International Portfolios

During the fourth quarter, international portfolios obtained returns above 6%, and coincidentally we have continued to increase their target value. Currently, the upside potential for the international portfolio is 86% and for large companies it is 60%.

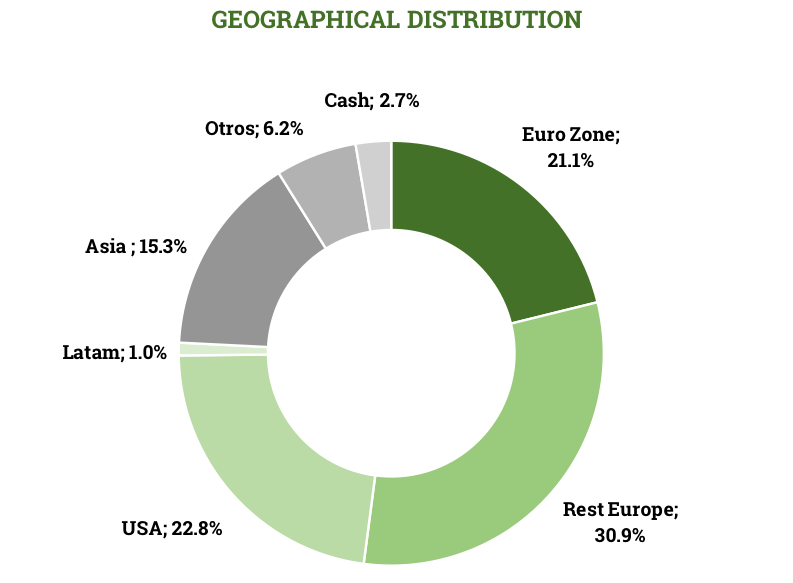

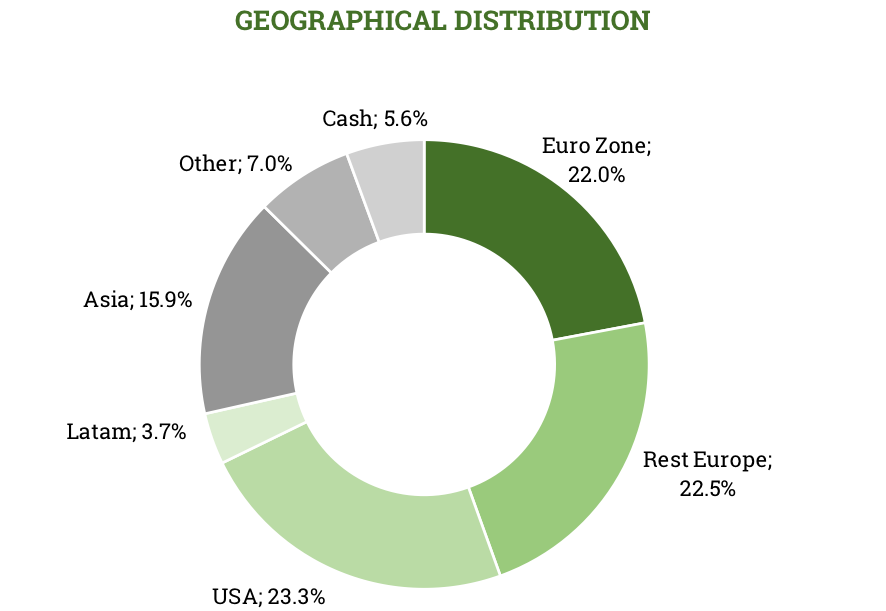

In terms of geographical distribution, this did not change significantly during the quarter, with the exception of the Cobas Grandes Compañias FI fund, in which we increased exposure outside of Europe and the Euro zone, to the detriment of these areas.

In this quarter we highlighted our trip to Asia to visit the Japanese companies and some of the Korean companies that we have in the international portfolio. An important part of the portfolio is invested in Asia and it is in our best interest to be close to the companies.

Iberian Portfolio

In the case of the Iberian portfolio, the revaluation obtained in the last quarter of the year was more than 2%. We have continued to increase the target value of this portfolio, with the upside potential standing at 39%.

