Investment is a way of life, and the way of investing with which we feel most comfortable will fit our personality. This is why there are no investment philosophies better than others, but ones more suitable for us and the achieving of our goals.

At Cobas we have reached the end of the first three years of this project built on enthusiasm, commitment and honesty. It is not an easy period for those of us who are part of it. Especially for the investors, who, in the midst of the excellent work carried out during the almost 30 previous years, entrusted us with their savings. But it’s worth stopping for a second and thinking that we’re three years in, but have been here for 30.

In my case, in addition to the learning process that all investors go through when they decide to invest their savings, something that I experience first-hand as a Cobas investor, is having the good fortune of being able to learn from our shareholders by working in the s Investor Relations department, which gives me the opportunity to be in permanent contact with investors, a group in which I also have friends and members of my family.

Throughout these three years, I have had the opportunity to meet in person with many of our investors, and to contact hundreds of them in one way or another. And if there’s one thing I’ve got imprinted on my mind, it’s the importance of listening to shareholders. Feeling their worries and fears, or their peace of mind and trust.

My work is mainly based on understanding the shareholder, knowing what reasons led him or her to invest at Cobas, beyond the obvious search for long-term profitability. Furthermore, I work with the obligation to be transparent so that the shareholder understands the reasons that lead us to remain faithful to our investment process, even in the most complicated moments. And all this is to avoid being swept away by the masses, since, as we can see below, market volatility constantly tests us with traps along the way, in order to benefit from the profitability that the stock market generates in the long term.

So, regarding both of those things, we try to figure out whether what we do is in line with what they are looking for, because, truthfully, it may not be.

Here lies what is really important. Does this fit with what I am looking for? Is it in line with my personality and who I am? Do I feel comfortable putting the effort of a lifetime’s work into the hands of these people? And in this way, sitting in a hotel, in an office, or in a cafe in any town, we forget the profits for a while and try to look further forward. To understand exactly what we do here, why and what we are here for. And we do so as equals, because I’m in their shoes too. I have my savings with Cobas and, more importantly, I feel responsible for the savings of people who know me and who, partly trust my judgement, and have theirs here too. Savings as a result of daily effort and consistency over a lifetime.

During those conversations we came to many conclusions, but I’ll choose one: how hard it is to be different and to do things differently. Because let’s not kid ourselves, investing in Cobas is not the easiest option. It is not, plain and simple, because we do things differently from the rest and, for a long time, we have understood that one of the main biases that have led to us, as the human race, being here today, is none other than the herd bias, which in the investment world is a handicap.

On this difficulty, and many others, Daniel Kahneman and Amos Tversky published a series of articles related to the general area of judgement and decision-making. In their theories, the authors addressed a number of cognitive biases that affect human behaviour, one of which is herd bias, also known as the bandwagon effect. Essentially, it is a psychological theory according to which individuals adopt ideas or actions simply because a large majority of people have done so previously.

In my opinion, this is damaging for both managers and investors. In the financial markets, returns are obtained by buying assets and then selling them at a higher price. This is easier when these assets are acquired at a price well below their real value, despite the underlying difficulty of acting in a different direction or way from that chosen by the majority.

