An ingenious lecturer of financial mathematics began his class by asking all the students the following question: “If, setting aside the mechanical difficulty, we folded a sheet of paper in half and with the folded sheet that we obtained we carefully folded it in half again and so on, until the operation is repeated, say, forty-two times, how thick would the resulting folded paper be? In other words, if we put one sheet on top of another, and two on top of those two, doubling the amount each time until we repeated this forty-two times, how high would the pile of paper that we would end up with be?

The answers were extremely varied and erratic: a handbreadth, a meter, twenty meters, the height of a building, among others. This helped the lecturer to show us in a practical way that the human mind is not prepared for exponential thinking. That is, when we have to string together calculation processes in which the conclusion or result of one is the basis of the following calculation (as in chess strategies), it is easy to get lost in anticipating a few short moves.

We find this same difficulty in financial planning when we want to focus on the long term. This is what happens, for example, when a young person wants to plan their retirement and does not have the necessary calculation tools. Thus, we usually encounter heated debates about the different pension options and, in particular, about the tax advantages (or not) of pension plans.

Doubts arise as to whether it is better to be taxed on work income (pension funds) or on capital increase (investment funds). On forms and date of redemption (as capital or as income). On the different impact depending on the return obtained (the entire redemption amount is taxed in the pension fund, while only the surplus obtained is taxed in investment funds) and even on the legal certainty and foreseeable stability of the tax rules that regulate one form of investment or another.

In my opinion, the only way to do the analysis is to establish clear and simple assumptions with homogeneous conditions for both types of investment (which allows comparison), accurately model the tax effects for investment funds and pension funds and analyze different scenarios.

Clear and simple assumptions

First, if we are going to compare two vehicles to see which one has a tax advantage over the other, the rest of the conditions must be the same. Thus, we are going to compare the investment in an investment fund and in a pension fund, assuming that in both cases the portfolio, management and fees are exactly the same, i.e. the financial result of the investment is the same.

Secondly, if we are going to make an analysis to study the best way to save as a forecast (to complement our public pension, for example) we will have to assume an investment with the characteristics of the forecast savings, which are basically:

- Very long-term savings.

- Periodic investment, both in the accumulation period (active worker stage) and in the redemption period (when the saved capital is consumed in retirement). That is, we save by means of an annual contribution and upon retirement, we receive the savings through an annual income.

- Finally, to clearly see the effects, let’s set a sufficiently long period: 30 years of accumulation and another 30 years of redemption (it would be, in our hypothesis, the case of a worker who begins to save at 31, works until 60 and from 61 enjoys an annual income up to 90 years of age).

Modeling of tax effects:

- The investment fund is taxed on capital increase at rates ranging from 19% for the first tranche to levels of 21% or 23% in higher tranches. It is taxed at the time of reimbursement as per FIFO criteria (paid on the oldest capital gains at the time of reimbursement).

- The pension fund is taxed when it is redeemed (for the amount drawn), as work income that is integrated into the individual’s annual taxable income, being taxed at the resulting statutory income tax rate.

- The tax advantage of the pension fund is that when making the contribution (with an annual limit of the smallest amount between 8,000 euros and 30% of the net income of the taxpayer’s work and economic activities) this contribution is deducted from the taxable income, so the net effect is a reimbursement on personal income tax (or lower amount to be paid) equivalent to the marginal rate (i.e. with a marginal income tax rate of 40%, after a contribution of 8,000 euros to the pension plan, a reimbursement on personal income tax of 3,200 euros is obtained).

Homogenization of both investments:

- In both products, we will assume the same annual net contribution and the same annual net redemption, which, with the same return and fees, will allow us to attribute the different evolution in the accumulated equity, to the different taxation.

- To assume the same annual net contribution, it must be taken into account that in the pension fund there is a reimbursement on personal income tax on the gross contribution (in our example 8,000 euros) which implies a lower net contribution, which is the one used for the comparison (following the example, if the return is 3,200 euros the net contribution to the pension plan is 4,800 euros, even though 8,000 euros are actually invested in the plan)

With these assumptions we can analyze different scenarios:

