Investment is often counterintuitive. We have to fight a lot of bias if we want our investment to succeed. Even more so in the complex and slightly unstable economic environment in which we live: tensions around the world (Brexit, trade wars, etc.), the debt bubble, signs of deceleration in some of the main economies… These are all situations that generate much noise that can sometimes fuel our fears.

In the face of this fear, investors, of course, aim to protect their assets, generally through liquidity or fixed income. But, is that the right thing to do? The purpose of this article is to analyse—from the perspective of a value investor (buy cheap, invest money that you do not a priori need and focus on the long term)—some of the key fears that we face as participants in funds and to use empirical data to gauge whether they are founded or not.

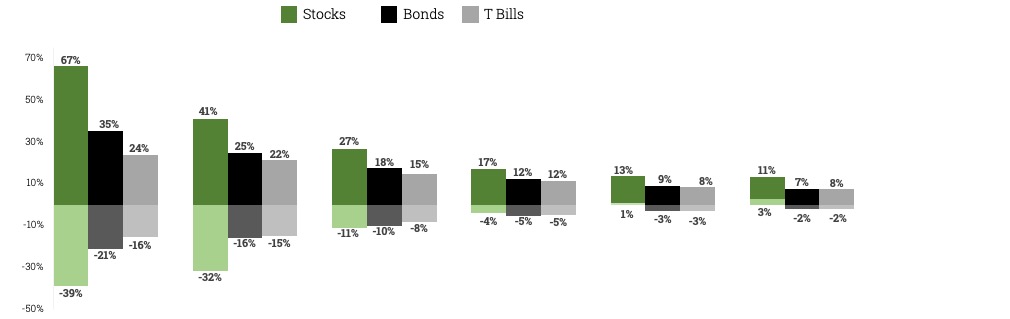

The first thing that may scare us is volatility or, in other words, big changes in the market over a short period of time. It is true that variable income is, by far, the most volatile instrument in the short term. But, although it is true that there might be severe changes in the short term, it is no less so that variable income is the safest asset in the long term, as it is the only instrument that guarantees a return on invested capital, as may be seen in the following chart:

Furthermore, another positive thing about volatility is that it causes temporary inefficiencies in the market that generate investment opportunities in companies that we can take advantage of. So, as long-term investors, should volatility concern us?

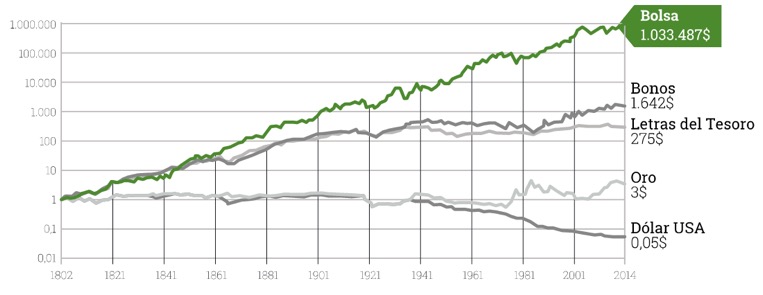

Equities in the long term are not just the safest instrument, they are also the most profitable. The table below shows a chart by Jeremy Siegel, where we can see the profitability obtained from a $1 investment in different types of assets in real terms from 1802 to 2014:

So far, we have seen that variable income is not just the safest instrument in the long term, but it is also the most profitable one by far. Is it not every investor’s dream to maximise profitability with minimum risk?

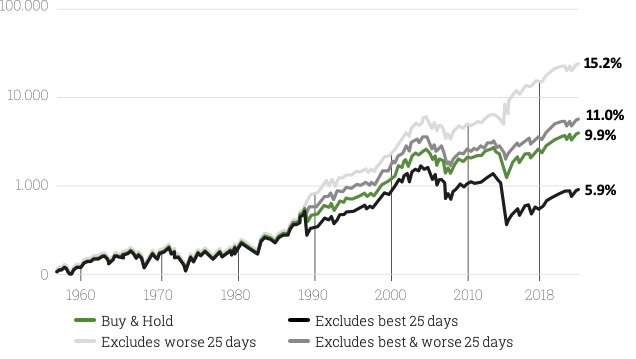

Another fear we face as investors is one that tempts us to try and anticipate market behaviour to avoid steep drops or recessions and so protect our assets. The chart below provides an analysis of different scenarios and how they affect profitability:

Looking at this chart, we can see that best and worst days have a huge effect on profitability. Therefore, and because it is statistically highly unlikely (if not impossible) that we can get market timing right at this concentration, it also transforms our investment into a game of chance and may really drag down the profitability of our investment.

A final factor that may scare us as investors is that ‘value’ assets are going through a bad time in comparison with ‘growth’ assets: This means that, while certain shares—growth shares—are listed with very high prices, our companies are very cheap (p/e for the Selección portfolio at the end of September was 5.9x). In fact, as we can see in the chart below, it is the first time in history there has been this much polarisation between both company ratings:

So, why should we continue to trust in values disfavoured by the market? For several reasons:

- We are contrarians. We go to the sectors and companies that nobody wants and we wait for the market to recognise their value because, although slow, the market is efficient. If we want to generate above-usual profitability, we cannot replicate what the rest of the market is doing.

- Companies generate profits over time, and if this does not feed through to the share price, then the company accumulates a value that increases its upside potential every day. The greater its potential, the greater the likelihood of somebody recognising the value.

So, we can see that, when it comes to investment, time is on our side. Our work involves finding values that allow us to improve in the long term the already-good data offered by the market. So, at the end of September, the Selection portfolio has a potential of over 150%, with very strongly competitive positions and entry barriers (average ROCE of 26%), many with net cash or little financial risk and with management teams aligned with our interests (66% of the portfolio companies have a majority shareholder), some of whom are even repurchasing shares. These numbers combined with qualitative analysis of our portfolio businesses means we can look towards the future with confidence.

Where there is conviction, we must be disciplined and patient. Paraphrasing the renowned Warren Buffett: “The stock market is a device for transferring money from the impatient to the patient.” Let us forget certain fears and wait, as there are few areas of our lives where time is on our side.

Did you find this useful?

- |