During the quarter we reduced the exposure to Portugal to 20%, from the 26% we had at the end of the previous quarter.

Our Funds

COBAS INTERNACIONAL F.I.

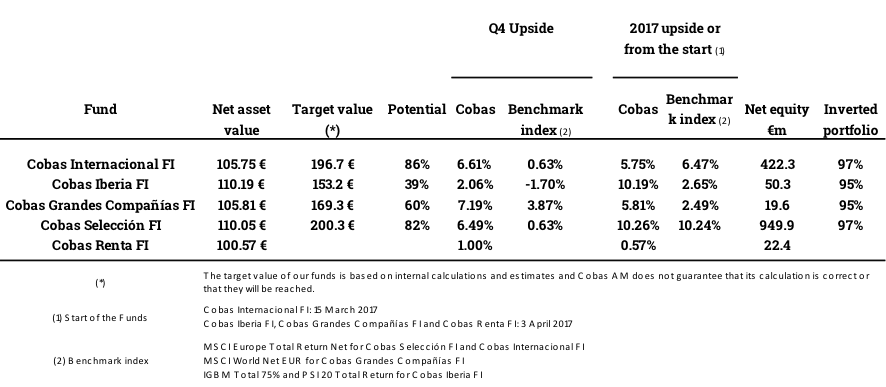

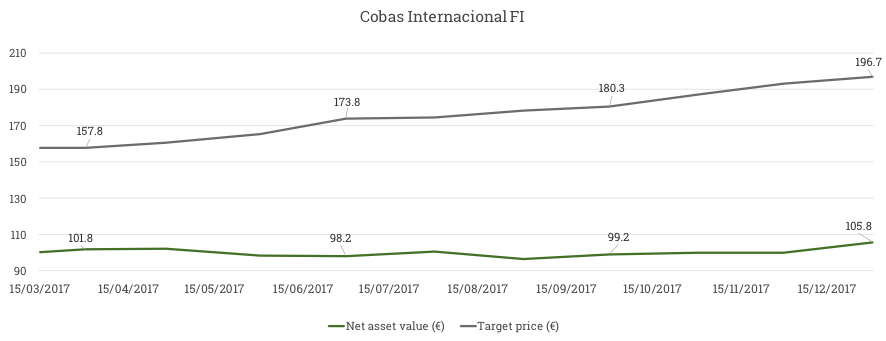

Cobas Internacional FI posted a return of 6.61% in the fourth quarter, compared to a 0.63% increase in the benchmark MSCI Europe Net Total Return index. Net asset value as of 31 December stood at 105.75 euros per share.

Since the Cobas Internacional FI fund began investing in equities in mid-March, it has obtained a return of 5.75% despite the 4% negative impact as a result of the revaluation of the Euro, already mentioned in the previous quarter. The benchmark index was revalued by 6.47%.

The target value for the portfolio is €196.70/share, a long way above its current net asset value, with potential upside of 86%. We have continued to raise the value of the portfolio over the quarter and we expect that this value will continue to be reflected over time in its net asset value.

Obviously, and as a result of this potential, we are invested to 97%, close to the legal maximum allowed of 99%. Assets under management to 31 December amounted to 422.3 million euros, reaching a total of 5.781 shareholders.

