and to invest the money in a pension plan. It’s a matter of starting to water the tree that will give us shade in a time yet to come.

Did you find this useful?

- |