Investing against the tide is not easy, but we believe it is necessary.

Our investment philosophy pivots on the objective of finding businesses that, for one reason or another, have a stock market price that is lower than the core value of the business, which we ourselves try to estimate.

In other words, this objective implies investing in those places (industries, countries, etc.) where there is a lack of capital, places without sufficient attractiveness to, for a period of time, attract the attention and interest of the investment community, thus leaving room for opportunity.

This approach to investment, by its very definition, entails the need for two qualities that we believe to be essential: patience and optimism.

PATIENCE, which is necessary when one’s objective is to get to places before others do, because that will mean waiting for them. OPTIMISM, because when we try to get there first, we must implicitly assume that we will travel a path contrary to that of the majority, which will be more bearable if we face it with positivism.

These two qualities go into oneself, and serve as a foundation to develop a third, the one resulting from the valuation work that we carry out daily, CONVICTION.

With these premises, we are nearing the end of our first five years as a fund manager and, at this point in our history, I think it is a good time to stop and ask ourselves where we are and where we are heading, for which, over the following lines, I will try to explain the structure of our portfolios and the most important recent events that have taken place in their main positions, focusing on our International Portfolio, the basis on which our two main funds, Cobas Selección FI and Cobas Internacional FI, are built.

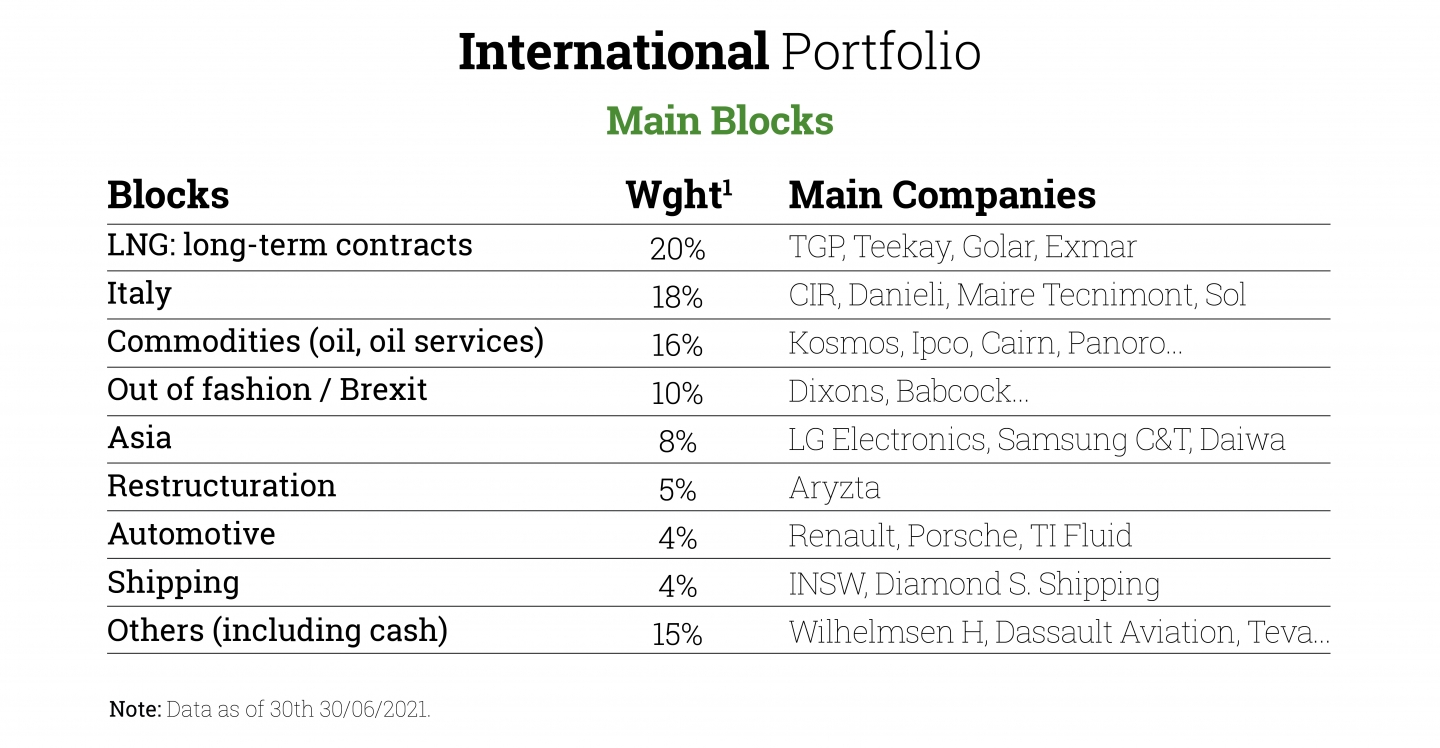

The following table shows the structure of the International Portfolio:

At a first glance, one first idea is clear: conviction.

Around 40% of the portfolio is exposed to two specific energy sources, and a further 30% is made up of businesses listed in two countries which, for various reasons (size of their market and political situation), are not at the centre of the market’s attention.

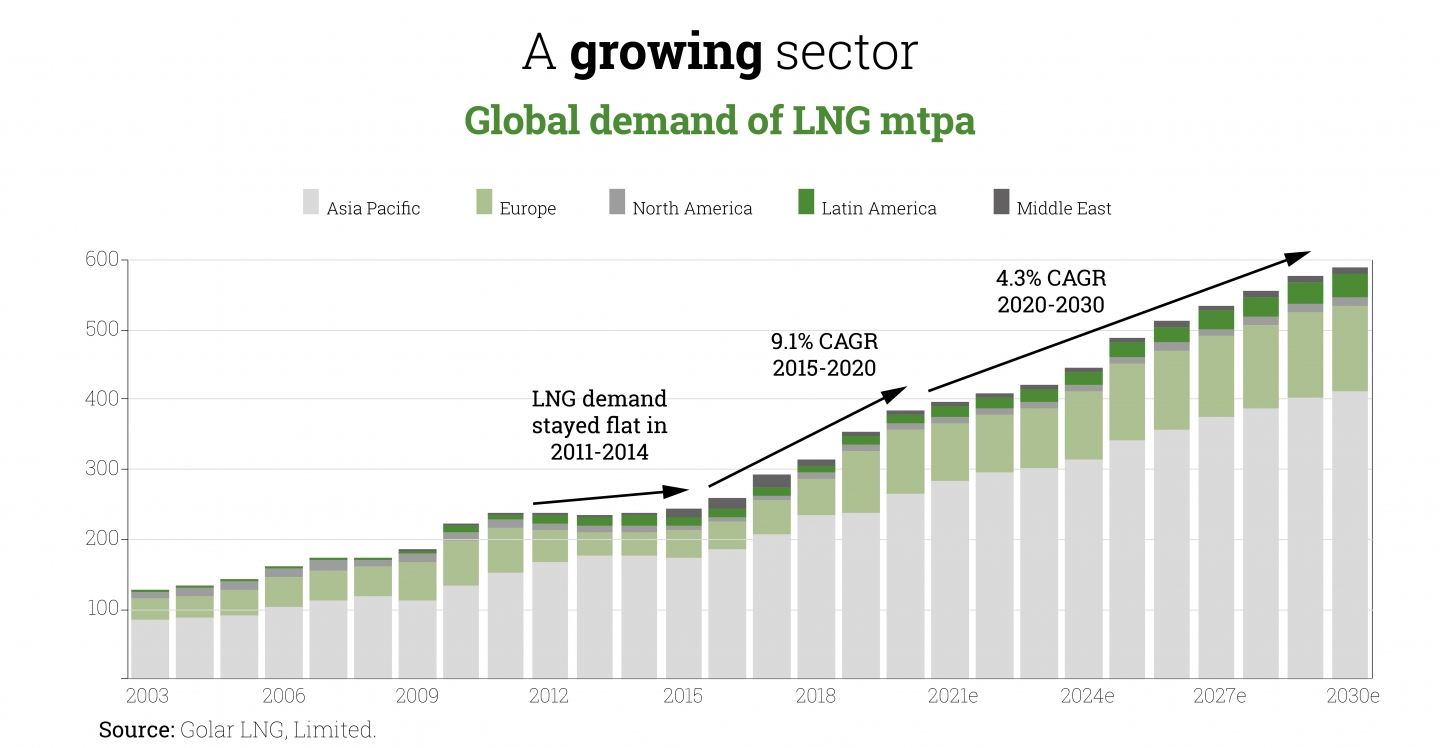

Let us start with natural gas, our largest exposure. Our general vision for this investment stems from thinking about the energy transition and, in particular, the role we believe gas will play in it as a transitional energy, especially given the strong demand prospects from Asia, the fact that it emits 30-40% less CO2 than oil or coal and that it is the main back-up for renewable energies.

