INTERNATIONAL PORTFOLIO

As noted in our previous letter, we are struggling to find sufficient quality companies at attractive prices in our natural environment of Europe, meaning that our position in non-European companies is higher than normal. We also have a somewhat greater focus on companies in the commodities business, especially in some sectors with capital needs, such as maritime transport.

Commodity companies have the added advantage of providing the portfolio with a particularly effective defence against the possible negative consequences of central bank monetary manipulation.

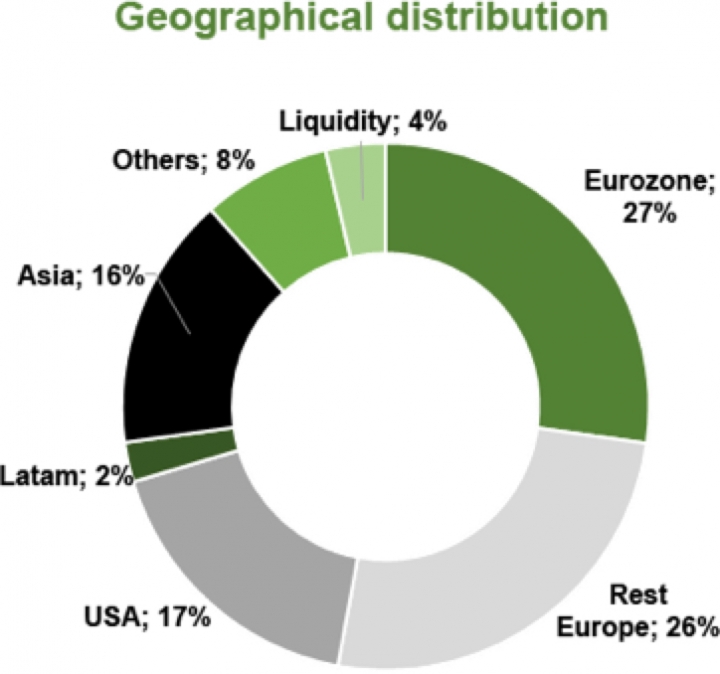

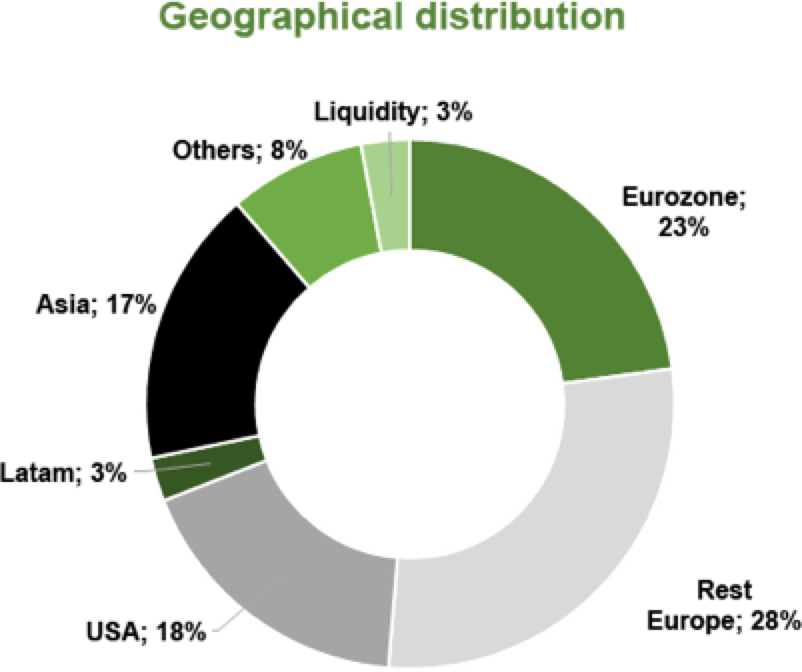

Overall, the geographic distribution of the portfolio has not changed significantly over the quarter, maintaining a strong exposure to companies outside of Europe and the Eurozone.

Currency impacts

We took a decision at the start of the year to hedge part of our dollar exposure in light of the attractive opportunities on offer in the region. We estimate that Purchasing Power Parity (PPP) for the dollar/euro is around 1.25-1.30. We intend to unwind this hedge once we reduce our exposure to the dollar or when the exchange rate closes in on this PPP anchor.

However, we are not planning to cover our investment in other currencies given that the overall impact is smaller and there is a natural hedge.

Notwithstanding, currency developments have led to a -4.19% impact on our model portfolio, the Cobas Selección fund, since the start of the year.

IBERIAN PORTFOLIO

Thanks to the adjustment in the Spanish market and negative news regarding some companies, we have uncovered some new attractive stocks, boosting the potential upside to 40%.

Over the course of the quarter we have taken stakes in companies which have almost all seen a degree of decline in their share price, bringing them into attractive territory from a purchase perspective.

We have significantly increased our position in Técnicas Reunidas, a high-quality company which we have been following for some time. The loss of two contracts provoked an exaggerated decline in its share price (21.02% in the quarter), which we have exploited to increase its weight in our portfolio.

Unicaja is a different case, where exceptionally for us we decided to take part in the Initial Public Offering. The fact that the seller was to some degree “forced” to sell, mitigated the usual problem associated with this type of transaction where the seller typically has much more information than the buyer. In any case, both the asset – a reasonably well-managed bank – and the price were attractive.

OUR FUNDS

COBAS SELECCIÓN F.I.