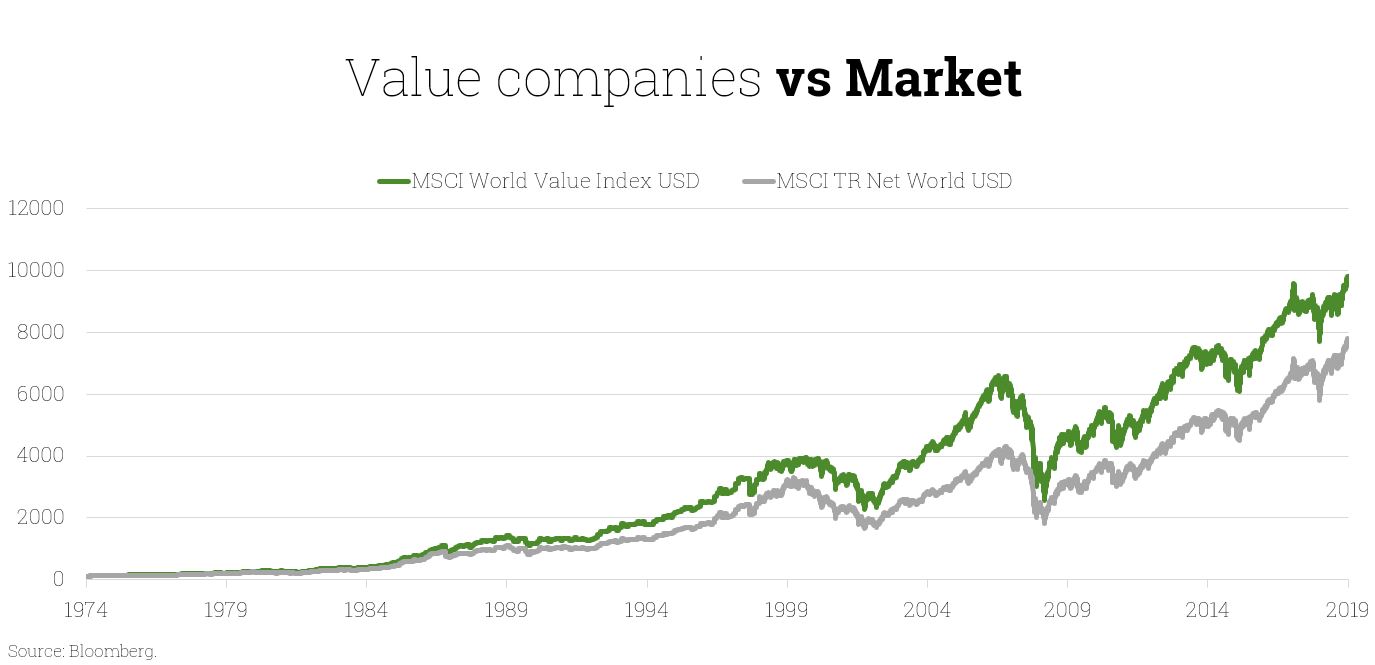

This is basically what value investing is all about. And, as we see in the following graph, it is a strategy that has historically offered returns above the market average:

I have often wondered why we make life so difficult for ourselves, instead of operating closer to the market. Because by approaching the market you avoid a lot of worries, because when things go wrong, they will go wrong for everyone and you will be there hidden among the majority. Whereas when it goes well, you’ll enjoy it with everyone, too. In short, by following the market you will always feel sheltered.

Well, I answer that question by looking at history and seeing how, throughout history, those who have stood out the most have been precisely those who have moved away from the herd and decided to be brave and consistent with their way of thinking. And history is very long. It isn’t written in two days, not even in three years. Don’t let anyone tell you that you can’t do something.

Speaking of brave people, today our shareholders are proving to be very brave, as well as very patient. It’s normal for you to have deep-seated doubts, always asking “what if”. Doubt is inherent to human beings, and is something not to be afraid of. You made a decision based on reasoning that you arrived by your own, and you did so by coming up with some goals, all of them aligned with the same objectives as us. So don’t let the trees stop you from seeing the depth of the forest, because it’s the same one we started planting almost 30 years ago. Nothing has changed, and we have the utmost confidence that our investments will bring us profits once again, which is why we are incredibly consistent and faithful to our investment process.

These last few weeks, there is a topic that has been taking up a large part of our meetings, since it is an element that has been affecting the market significantly in the last few days and is likely to continue. It’s the Coronavirus. In our opinion, this is a temporary situation that should not make us lose focus on the fact that our objective is not based on the short term.

We know that these risks are inherent in the market, and they are also difficult to predict, but we are also sure that they are temporary and that what really matters is the cash flow generated by our companies. These type of unforeseen events come, affect the market and disappear, and tomorrow others will come. We have seen them countless times, but our companies will continue to develop, paying dividends, buying back shares or reinvesting that cash in the business, so it’s really best to take advantage of these situations.

As I talk to many of you, I am sure that sooner rather than later, the day will come when we will sit down again in that hotel, office or cafe in any town and share anecdotes about the difficult times we lived through together.

Remember that patience is always rewarded.