Portfolio

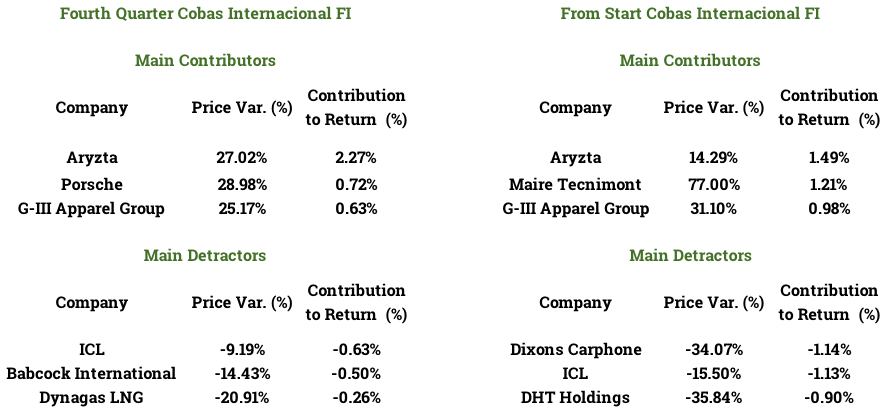

During the quarter, and also since the start, the greatest contribution to the positive result has been that of Aryzta (+ 2.27%), where the publication of results together with the positive news on sales of non-essential assets and the extraordinary dividend of its subsidiary Picard, have contributed to the beginning of the recovery of its share price and the reduction in our exposure. However, during January, the company announced a profit warning, suffering a drop in the share price. Both, the company and ourselves, think it is a temporary problem (Due to a sudden rise of the costs in USA), which will not affect the valuation of the company in the long term. On the negative side is ICL (-0.63%) and Babcock International (-0.50%), the latter penalised by a mistaken market perception about its competitive advantages.

The weights of the main stocks have not changed significantly, with Aryzta, the Teekay group and ICL our top three investment picks, with a combined weight of close to 25%.

The geographic distribution has not changed significantly over the quarter either, maintaining a strong exposure to companies outside of Europe and the Eurozone. While this is impairing our short-term performance due to the strong euro, we are confident this approach will yield attractive returns in the future.

We still have 100% of the dollar exposure hedged.

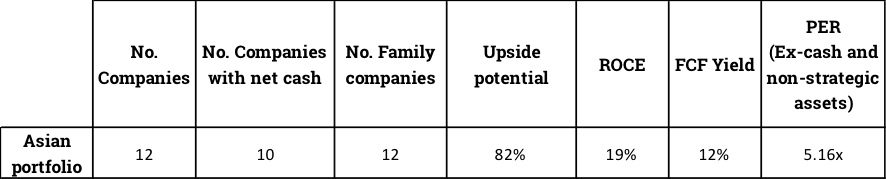

Investment in Asia

As Mingkun Chan explained in a recent blog, we spent a week in Japan in December, visiting our Japanese companies and some of the Korean ones. An important part of the portfolio is invested in Asia and it is in our best interest to be close to the companies, which we can do thanks to Mingkun.

This high investment percentage is derived from the high prices in Europe and the United States, our natural markets, and, on the other hand, from the very attractive valuations of our Asian businesses.

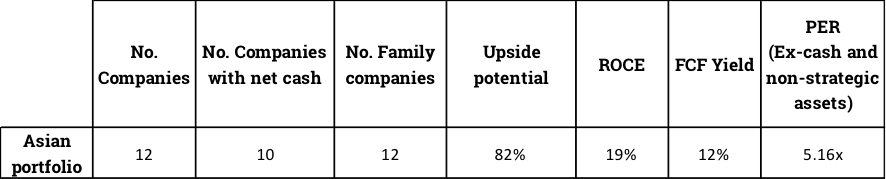

Below are the main characteristics of the Asian companies in portfolio at the end of December:

This allows us to be careful with our investments in Europe and the rest of the world, because we do not need to buy assets that are not clearly undervalued.

One of the companies we visited during our trip to Japan was Daiwa Industries. Its weight on 31 December at Cobas Internacional FI was 1.88%. We have already visited them twice in Osaka.

It is a family business, with 42% of the capital in the hands of the Ozaki family, whose business consists of manufacturing industrial refrigeration equipment, which it sells to restaurants, hospitals, retail shops, etc.

The 4 main competitors in Japan have consolidated their market share in recent years and accumulate around 75% of that quota.

It is a good business with a ROCE of more than 50% and stable sales growth of around 3-4% per year.

It is a business with high entry barriers given the customisation required by kitchens and the wide portfolio of products to be offered in order to be competitive. It is necessary to have a good and fast pre-sales and after-sales service (24 hours a day, 365 days a year) since, being cold machines, customers can not wait due to the type of products they keep. For more than 20 years, we had an investment experience in Spain in the sector, specifically in Ibérica del Frio (Koxka), one of the sector leaders in Spain.