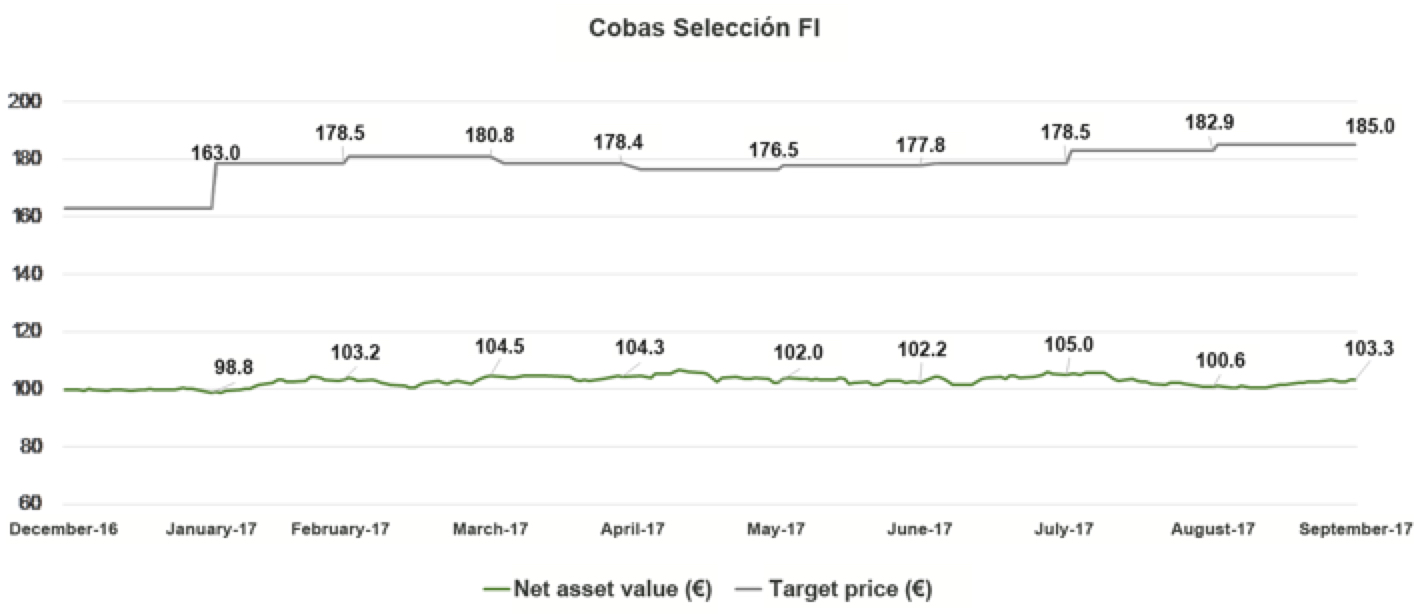

The fund posted a positive return of 1.13% over the quarter, compared to a 2.70% increase in the benchmark MSCI Europe Net Total Return index. Net asset value stood at 103.34 euros per share.

The Cobas Selección fund has posted a 3.54% return since 31 December 2016 compared to a 9.55% increase in the benchmark index.

Our target value for the Cobas Selección fund is 185 euros per share, well above the current net asset value and representing potential upside of over 80%. We have continued to raise the value of the portfolio over the quarter and we expect that this will be reflected over time in its net asset value.

Assets under management to 30 September amounted to 826.7 million euros, reaching a total of 10,061 shareholders.

Currency

The currency impact continues to hamper the performance of the portfolio with 75% invested outside of the euro area. The strong euro had a -0.98% impact on the quarterly outturn and has subtracted -4.19% since the start of the year.

We have the feeling of swimming upstream: the strong performance of our stocks is being offset by currency developments which have impaired the overall return.

In this regard, we would like to shed some light on the results obtained to date; while our stock selection has yielded satisfactory results, it has been penalised by unfavourable currency developments.

As discussed in our previous quarterly letter we are only hedging our significant position in dollars. For the remaining currencies, we expect the companies to adjust over time to a weaker currency and benefit from it over the medium-term, meaning we do not see any logic in short-term hedging given the cost involved. Furthermore, prior experience – for example 2002-03 – tells us that movements between the main currencies tend to autocorrect leading to a neutral impact over the long-term.

Portfolio

The Cobas Selección fund is our model portfolio, around 90% is invested in the international portfolio and 10% in the Iberian portfolio.

