The winter season is starting and high electricity and energy prices are on everyone’s mind. It seems to be a situation that we have suddenly found ourselves in. However, it is something that has been a few years in the making.

The main reason for this energy crisis is the global increase in the prices of natural gas and other energy-related raw materials. In both the US and Europe they have reached multi-year highs, to the extent that comparisons with the oil crisis of the 1970s are not as far-fetched as some might think.

In order to understand this whole situation, the reasons must be sought in structural causes and not simply a whim of the market. Markets other than energy, such as fertilisers and ethanol production, could be affected by the structural increase in gas prices, adding to the supply chain disruptions faced by companies.

Moreover, if it holds – and this obviously depends on weather and geopolitics – US and especially European households could be in for a very expensive winter, as gas inventory levels are at multi-year lows.

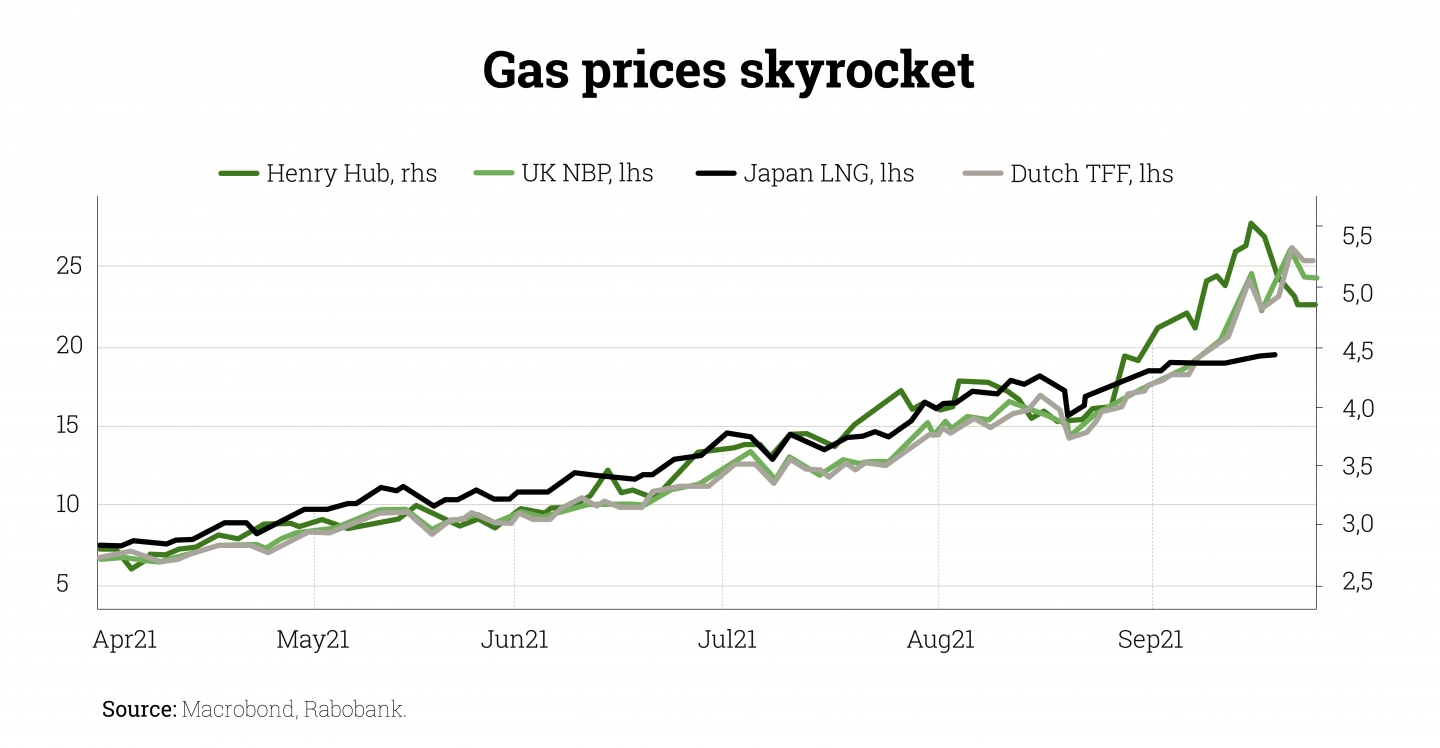

The energy sector and, in particular, the natural gas markets have seen the most explosive price increases. Natural gas prices in Europe and Asia have become parabolic, rising by more than 200% in Europe and 150% in Asia in a matter of months. This compares with increases of almost 100% in US benchmark prices. So what is behind these steep and staggering price increases?

A “fad” or something that was a long time coming?

Broadly speaking, the recent movement in world natural gas prices has been a long time in the making, and it is likely that structurally higher natural gas prices are here to stay. The main reason is the sharp slowdown in US natural gas production, the engine of global natural gas supply growth over the last decade thanks to the fracking revolution. In fact, it was practically swimming in natural gas until a few years ago, when it started to increase LNG export capacity.

However, things have changed dramatically in recent months, and the US is no longer increasing supplies, and production remains far from pre-pandemic peaks. At the same time, global demand continues to rise as the world seeks to move towards a carbon-free future. At present, this ambitious goal is simply not feasible without natural gas as an important bridge away from dirtier fuels such as coal and oil. As a result, global natural gas supply and demand balances are extremely tight and storage levels are critically low ahead of the high-demand winter months.