In the case of Daiwa, it is a company with a net cash / market capitalisation percentage of approximately 64%. It is trading at a P/E ratio of 5x, while its biggest competitor (Hoshizaki) trades at 20 times profit.

Stock movements

Although the main values of the portfolio have remained stable, there have been variations in the secondary values. This quarter we sold several securities, some with more or less significant revaluations (Exor, Gaztransport, Howden Joinery, Kroton, LG Household, Rieter and Tesco), and others, despite having no major movements (Gaslog Partners, Phosagro and Polymetal).

The logic underpinning all these sales is their lower potential upside relative to the alternative stocks which we have purchased: Costamare Inc, Exmar, Fugro, Golar LNG, Kongsberg Grupp, LG Corp Prefs., Mylan, NS Shopping, Petra Diamonds, Petrofac, TechnipFMC and Teva. We expect upsides of between 50% and 100% in all these stocks.

The Teekay Tankers shares come from out stock holding in Tanker Investments. By merging both companies, we have received shares from the first.

Target value

As has been the recurrent factor throughout the year, the most positive development in this quarter has been the continued improvement in the target prices of the funds.

The estimated target value of the international portfolio has increased from 180.3 to 196.7 euros per share. Therefore, the potential upside of the fund is 86%.

The most significant valuation increase occurred in automobile securities, with an average increase of 15%, since we have used somewhat less conservative but more realistic assumptions.

Meanwhile, the net purchases have had an impact on securities with more potential, as is logical.

Overall, the portfolio trades at a P/E ratio 9.2x and an ROCE of 28%.

COBAS IBERIA F.I.

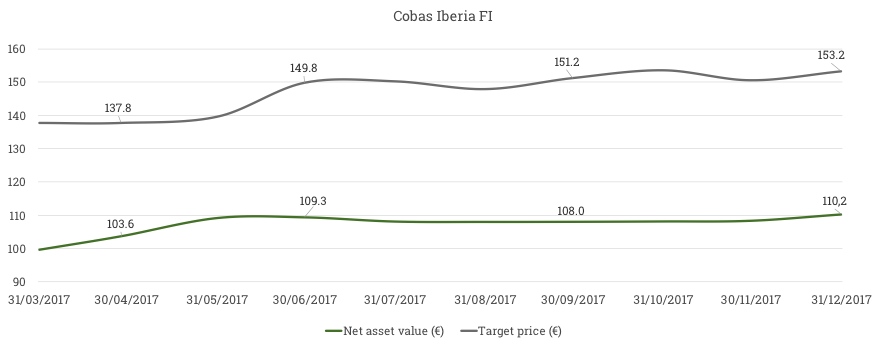

The return from Cobas Iberia FI during the fourth quarter was 2.06% compared to a loss of 1.70% for the benchmark index comprised by I.G.B.M. Total of 75% and a 25% PSI 20 Total Return. Net asset value stood at 110.19 euros per share.

Since Cobas Iberia FI fund began investing in equities at the beginning of April, the return has been 10.19% compared to an upside of 2.65% for the benchmark index.

The target value of the fund is above the net asset value, €153.2 /share, with an upside potential of 39%. We have slightly increased the value of the portfolio over the quarter and we expect that this will be reflected over time in its net asset value.

We continue with a high percentage of investment in shares, of around 95%. Assets under management to 31 December amounted to 50.3 million euros, reaching a total of 1.640 shareholders.

Portfolio

This quarter, as has happened since the start of the fund, the largest contributor of profitability in the Iberian portfolio was Elecnor (+ 1.11% in the quarter). Likewise, the contribution of Quabit during the last quarter of the year is also noteworthy, contributing 0.64%. Telefónica is the main detractor of profitability (-0.69%).

The portfolio remains stable, although we have continued to increase positions in Técnicas Reunidas, Telefónica, Euskaltel, Quabit, Sacyr and CTT – Correios de Portugal, taking advantage of the price drops. We have also slightly reduced the weight of Elecnor, our main position during a large part of the year, taking advantage of the strong revaluation that it has had in 2017.