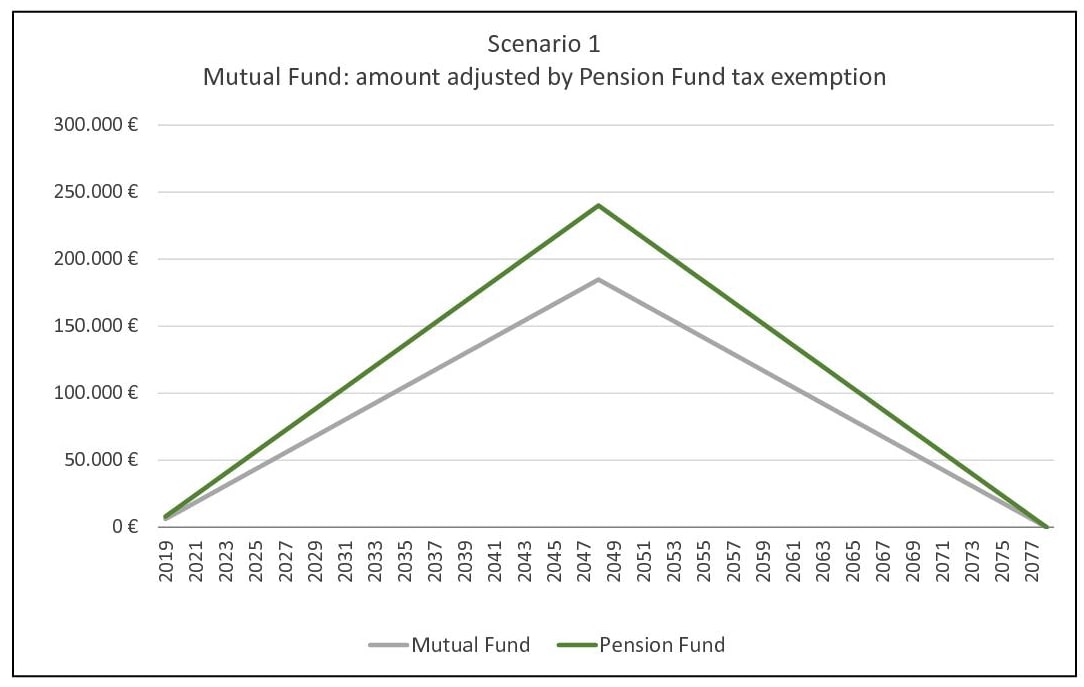

Scenario 1:

- The return throughout the entire investment is 0%.

The marginal rate in personal income tax in the contribution is 23% and in the redemption also 23%.

In this scenario we clearly see the effect of taxation: the initial tax advantage of the pension plan is lost if there is no return and if the redemption is at the same marginal rate of personal income tax as the one that was had when the contributions were made.

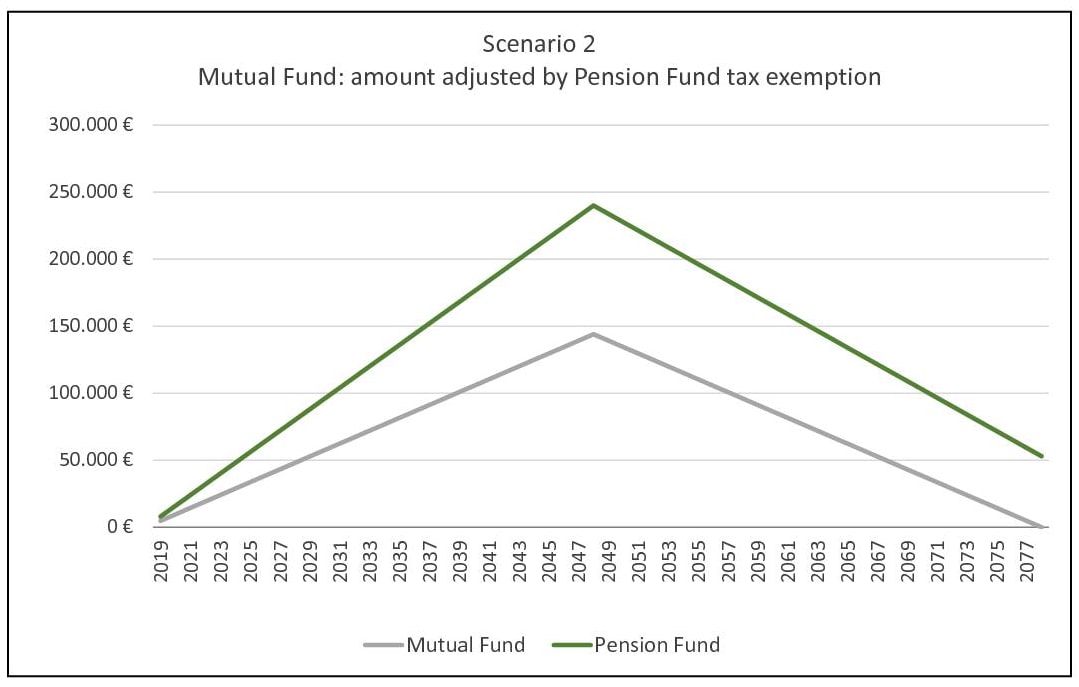

Scenario 2:

The same, 0% return, but with a greater marginal rate of personal income tax in the accumulation stage (40%) than in the redemption phase (23%):

Here we can already clearly see that, even if we did not have a return on investment, we would be interested in the pension fund because we improve our total taxation (as a result of the fact that what we stop paying 40%, then pay, during retirement, 23%).

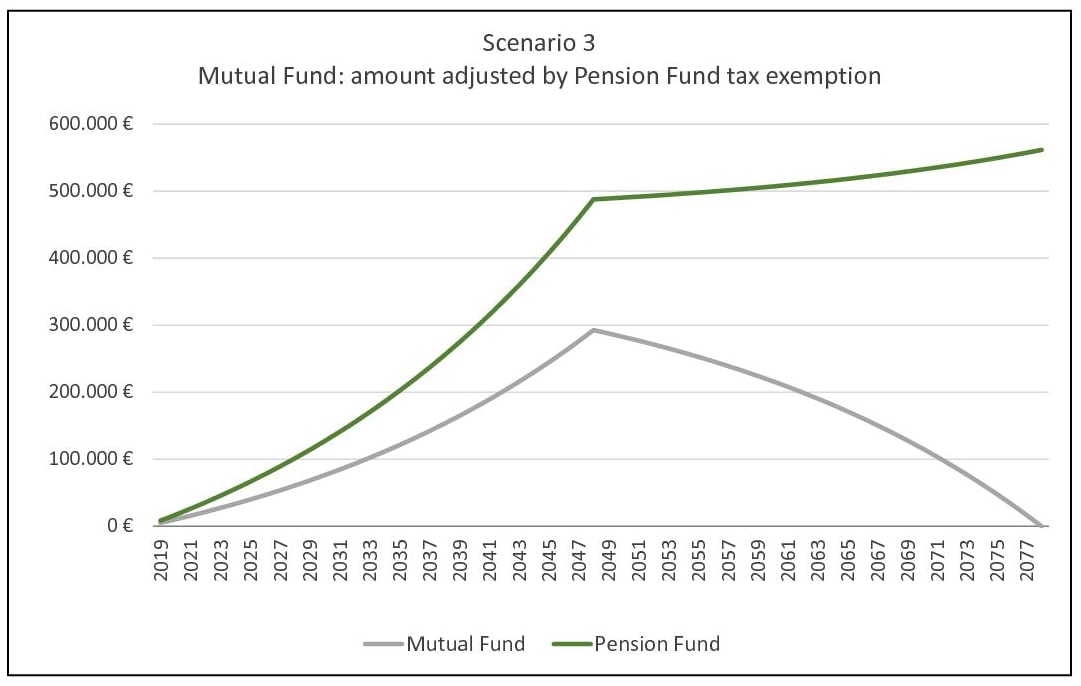

Scenario 3:

Finally, we can take our analysis to a more realistic scenario, in which the investment had a net return (during the 30 years of accumulation and 30 years of redemption) of 4.25% per year:

In this example, with a marginal rate of personal income tax on the contribution (while being active and having a salary) of 40% and an average rate of personal income tax in redemption (during retirement) of 23%, assuming a gross annual contribution of 8,000 euros per year and an annual net repayment or redemption of 14,395 euros per year, in the Investment Fund (grey line), we would consume the accumulated capital after 30 years of reimbursements, while in the pension fund (green line), due to the capitalization of tax savings, the remaining amount would increase until an additional €560,000 is accumulated after 30 years of annual redemptions.

This is the reason why, in my opinion, it is absolutely advisable, when saving in the long term and as aforethought, to consume all the tax advantage that allows us to contribute to a pension fund.

In the analysis shown, we clearly see the enormous tax advantage of pension funds, as well as the magic, so often commented here, of compound capitalization in long-term investment.

And, by the way, speaking of compound interest, the answer to the initial question of the ingenious lecturer, assuming that each sheet is one-tenth of a millimeter thick, is that the pile of paper would have a height of about 430,000 kilometers, more or less the distance from Earth to the Moon.

Did you find this useful?

- |