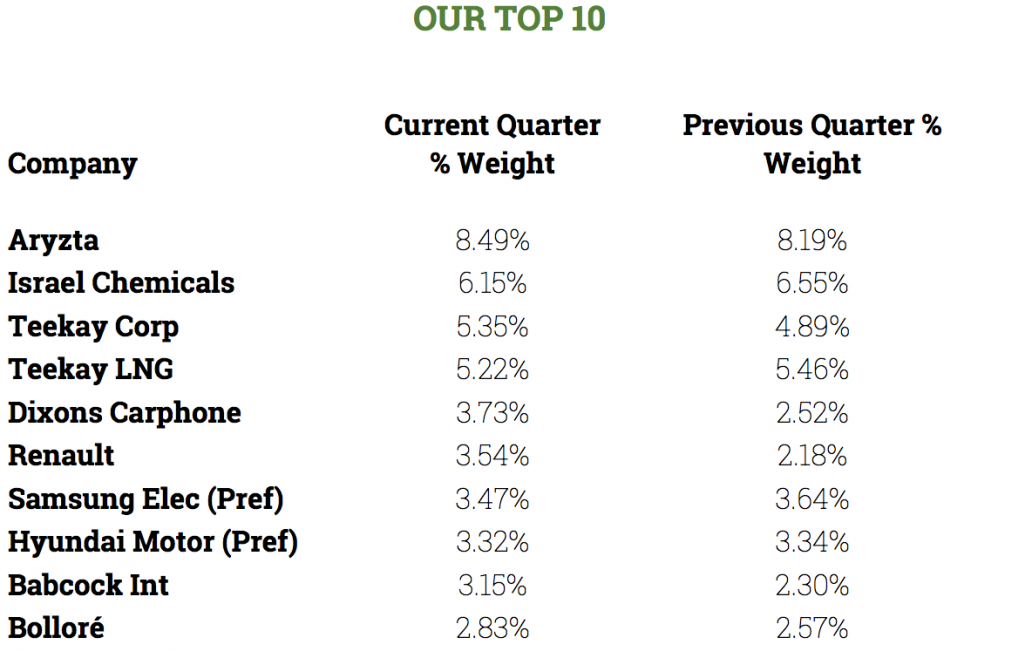

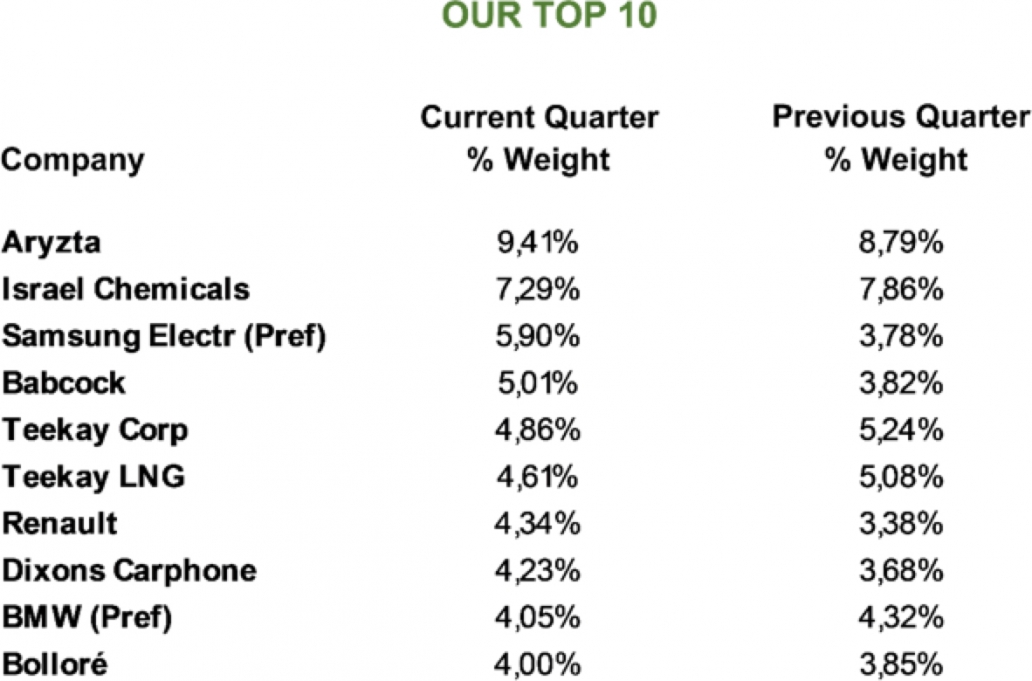

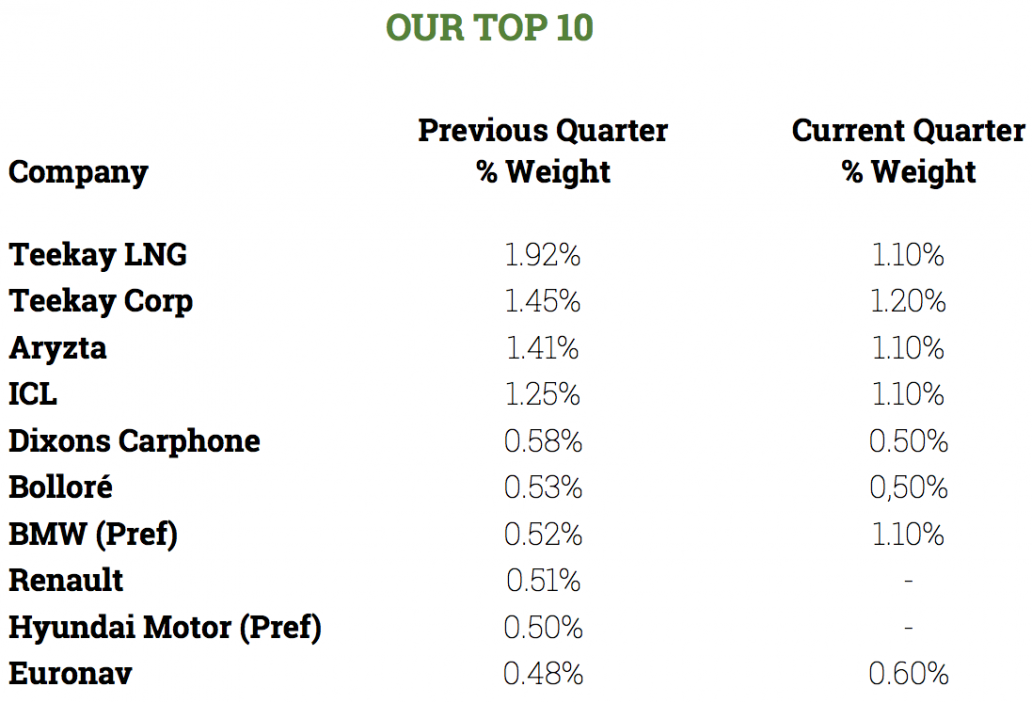

The weights of the main stocks have not changed significantly, with Aryzta, the Teekay group and ICL our top three investment picks, with a combined weight of around 25%.

The geographic distribution has not changed significantly over the quarter either, maintaining a strong exposure to companies outside of Europe and the Eurozone. While this is impairing our short-term performance due to the strong euro, we are confident this approach will yield attractive returns in the future.