We have significantly increased our position in Técnicas Reunidas. This is a high quality company, which we have been following for some time. The loss of 2 contracts at the start of the year and the delay in the granting of 3 other large contracts has caused a short-term fall in margins, as there was an overlap between income, temporarily lower, and fixed costs, which resulted in the profit warning” (or warning that it was not going to reach the expected results) of November, provoking an exaggerated fall in the price over the last 6 months, which we used to increase its weight in the portfolio. The levels before the profit warning were recovered in January.

The increase in our position in Euskaltel has also been significant. We are talking about a stable business capable of generating recurring earnings. The drop in the company’s share price (18.3% in the third quarter and 9% in the last quarter) has been the impetus for this movement.

We are also positive with the real estate sector and increase exposure to the cycle through Quabit. It is a company with a reference shareholder that is quoted at a discount on the value of its assets, since part of them do not include the price increase that has occurred in the big cities. In December we went to the capital increase due to the discount with which the operation was made.

Stock movements

During the quarter we have taken stakes in: Indra, Merlin and Parques Reunidos. We have offloaded two stocks: Galp y Viscofan, since we believe the existing stocks in the portfolio plus the new additions have greater upside potential.

Target value

The target value of the portfolio has increased slightly to 153.2 euros per share.

We currently see potential upside of 39% with a P/E ratio of 11.0x and ROCE of 24%.

COBAS GRANDES COMPAÑÍAS F.I.

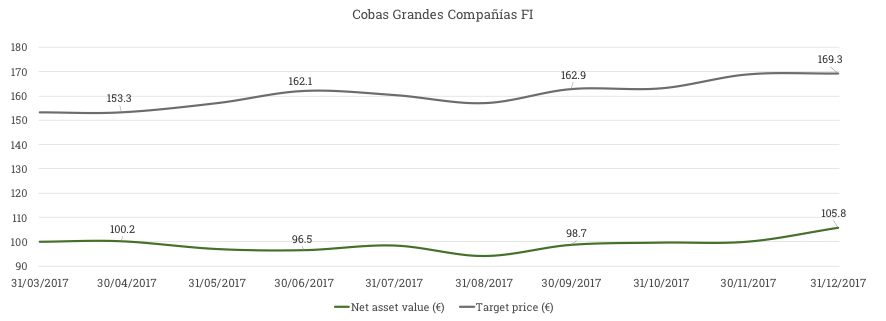

The return from Cobas Grandes Compañías FI during the quarter was 7.19%, against an upside of 3.87% for the reference index, MSCI World Net EUR. Net asset value of Cobas Grandes Compañías stood at 105.81 euros per share.

Since the Cobas Grandes Compañías FI fund began investing in equities at the beginning of April, the return has been 5.81% compared to an upside of 2.49% for the benchmark index.

The target value for the portfolio, €169.3/share, is a long way above its current net asset value, with potential upside of 60%.

We continue with a high percentage of investment in shares, of around 95%. Assets under management to 31 December amounted to 19.6 million euros, reaching a total of 664 shareholders.

Portfolio

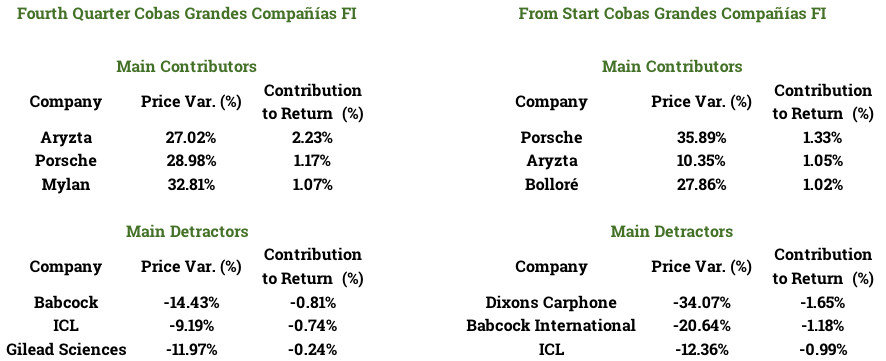

The company that contributed the most to the positive return of the fund in the last quarter was Aryzta (+ 2.23%), while Babcock International (-0.81%) stood out in negative. However, we have taken advantage of the falls in the share price of the latter to increase its weight in the portfolio, as well as in other funds with an international vocation.