If the worst-case scenario is realised, the world’s storage facilities would be virtually empty in a cold winter scenario. This would be a catastrophic scenario that the market is trying to solve for now by raising prices so much that demand is forced to ration. We are beginning to see this dynamic in real time, as fertiliser facilities and other industries are forced to close in Europe as a direct consequence of high natural gas prices. This should help alleviate demand, with important side effects, such as the threat of food shortages in the UK due to lack of fertiliser, but so far no supply relief is in sight.

The supply chain disruptions that the world has witnessed since Covid, in sectors such as semiconductor manufacturing, now have their own equivalent in the natural gas crisis. Firstly, electricity suppliers are being hit hard, especially if they have not sufficiently hedged their purchases. This already seems to be a reality in the UK.

In addition, gas shortages also highlight the dependence of other (energy) markets on gas, and those that rely heavily on electricity, which is a very long list.

Clear examples are ethanol production, which requires a lot of heating (using natural gas) to distil the alcohol. And the list goes on: aluminium production, (speciality) chemicals such as paint, refined products, plastics and food packaging.

Almost the entire economy is implicated in one way or another in a cascading effect, as we have seen in other areas of seemingly innocuous supply chain disruption.

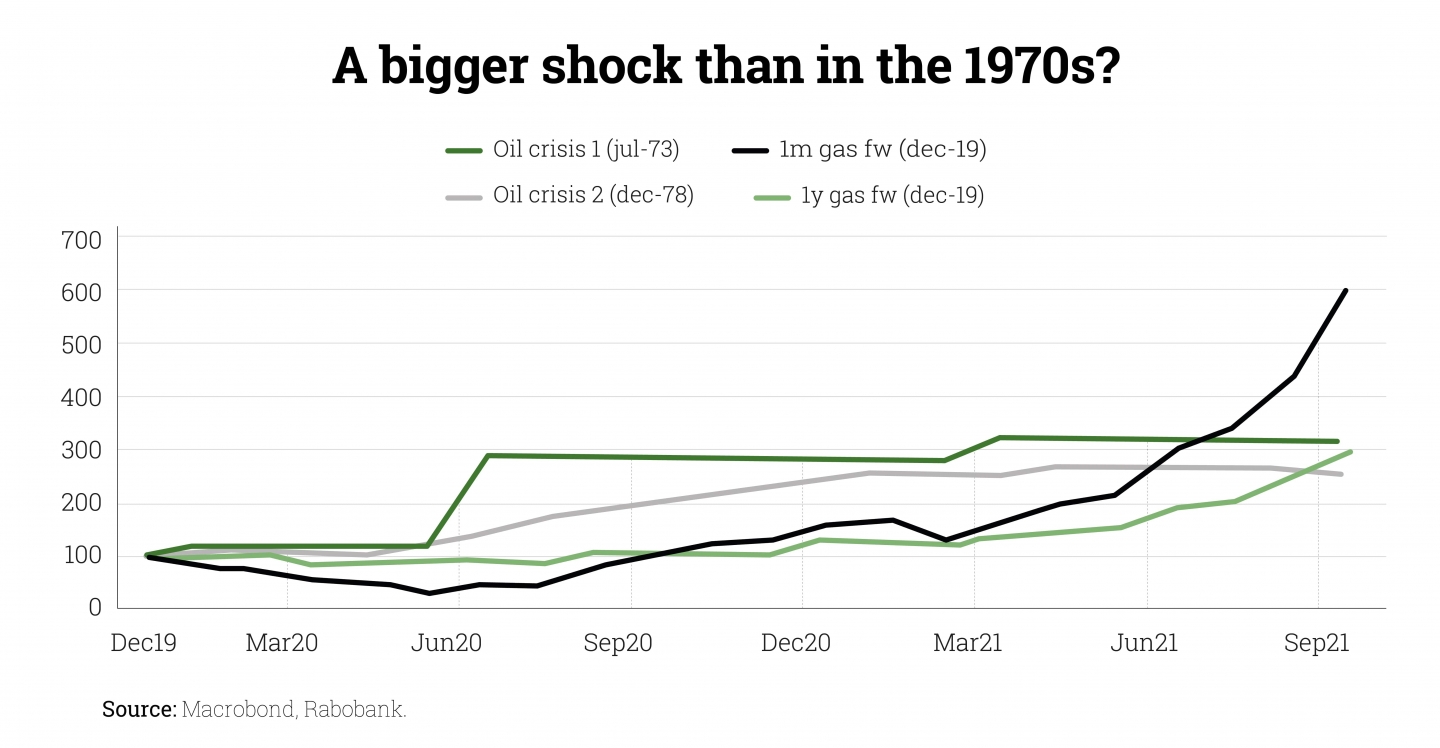

Moreover, to put the current gas price rise in perspective, it is interesting to compare its trajectory since the end of 2019 with the evolution of the oil price during the two major oil shocks in Figure 2. By these measures, the short-term price shock already exceeds those infamous episodes of the 1970s.

All this only strengthens certain trends that were already occurring globally. Inflation, which is gaining momentum, will be strengthened by this increase in the cost of energy. Supply chains will be further affected by cost increases in different parts of the supply chain.

There is only one protection left for us as savers and investors: to invest in real assets that can protect us from this coming inflation. As a result, we stand to benefit and will be able to profit from our exposure to the oil and gas industry. For example, our most production- or exploration-exposed companies because they will achieve record EBITDA and FCF levels, thanks to these commodity prices. The companies most exposed to facilities and engineering are also seeing their order books grow at much higher levels than in previous years, due to the expressed need for investment in oil and gas infrastructure.

In conclusion, the most important thing is that our portfolio will be able to protect us from this temporary change, which has a structural background. It will protect us from upcoming inflation and we will be able to preserve our purchasing power in the long term.

Did you find this useful?

- |