Stock movements

We have sold various stocks over the quarter, some attaining relatively significantly upsides: Maire Technimont, Dassault Aviation, OVS, BW Offshore, EVN and Beni Stabili, while we have offloaded others despite not seeing significant movements: Next, Ralph Lauren, B2Gold, Gold Fields and Travis Perkins.

The logic underpinning all these sales is their lower potential upside relative to the alternative stocks which we have purchased: Porsche, Catcher Technologies, International Seaways, Greene King, Mitchells and Butler, QGEP and Spectrum. We expect upsides of between 50% and 100% in all these stocks.

Target value

The most positive development in this quarter has been the continued improvement in the target prices of the funds.

The estimated target value of Cobas Selección has increased from 177.8 to 185 euros per share. Therefore, the potential upside has risen to over 80% relative to 74% in the previous quarter.

Three main factors are behind this increase in intrinsic value: the increase in some target prices, the mere passage of time and the swapping of stocks with lesser upside for higher upside stocks, which will be discussed in the following section and is the essence of what we do.

The largest upward revision to our target value is in Samsung Electronics pref. The excellent performance by the company’s three main segments – storage, mobile phones and screens – together with a gradual improvement in corporate governance encourages us to be more optimistic about the company’s target value. The company is also sitting on an enormous stockpile of cash, which affords peace of mind should one of these areas underperform.

We also remain very upbeat about our two main positions and news over the summer has corroborated our conviction in them.

In terms of the Teekay group, after receiving support for its offshore subsidiary, we now await the entry into operation of its new LNG boats. All these boats have long-term contracts and will generate the necessary cash flow to significantly boost dividends in 2018 or 2019.

Aryzta has managed to stem the deterioration in its results and established the basis for a turnaround. Both we and the company’s competent new management team are confident this will happen given the quality of the business where it is a global leader.

The increase in the target value of the portfolio comes despite revising down our target prices for two important stocks, Dixons and Hyundai Motor pref.

We have significantly reduced our outlook for Dixons following a warning from the company that earnings from its telephone subsidiary, Carphone Warehouse, which accounts for 40% of the total, were set to disappoint. They gave two main reasons for this: a lengthening of replenishment times for telephones – it is unclear whether this will be temporary or permanent – and growth in SIM cards without an associated contract, which is less profitable for the company than selling a phone with a contract with an operator.

Even so, Dixons is still a clear leader in its other business lines – sales of electronic products in UK and Nordic countries – and growth here remains in line with expectations. Therefore, despite the downward revision, our estimate of the company’s value still remains well above the current share price and we have slightly increased our position in the company, which is trading at a P/E ratio of 7.3x.

Regarding Hyundai, we have decided to adjust our valuation of the car sector, following an in-depth study of the industry, which has also led us to invest in Renault and Porsche. The most significant conclusion of this research is that we now attach somewhat less value to the companies’ cash positions, since we think it is unlikely that shareholders will reap the full benefit. The uncertainties and investment needs facing these companies are leading them to be more conservative in this regard.

The impact of Hyundai’s enormous cash position on our valuation is very significant, which is why the reduction is particularly notable here. Even so, the upside potential remains very high (in line with the fund) and similar to our other three investments in the sector. BMW is the fourth company.

As we explained during our Value School seminar on 10 October using the example of Renault, the sector is currently very attractive following three years of mediocre market performance. The latter has been fuelled by concerns over the cycle in the United State and Europe (which only represents 30% of the global market) and the migration towards electric vehicles, especially Tesla. We think these concerns are totally unjustified. Applying prudent assumptions regarding sales in Europe and the United States, the first risk is mitigated by growth in other markets. Furthermore, even if Tesla were to be wildly successful and sell two million cars in 2022 (unlikely since it has yet to show it can manufacture on a large scale and it does not have a clear significant competitive advantage, since the battery which is the fundamental component of an electric car is developed by Panasonic), the global market would still be around 110 million units. In other words, Tesla would have a 2% share of a market where the other manufacturers have already announced plans to have a strong exposure to electric cars. It does not look like a serious threat.

As a result, we believe the sector’s relatively poor performance over the last two years will change, given the quality of its assets, sound balance sheets, more market-oriented management and an attractive price.

Regarding the Iberian equity investments in the portfolio, thanks to the adjustment in the Spanish market and negative news regarding some companies, we have uncovered some new stocks with attractive upside.

During the quarter we have taken a position in Unicaja – unusually for us we decided to participate in the Initial Public Offering. The fact that the seller was to some degree “forced” to sell, mitigated the usual problem associated with this type of transaction where the seller typically has much more information than the buyer. In any case, both the asset – a reasonably well-managed bank – and the price were attractive.

We have also built up a position in Técnicas Reunidas amounting to 1% of the portfolio. This is a high-quality company, which we have been following for some time. The loss of two contracts provoked an exaggerated decline in its share price (21.02% in the quarter), which we have exploited to increase its weight in our portfolio.

Overall, the portfolio is trading at a P/E ratio of 8.0x and a ROCE of 28% with a high potential upside since – as explained in our introductory letter in January – share prices invariably trend towards the intrinsic value of their underlying assets, which is the basis of our estimated target values.

COBAS INTERNACIONAL F.I.

The fund posted a positive return of 1.04% over the quarter, compared to a 2.70% increase in the benchmark MSCI Europe Net Total Return index. Net asset value stood at 99.20 euros per share.

Since its inception the Cobas Internacional fund has posted a negative return of -0.80% compared to a 5.34% increase in the benchmark index.

The target value for the Cobas Internacional portfolio is 180 euros per share, a long way above its current net asset value, representing potential upside of over 80%. We have continued to raise the value of the portfolio over the quarter, which is the essence of what we do, and we expect that this will be reflected over time in its net asset value.

Assets under management to 30 September amounted to 353.8 million euros, reaching a total of 5,188 shareholders.