There has been a significant increase in the weight of Teva and Mylan, global leaders in generic medications. The incorporation of KT Corp., a Korean telecommunications company, among the top 10 securities, is also noteworthy.

Stocks with a market capitalisation of less than €4bn represent 18.55% of the portfolio.

In terms of geographical distribution, exposure to Europe was reduced during the quarter (both the Euro zone and the non-Euro zone), increasing especially the weight of the portfolio in the USA. from 12% to 23%, derived from the incorporation of new stocks in the portfolio and the increase in the weight of some American companies that were already in the portfolio, such as Teva Pharma, for example.

We still have 100% of the dollar exposure hedged.

Stock movements

We have sold the following stocks over the quarter: Bayer, Continental, Euronav, Iliad, KPN, Taro Pharma, Vale. In general they have obtained revaluations that made them less attractive than the alternatives. In the particular case of Euronav, we have replaced it with International Seaways, a company in the same sector, but with greater appeal.

The new stocks in the portfolio are: Gilead Sciences, International Seaways, KT Corp., Petrobras, Petrofac, TechnipFMC, Telefonica and Thyssenkrupp.

Teva Pharma

Teva is the world leader in generic drugs, with a global share of 8%, and also has an important presence in innovative products related to neurodegenerative, respiratory and oncology diseases.

A poor management of the existing business, together with an aggressive acquisitions policy at the wrong time, caused the company to lose focus in the business at a crucial time for the sector (clients were consolidating, together with greater public pressure on the product prices), which generated more pressure (than the normal) in the prices of generic products. Furthermore, its most important innovative medicine (Copaxone) lost its patent in 2017. All these difficulties lead to expectations deteriorating and showing a weak balance with a Net Debt ratio to EBITDA (close to 5 times).

This caused shares to fall from a maximum of $70 in 2015 to $11 in November 2017. We, as usual, started buying too soon, but we took advantage of the drop to strongly increase our position.

Convinced that the sector has a future, because it is a sector that grows, due to the growth of the population, its ageing, and also due to the greater diagnosis and penetration of medicines in emerging markets, although with lower prices, together with the references of the new CEO, Kåre Schultz, which are extraordinary. As the COO of Novo Nordisk, the Chairman of the board of Royal Unibrew, and CEO of Lundbeck, the results show that he did a very effective job (just to mention the last case, his stage in Lundbeck, shares multiplied by 3 times from May 2015 to September 2017).

Based on this generated credibility, we are confident that he can carry out the announced restructuring without the need for dilutive capital increases, which makes the valuation of Teva, which is trading at a 6.25x P/E ratio at 31 December, very attractive.

Target value

The portfolio has increased its target value from 162.9 euros per share to 169.3 euros.

In addition to the aforementioned improvement in automobile-related companies for the international portfolio, the improvement of the Teva target price has been a special incident.

The companies in the portfolio continue to have a very positive outlook, with a potential upside of 60%, resulting from the attractive prices at which they are trading – P/E ratios of 7.5x – and their underlying quality, with an average ROCE of 27%.

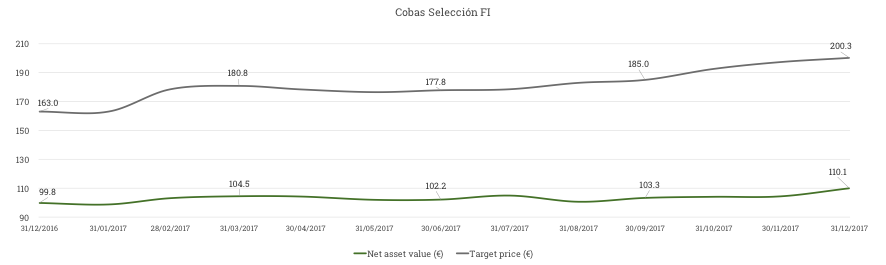

COBAS SELECCIÓN F.I.