The theory is materialised mainly through infrastructure investment, which we believe, in view of the demand outlook, will be capital-intensive in the coming years.

Our main investment is Golar LNG, a company that many will already be familiar with and which has been simplified following the sale of its gas import and distribution terminals business in Brazil. This sale has also helped to reduce the company’s financial risk.

Recently there has been a positive event related to its main business, the one that makes it stand out, that of floating liquefaction vessels or FLNGs, given that one of them, the Hilli Episeyo, has signed an agreement with its client (Perenco) to increase the vessel’s capacity utilisation, thus increasing its EBITDA generation.

Looking ahead, we believe that further simplification of its structure through a possible spin-off of its gas transportation division, and the pursuit of new projects in the liquefaction segment, would go a long way to closing the valuation gap that we currently believe exists. We are optimistic about that.

Our other major investment in the sector is the Teekay Group, to which we have exposure through its parent, Teekay Corporation, as well as one of its subsidiaries, Teekay LNG, which in turn accounts for the bulk of the valuation.

Teekay LNG (TGP) is the world’s largest LNG carrier. In an eminently cyclical segment such as gas transportation, TGP operates in a way that makes it stand out, and the thing is that most of its fleet is fixed through long-term contracts, with an average duration of around 13 years, which offers us a very interesting visibility of future flows.

Today the thesis is being executed flawlessly, with the company generating more and more cash flow, which is being allocated to debt reduction and shareholder distribution via dividend increases. In our view, the main catalyst here will be timing, as such cash generation will eventually push the share price upwards when the profitability of the business cannot go unnoticed by the market.

Let’s move on to oil, our other major sector exposure within the International Portfolio.

In a nutshell, our investment theory is based on the industry’s capital cycle, which we believe will evolve into a supply/demand mismatch once the world returns to full normalcy after the impact of COVID-19, given the low level of investment in capacity over the last few years. You can access a more thorough discussion of this theory by viewing our last quarterly commentary at the following link.

Perhaps the most relevant thing we are observing in this investment is the rebound in commodity prices (which it is reasonable to believe has its origin in the evolution of the capital cycle) which, so far and possibly due to the market’s rejection of oil and gas companies for sustainability reasons, has not been followed by prices to their fair share. We believe this will change.

This situation is allowing us to detect investment opportunities in the sector in companies with low risk, thanks to a healthy balance sheet, producers with low costs and good management teams, at multiples that we consider tremendously attractive as we are finding businesses with these characteristics at 3x-5x earnings, thus obtaining a very high safety margin.

As for the rest of the most relevant positions in the portfolio, the last few months have been positive and we are receiving good news that reinforces our conviction in them and allows us to be optimistic about what we believe is to come.

After the arrival of a new management team at the end of last year, Babcock has already carried out a contract and balance sheet review programme, resulting in a divestment programme of up to £400MM, which they have already completed in record time.

Italy’s CIR launched a voluntary takeover bid a few months ago with the aim of buying back up to 12% of outstanding shares. This was unequivocal proof that the Benedetti family, which owns the company, is also aware of the undervaluation of KOS, its main asset, which is gradually recovering from the strong impact of COVID-19 on its nursing home business in Italy and Germany.

As for Dixons, the theory has already reached one of its main milestones this year, which is putting an end to the negative impact of the mobile business, derived from the contracts it has held with the main British telecommunication providers in recent years. Without the cash outflows generated by this division, with the strong growth in online sales and the success of its omnichannel strategy, we believe that the theory is now fairly clear and we are very optimistic about the future.

At Aryzta, the theory has evolved very positively in recent quarters. On the one hand, the company’s entire management team has been replaced, giving the reins of the business to people with extensive experience in the industry who seem to be making good decisions. These include the divestments in the US and Brazil committed this year, which will help alleviate balance sheet tensions and allow us to focus our efforts on the organic recovery of the business in Europe, where we expect the progressive reopening of the companies to have a positive impact on the cash generation of the business.