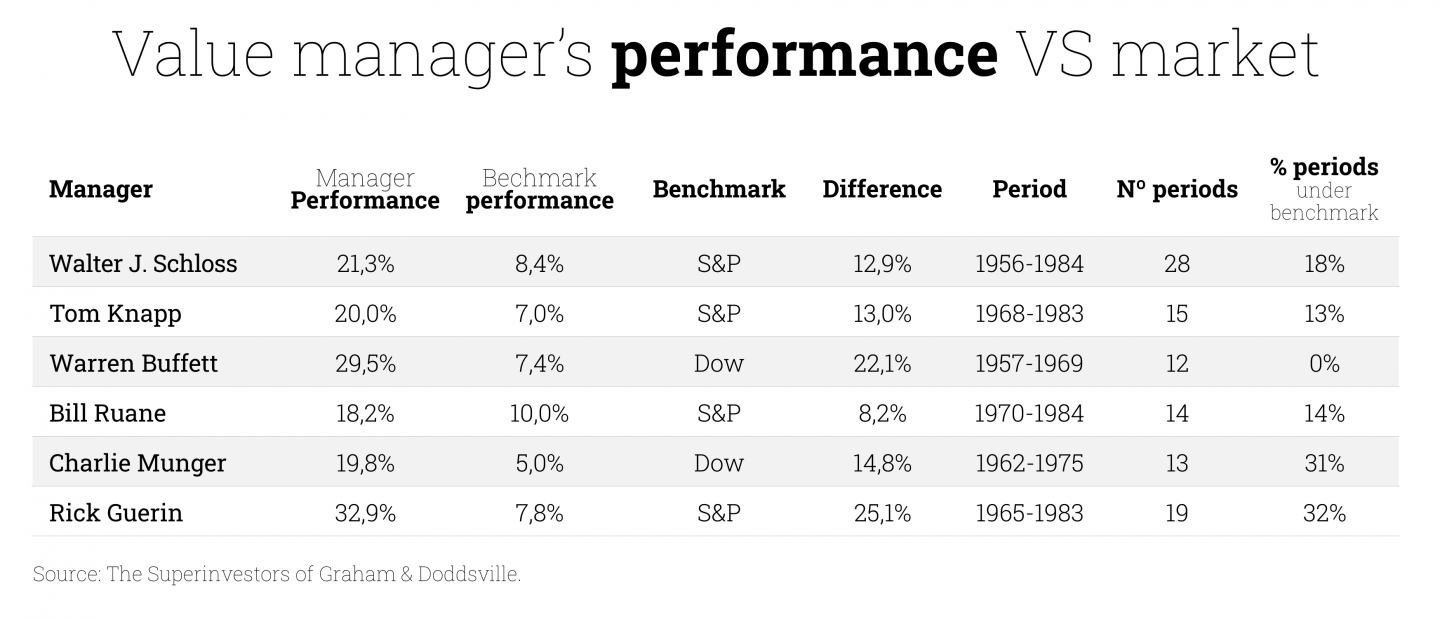

Returning to our commentary on the third quarter of 2019, in which we reviewed the performance of the international portfolio obtained by Francisco García Paramés and his team in all periods of 3, 5 and 10 years, we can draw two very valuable conclusions:

- The first is that about 20% of all 3-year periods the profitability was negative, approximately -15%. In these first three years of Cobas AM, we are in a similar situation.

- The second conclusion is that in all 10-year periods the profitability was positive, with the average profitability of those periods being over 150%. However, as you already know, past performance does not guarantee future returns. That is, history does not repeat itself. But with a carefully crafted and constant investment method, and a strictly-applied investment philosophy, it is normal for things to look very similar.

In the investment world, the best decision is generally not to make too many decisions. As you can see in the following chart prepared by Allianz Global Investors. It shows an inverse relationship between the degree of turnover of a portfolio and its results, which is down to both transaction costs and the difficulties of getting timings right.

In short, after three years, which have been difficult for all of us, we can say that the extent of knowledge regarding our investment ideas is much deeper, which is why our level of confidence for the future is growing. The cash flow generation we see in our businesses, along with the passage of time, is bringing us closer to the shore, as the market has not usually been volatile for very long, so we can assume that it won’t be in the future. All of this is possible, to a large degree, because of your attitude, which has a much greater bearing on long-term returns than many people might think.

Thank you very much for the confidence you show in us. You can be sure that with every day that passes, we are giving every last drop of sweat to repay it.

Did you find this useful?

- |