The return from Cobas Selección FI during the last quarter of 2017 was 6.49% compared to an upside of 0.63% for the benchmark index, MSCI Europe Total Return Net. As of 31 December, the net asset value of Cobas Selección stood at 110.05 euros per share.

Since 31 December 2016, the fund’s return has been 10.26%, despite the negative impact of 4% as a result of the appreciation of the Euro, which was already mentioned in the previous quarter. The benchmark index was revalued by 10.24%.

The target value of the fund is €200.3/share, well above the net asset value, with an upside potential of 82%. We have continued to raise the value of the portfolio over the quarter and we expect that this value will continue to be reflected over time in its net asset value.

Obviously, and as a result of this potential, we are invested to 97%, close to the legal maximum allowed of 99%. Assets under management to 31 December amounted to 949.9 million euros, reaching a total of 10,989 shareholders.

Portfolio

Cobas Selección fund is our model portfolio, around 90% is invested in the international portfolio and 10% in the Iberian portfolio.

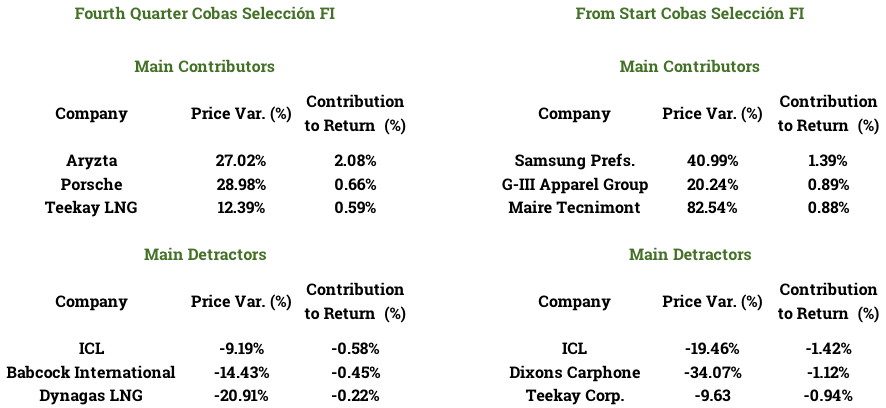

During the quarter, and also since the start, the greatest contribution to the positive result has been that of Aryzta (+ 2.08%), where the publication of results together with the positive news on sales of non-essential assets and the extraordinary dividend of its subsidiary Picard, have contributed to the beginning of the recovery of its share price and the reduction in our exposure. However, during January, the company announced a profit warning, suffering a drop in the share price. Both, the company and ourselves, think it is a temporary problem (Due to a sudden rise of the costs in USA), which will not affect the valuation of the company in the long term. On the negative side is ICL (-0.58%) and Babcock International (-0.45%), the latter penalised by a mistaken market perception about its competitive advantages.

The weights of the main stocks have not changed significantly, with Aryzta, the Teekay group and ICL our top three investment picks, with a combined weight of around 23%.

The geographic distribution has not changed significantly over the quarter either, maintaining a strong exposure to companies outside of Europe and the Eurozone. While this is impairing our short-term performance due to the strong euro, we are confident this approach will yield attractive returns in the future.

We still have 100% of the dollar exposure hedged.

Investment in Asia

As Mingkun Chan explained in a recent blog, we spent a week in Japan in December, visiting our Japanese companies and some of the Korean ones. An important part of the portfolio is invested in Asia and it is in our best interest to be close to the companies, which we can do thanks to Mingkun.

This high investment percentage is derived from the high prices in Europe and the United States, our natural markets, and, on the other hand, from the very attractive valuations of our Asian businesses.

Below are the main characteristics of the Asian companies in portfolio at the end of December:

This allows us to be careful with our investments in Europe and the rest of the world, because we do not need to buy assets that are not clearly undervalued.

One of the companies we visited during our trip to Japan was Daiwa Industries. Its weight on 31 December at Cobas Selección FI was 1.68%. We have already visited them twice in Osaka.