Currency

Currency developments continue to hamper the performance of the international portfolio with 75% invested outside of the euro area. The strong euro had a -1.16% impact on the quarterly outturn and has subtracted -3.29% since the start of the year.

We have the feeling of swimming upstream: the strong performance of our stocks is being offset by currency developments which have impaired the overall return. Since we began investing in January through Cobas Selección, the impact of non-euro exposure has resulted in a loss of 4.19%.

In this regard, we can shed some light on the results obtained to date; while our stock selection has yielded satisfactory results, it has been penalised by unfavourable currency developments.

As discussed in our previous quarterly letter we are only hedging our significant position in dollars. In the remaining currencies, we expect the companies to adjust over time to a weaker currency and benefit from it over the medium-term, meaning we do not see any logic in short-term hedging given the cost involved. Furthermore, prior experience – for example 2002-03 – tells us that movements between the main currencies tend to autocorrect leading to a neutral impact over the long-term.

Portfolio

The Teekay group made the largest positive contribution (+2.16%) over the quarter boosted by an association with the Brookfield group in its offshore oil activity, which has eliminated market concerns regarding the subsidiary’s financial situation. Meanwhile, Dixons (-0.93%) performed particularly poorly, which we will discuss in more detail below.

It is worth emphasising the concentration in the portfolio with ten stocks accounting for 50% of the portfolio. This means that movements in the portfolio will not necessary be correlated with wider market developments and will instead occur as the companies take forward their business plans and the market wakes up to their value.

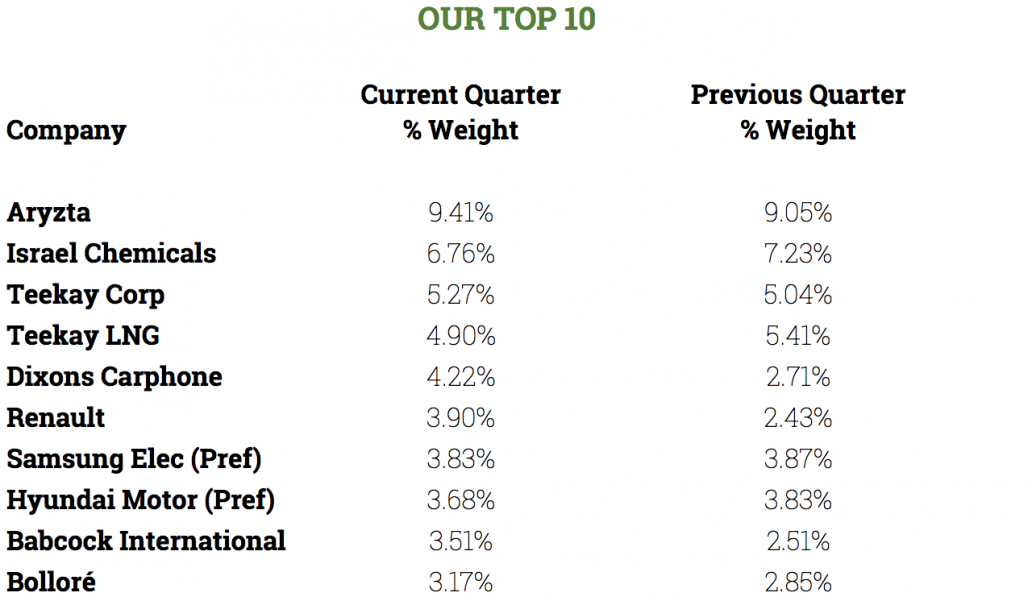

The weights of the main stocks have not changed significantly, with Aryzta, the Teekay group and ICL our top three investment picks, with a combined weight of over 25%.

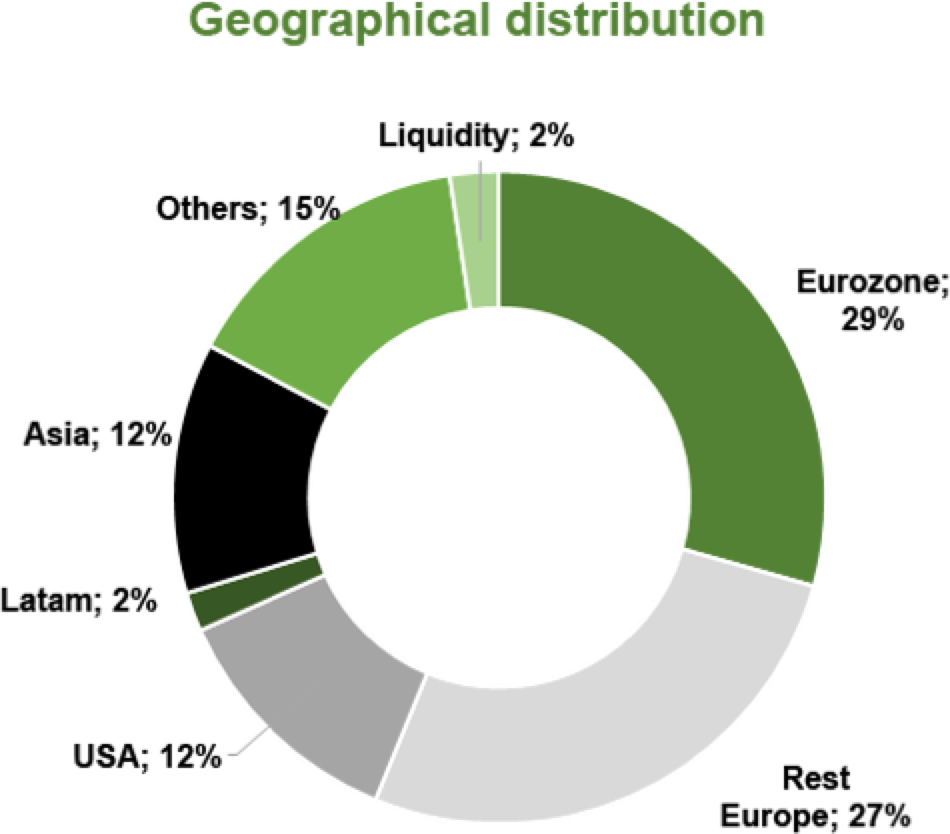

The geographic distribution has not changed significantly over the quarter either, maintaining a strong exposure to companies outside of Europe and the Eurozone. While this is impairing our short-term performance due to the strong euro, we are confident this approach will yield attractive returns in the future.