This is good news that reinforces our work and encourages us to remain confident that, after a few difficult years in which the market has tested our patience and conviction, the best is yet to come and is ever closer.

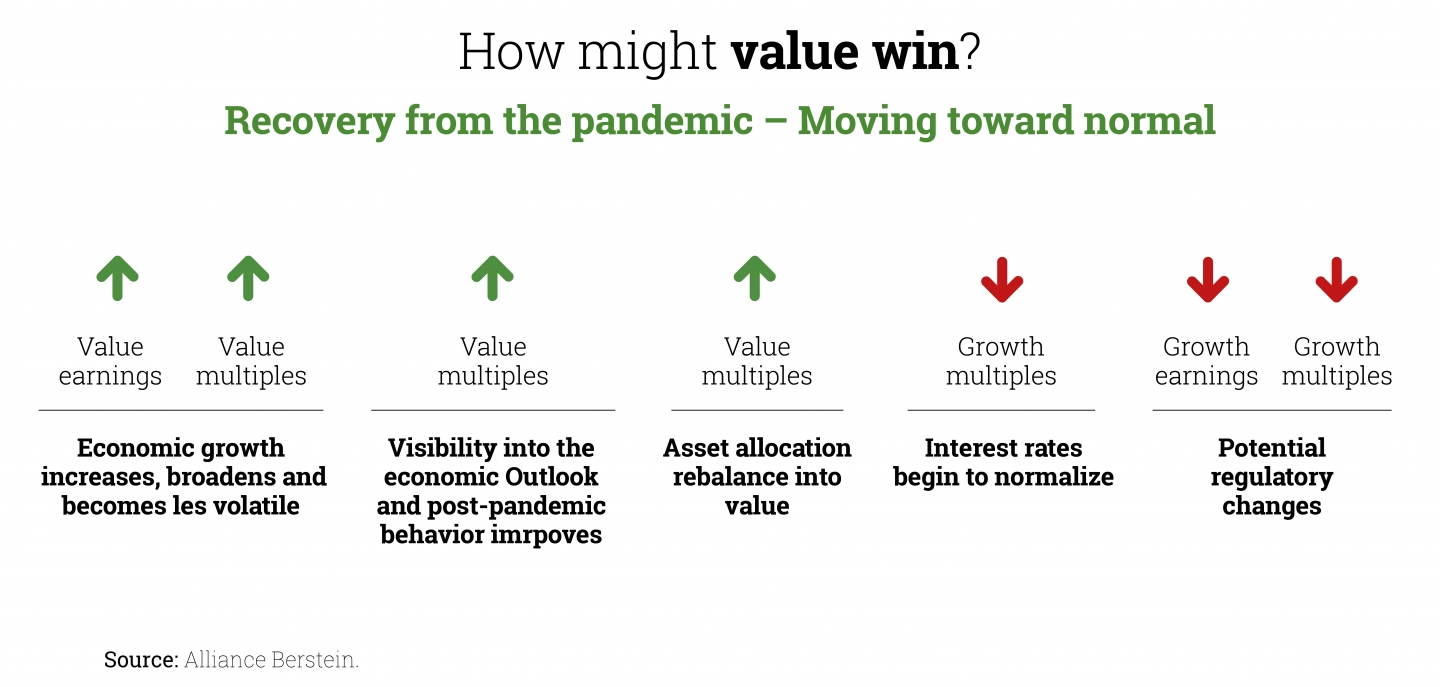

To this good news, we add the positive evolution of the global economic situation, which presents a number of situations that encourage us to believe that the recovery of value investing has begun.

All in all, our portfolios continue to trade at tremendously attractive multiples, with a P/E ratio at the end of August of around 7x estimated earnings for this year and target prices of close to €200/share, all with a Return on Capital Employed of close to 30%. In our opinion this ratio demonstrates that we have quality investments, despite the low valuation that the market has been giving them for some time now.

For all these reasons, we believe that we are facing an exciting moment that reminds us of what happened in the 2001-2003 period, which brings back such good memories in terms of profitability.

Did you find this useful?

- |