It is a family business, with 42% of the capital in the hands of the Ozaki family, whose business consists of manufacturing industrial refrigeration equipment, which it sells to restaurants, hospitals, retail shops, etc.

The 4 main competitors in Japan have consolidated their market share in recent years and accumulate around 75% of that quota.

It is a good business with a ROCE of more than 50% and stable sales growth of around 3-4% per year.

It is a business with high entry barriers given the customisation required by kitchens and the wide portfolio of products to be offered in order to be competitive. It is necessary to have a good and fast pre-sales and after-sales service (24 hours a day, 365 days a year) since, being cold machines, customers can not wait due to the type of products they keep. For more than 20 years, we had an investment experience in Spain in the sector, specifically in Ibérica del Frio (Koxka), one of the sector leaders in Spain.

In the case of Daiwa, it is a company with a net cash / market capitalisation percentage of approximately 64%. It is trading at a P/E ratio of 5x, while its biggest competitor (Hoshizaki) trades at 20 times profit.

Stock movements

Although the main values of the portfolio have remained stable, there have been variations in the secondary values. This quarter we sold several securities, some with more or less significant revaluations (Alba, Exor, Gaztransport, Howden Joinery, Inmobiliaria del Sur, Kroton, LG Household, Rieter, Tesco and Unicaja), and others, despite having no major movements (Gaslog Partners, Phosagro and Polymetal).

The logic underpinning all these sales is their lower potential upside relative to the alternative stocks which we have purchased: Costamare Inc, Euskaltel, Exmar, Fugro, Golar LNG, Kongsberg Grupp, LG Corp Prefs., Mylan, NS Shopping, Petra Diamonds, Petrofac, Quabit Inmobiliaria, Sacyr, TechnipFMC and Teva. We expect upsides of between 50% and 100% in all these stocks.

The Teekay Tankers shares come from out stock holding in Tanker Investments. By merging both companies, we have received shares from the first.

Target value

As has been the recurrent factor throughout the year, the most positive development in this quarter has been the continued improvement in the target prices of the funds.

The estimated target value of Cobas Selección has increased from 185 to 200.3 euros per share. Therefore, the potential upside is 82%, compared to 79% in the previous quarter.

The most significant valuation increase occurred in automobile securities, with an average increase of 15%, since we have used somewhat less conservative but more realistic assumptions.

Meanwhile, the net purchases have had an impact on securities with more potential, as is logical.

Overall, the portfolio trades at a P/E ratio 9.2x and an ROCE of 29%.

COBAS RENTA F.I.

Cobas Renta FI posted a positive return of 1.00% over the quarter. Net asset value of Cobas Renta stood at 100.57 euros per share.

Since inception, the Cobas Renta fund has achieved a return of 0.57%.

Faced with a backdrop of a financial market where central banks are taking monetary manipulation to the extreme, Cobas Renta has to fight against negative nominal and real interest rates, which hamper efforts to obtain reasonable returns for fixed income investors. Fortunately, our management fee is the lowest on the market, at 0.25%, which provides a degree of relief.

Assets under management to 31 December amounted to 22.4 million euros, reaching a total of 398 shareholders.

As always, we complement short-term fixed income with a modest investment in equities (up to 15% of assets).

This includes the key companies in Cobas Selección and we hope that over the long-term this will prove sufficient to compensate inflation and our fees, at least maintaining investors’ short-term purchasing power.

In the last quarter, we requested authorisation to invest up to 5% of assets in sub-investment grade bonds. This quarter we have requested authorisation to raise the limit to 10% of the fund’s assets. The goal is to take advantage of occasional opportunities to add value to the portfolio.

For this reason, we have purchased corporate bonds from Exmar and Teekay Corp, taking advantage of the attractive prices at which they were listed.

MIFID Regulation

In accordance with Markets in Financial Instruments Directive, known as MIFID II and its development regulations, Cobas, as management company, intends to assume the costs arising from analysis services provided by financial intermediaries, included so far in the brokerage fees and trading commissions and supported by the investment funds.

We remain at your disposal for any further question in the phone number +34 900151530 or international@cobasam.com.

Best regards

Investors Relations Team of Cobas Asset Management

Did you find this useful?

- |