Stock movements

We have sold various stocks over the quarter, attaining relatively significantly upsides: Maire Technimont, Dassault Aviation, OVS, EVN y Beni Stabili, and have offloaded others despite not having seen significant movements: Next, Ralph Lauren, B2Gold, Gold Fields and Travis Perkins.

The logic underpinning all these sales is their lower potential upside relative to the alternative stocks which we have purchased: Porsche, Catcher Technologies, Greene King, Mitchells and Butler, QGEP and Spectrum. We expect price increases of between 50% and 100% in all these stocks.

Target value

The most positive development in this quarter has been the continued improvement in the target prices of the funds.

The estimated target value of the international portfolio has increased from 173.8 to 180.3 euros per share. Therefore, the potential upside of the fund is over 80%.

Three main factors are behind this increase in intrinsic value: the increase in some target prices, the mere passage of time enabling the companies to accumulate earnings and the swapping of stocks with lesser upside for higher upside stocks, which as we have discussed in previous occasions is the essence of what we do.

The largest upward revision to our target value is in Samsung Electronics pref. The excellent performance by the company’s three main segments – storage, mobile phones and screens – together with a gradual improvement in corporative governance encourages us to be more optimistic about the company’s target value. The company is also sitting on an enormous stockpile of cash, which affords peace of mind should one of these areas underperform.

We also remain very upbeat about our two main positions and news over the summer has corroborated our conviction in them.

In terms of the Teekay group, after receiving support for its offshore subsidiary, we now await the entry into operation of its new LNG boats. All these boats have long-term contracts and will generate the necessary cash flow to significantly boost dividends in 2018 or 2019.

Aryzta has managed to stem the deterioration in its results and established the basis for a turnaround. Both we and the company’s competent new management team are confident this will happen given the quality of the business where it is a global leader.

The increase in the target value of the portfolio comes despite revising down our target prices for two important stocks, Dixons and Hyundai Motor pref.

We have significantly reduced our outlook for Dixons following a warning from the company in August that earnings from its telephone subsidiary, Carphone Warehouse, which accounts for 40% of the total, were set to disappoint. They gave two main reasons for this: a lengthening of replenishment times for telephones – it is unclear whether this will be temporary or permanent – and growth in SIM cards without an associated contract, which is less profitable for the company than selling a phone with a contract with an operator.

Even so, Dixons is still a clear leader in its other business lines – sales of electronic products in UK and Nordic countries – and growth here remains in line with expectations. Therefore, despite the downward revision, our estimate of the company’s value still remains well above the current share price and we have slightly increased our position in the company, which is trading at a P/E ratio of 7.3x.

Regarding Hyundai, we have decided to adjust our valuation of the car sector, following an in-depth study of the industry, which has also led us to invest in Renault and Porsche. The most significant conclusion of this research is that we now attach somewhat less value to the companies’ cash positions, since we think it is unlikely that shareholders will reap the full benefit. The uncertainties and investment needs facing these companies are leading them to be more conservative in this regard.

The impact of Hyundai’s enormous cash position on our valuation is very significant, which is why the reduction is particularly notable here. Even so, the upside potential remains very high (in line with the fund) and similar to our other three investments in the sector. BMW is the fourth company in the sector.

As we explained during our Value School seminar on 10 October using the example of Renault, the sector is currently very attractive following three years of mediocre market performance. The latter has fuelled concerns over the cycle in the United State and Europe (which only represents 30% of the global market) and the migration towards electric vehicles, especially Tesla. We think these concerns are totally unjustified. Applying prudent assumptions regarding sales in Europe and the United States, the first risk is mitigated by growth in other markets. Furthermore, even if Tesla were to be wildly successful and sell two million cars in 2022 (unlikely since it has yet to show it can manufacture on a large scale and it does not have a clear significant competitive advantage, since the battery which is the fundamental component of an electric car is developed by Panasonic), the global market would still be around 110 million units. In other words, Tesla would have a 2% share of a market where the other manufacturers have already announced plans to have a strong exposure to electric cars. It does not look like a serious threat.

As a result, we believe the sector’s relatively poor performance over the last two years will change, given the quality of its assets, sound balance sheets, more market-oriented management and an attractive price.

Overall, the portfolio is trading at a P/E ratio of 7.8x and a ROCE of 29% with a high potential upside, since – as explained in our introductory letter in January – share prices invariably trend towards the intrinsic value of their underlying assets, which is the basis of our estimated target values.

COBAS IBERIA F.I.

The fund posted a -1.23% return over the quarter compared to a 1.67% increase in the benchmark index composed of 75% I.G.B.M. Total and 25% PSI 20 Total Return. Net asset value stood at 107.97 euros per share.

Since its inception the Cobas Internacional fund has posted a return of 7.98% compared to a 4.78% increase in the benchmark index.

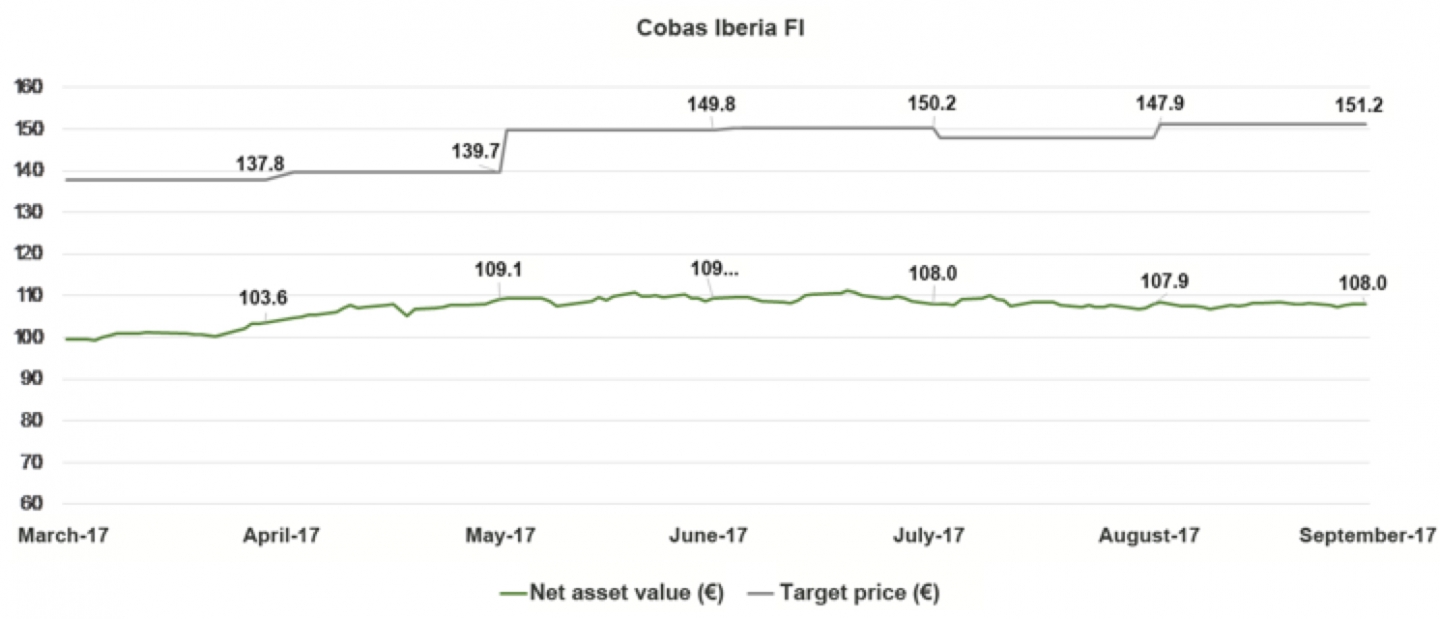

Our target value for the Cobas Iberia fund is 151.2 euros per share, well above the current net asset value and representing potential upside of close to 40%. We have continued to raise the value of the portfolio over the quarter and we expect that this will be reflected over time in its net asset value.

Assets under management to 30 September amounted to 40.7 million euros, reaching a total of 1,404 shareholders.

Portfolio

Despite a positive contribution from the two oil companies in the portfolio – Repsol (+0.67%) and Galp (+0.59%) – the performance of other stocks, especially the other oil sector company, Técnicas Reunidas (-1.26%), led the fund to post a negative return over the quarter.

The portfolio remains stable, although we have increased our positions in Técnicas Reunidas, Telefónica, Euskaltel and Tubacex taking advantage of declines in their share prices.

We have significantly increased our position in Técnicas Reunidas, a high-quality company which we have been following for some time. The loss of two contracts provoked an exaggerated decline in its share price (21.02% in the quarter), which we have exploited to increase its weight in our portfolio.

The increase in our position in Euskaltel is smaller but nonetheless significant. We are talking about a stable business capable of generating recurring earnings. The drop in the company’s share price (18.3% over the quarter) has been the impetus for this movement.

Stock movements

During the quarter we have taken stakes in Almirall, Bankia, Unicaja, Sacyr and Mapfre. Nearly all these companies have seen a degree of significant decline in their share prices bringing them into attractive territory from a purchase perspective. Unicaja is a different case, where exceptionally for us we decided to take part in the Initial Public Offering. The fact that the seller was to some degree “forced” to sell, mitigated the usual problem associated with this type of transaction where the seller typically has much more information than the buyer. In any case, both the asset – a reasonably well-managed bank – and the price were attractive.

We have offloaded three stocks: Telepizza, Rovi and Merlin, since we believe the existing stocks in the portfolio plus the new additions have greater upside potential.

Target value

The target value of the portfolio has increased slightly to 151.2 euros per share.

Thanks to the adjustment in the Spanish market and negative news regarding some companies, we have uncovered some new stocks with attractive upside enabling us to be almost fully invested.

However, the relatively small increase in the target value is because we have lowered our estimates for some of the main stocks in the portfolio, such as Elecnor, Técnicas Reunidas and Vocento.

We currently see potential upside of 40% with a P/E ratio of 11.8x and ROCE of 23%.

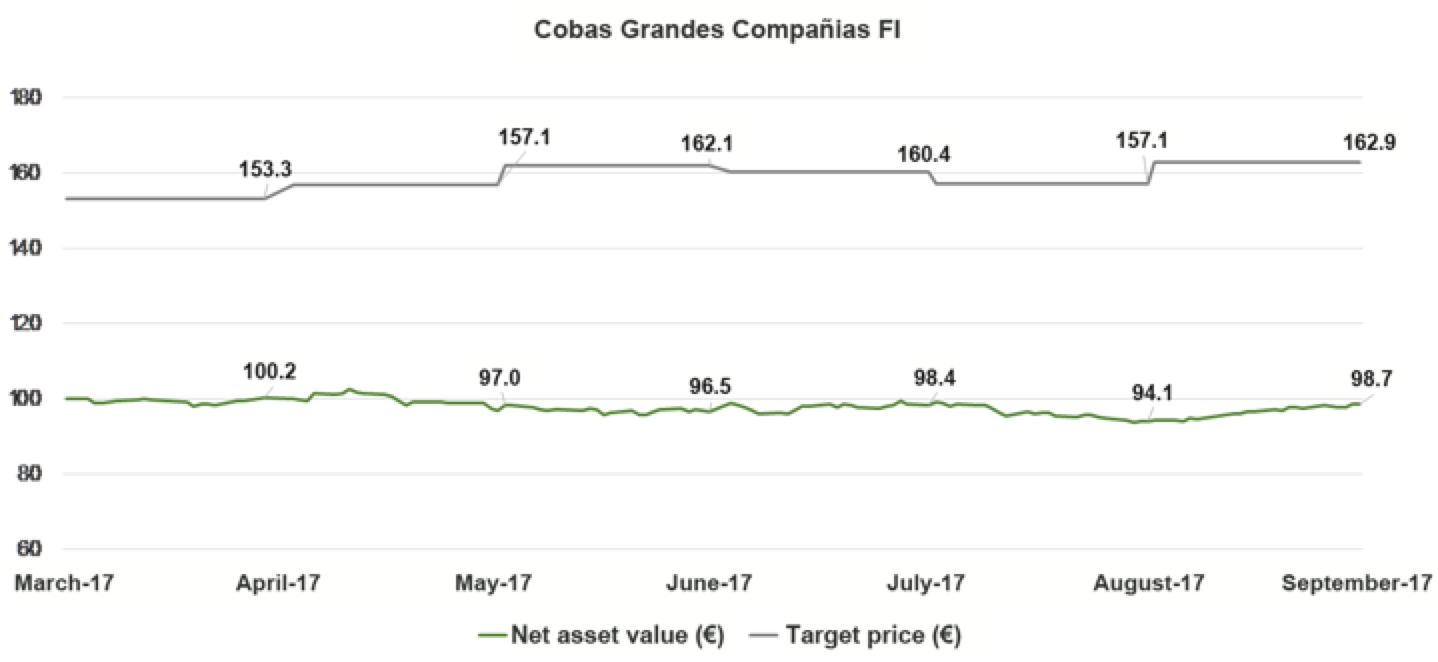

COBAS GRANDES COMPAÑÍAS F.I.

The fund posted a 2.29% return over the quarter compared to a 1.15% increase in the benchmark MSCI World Net EUR index. Net asset value stood at 98.70 euros per share.

Since its inception the Cobas Grandes Compañías fund has posted a return of -1.30% compared to a -1.40% fall in the benchmark index.

The impact from currencies continues to impair the returns achieved by the portfolio. The strong euro had a -0.54% impact on the quarterly outturn and has subtracted -2.95% since the start of the year. In this instance, the benchmark index has also been affected by euro depreciation.

The target value for the Cobas Grandes Compañías portfolio is 162.9 euros per share, a long way above its current net asset value, representing potential upside of over 65%. We have continued to raise the value of the portfolio over the quarter, which is the essence of what we do, and we expect that this will be reflected over time in its net asset value.

Assets under management to 30 September amounted to 17.3 million euros, reaching a total of 599 shareholders.

Portfolio

The fund registered a positive performance over the quarter, in line with its benchmark index. Teekay Corporation (+1.73%) made the largest positive contribution, while Dixons (-1.20%) performed poorly.

The weights of the main stocks have not changed significantly, with Aryzta, the Teekay group and ICL our top three investment picks, with a combined weight of over 25%.

The geographic distribution has not changed significantly over the quarter either, maintaining a strong exposure to companies outside of Europe and the Eurozone. While this is impairing our short-term performance due to the strong euro, we are confident this approach will yield attractive returns in the future.

Stock movements

We have sold various stocks over the quarter, attaining relatively significantly upsides: Easyjet, Gilead Sciences, Daiwa Industries, Thyssenkrupp, and offloaded others despite not having seen significant movements: Next, Ralph Lauren and Travis Perkins.

The logic underpinning all these sales is their lower potential upside relative to the alternative stocks which we have purchased: Porsche, Catcher Technologies, Bayer AG and Shire PLC. We expect price increases of between 50% and 100% in all these stocks.

Target value

The target value of the portfolio has increased slightly to 162.9 euros per share.

The companies in the portfolio continue to have a very positive outlook, with a potential upside of over 65%, resulting from the attractive prices at which they are trading – overall P/E ratio of 8.2x – and their underlying quality, with an average ROCE of 28%.

COBAS RENTA F.I.

The portfolio posted a positive return of 0.17% over the quarter. Net asset value stood at 99.58 euros per share.

Since inception, the Cobas Renta fund has achieved a return of -0.42%.

The strong euro had a -0.02% impact on the quarterly outturn and has subtracted 0.09% since the start of the fund.

Faced with a backdrop of a financial market where central banks are taking monetary manipulation to the extreme, Cobas Renta has to fight against negative nominal and real interest rates, which hamper efforts to obtain reasonable returns for fixed income investors. Fortunately, our management fee is the lowest on the market, at 0.25%, which provides a degree of relief.

Assets under management to 30 September amounted to 21.5 million euros, reaching a total of 384 shareholders.

As always, we complement short-term fixed income with a modest investment in equities (up to 15% of assets).

This includes the key companies in Cobas Selección and we hope that over the long-term this will prove sufficient to compensate inflation and our fees, at least maintaining investors’ short-term purchasing power.

During the quarter we requested authorisation to invest up to 5% of assets in sub-investment grade bonds. The goal is to take advantage of occasional opportunities to add value to the portfolio.

Did you find this useful?

- |