A road, inspiring landscapes, the window open and your hand outside waving in the wind enjoying the air that you can feel caressing your skin. Do you like driving?

In the minds of all of us, we can still remember the incredible landscapes, the tranquillity and the feeling of freedom that the famous BMW commercial gave off. Who didn’t feel like driving after seeing that ad? The impact was such that it was launched in Spain 22 years ago and I dare say we are all able to remember it. At the time of the ad’s premiere I was nine years old and I still remember rolling down the window and sticking my arm out the window to wave it. I too wanted to experience that feeling of freedom that BMW offered, even if it was on the way to school in a Chrysler Voyager with my brothers, and my mother yelling at me to reach inside the car and roll up the window.

If you watch the ad again, you can see that there is no mention of price, performance or even the car model. That year in Spain, BMW sales increased by 11.4% and turnover by 20.6%.

We all also remember how Red Bull managed to glue us to the TV to watch Felix Baumgartner (I don’t think any of us knew he existed until then), jump from the stratosphere to become the first human to break the sound barrier without the impulse of an engine. The campaign went viral, quadrupling the number of subscribers to its YouTube channel before the jump, with the consequent global brand impact. In the six months following the jump, the brand increased sales by 7% in the United States.

Did Felix Baumgartner’s jump make Red Bull taste better or finally give you wings? Did BMWs improve their performance and make better cars by filming a hand outside the window in awe-inspiring landscapes? I think the answer is obvious: a resounding no. Both are two illustrative examples of the great power that emotions can have in our decision-making process.

We go through life thinking that we are infallible and all our decisions are fully rational. The confidence we have in the rationality of human beings is such that even one of the premises of the neoclassical school of economics rests on the “homo economicus”, that is, supermen who are guided solely by reason and maximising utility in their decision-making process.

I have used the examples of the two advertising campaigns because they are able to translate into numbers how appealing to our emotions can condition our decision making, but the examples are endless: How most of us vote in elections, our football team, the anchor effect on prices, or simply ask a newlywed couple what the probability is that they will end up divorced; they will tell you it is zero. Statistics show that the divorce rate has been over 50% for the last seven years.

Acting rationally implies acting in accordance with reality, interpreting objective facts. Emotion tells us nothing about reality, it is a value judgement that we form automatically. This is not to say that emotions are useless. On the contrary, emotions are a vitally important element in our lives: They push us to act, to think, to make decisions for our survival in a matter of seconds, they allow us to recognise our biological needs, and so on. In fact, it is not only reason that differentiates us from other living beings, but also our complex emotional circuits.

This does not prevent them from being counterproductive in certain situations, such as in investment decisions. More than that, if we analyse the decision-making in our investment process we can conclude that we tend to make very bad decisions. A clear example is the famous Fidelity Magellan managed by Peter Lynch. The annualised return between 1977 and 1990 of 29%, one of the best in history, and yet the average investor lost money!

One reason may be that investment often generates negative emotions such as loss aversion. It has been shown that the pain of losing an amount is twice as great as the pleasure of gaining the same amount. If we take into account that negative emotions are the ones that separate us the most from a rational thought process and therefore lead us to be more impulsive, it is understandable that we are bad at making investment decisions.

So how can we avoid unconsciously falling into emotional impulses in our investment decisions? One of the keys is to create a frame of reference that allows us to fight against ourselves. Adhere to a set of key principles to ensure that our investment decisions are sound and therefore achieve the desired objective: they have to fulfil the purpose we had when we made them.

At Cobas AM, one of our main objectives is to try to promote and share some principles that help to avoid falling into those investment mistakes that often lead to our investments not meeting expectations. Here are some of them:

- Enhancing knowledge: Increase our knowledge of investment and how markets work. Knowledge is one of the strongest tools for controlling our emotions.

- Equity volatility: Equity investment is the best option over long periods of time in terms of returns. In the short term, however, the swings can be huge. If you decide to invest in equities, you have to ask yourself, am I going to be able to withstand the periods of sharp falls that will come sooner or later? If the answer is yes. Go ahead, you are ready to tackle equity investing.

- Long-term orientation: This point is fundamental and closely related to the previous one. The market is irrational in the short term, but not over long periods of time. If you have a long-term time horizon, you can benefit from the returns that equities provide over time.

- Confidence: Right now there are hundreds of thousands of investment options. The emergence of passive management has become a very good option for investing in equities, as its costs are lower and it beats most active managers. Therefore, if you know and trust an active manager who improves market performance over the long term, active management may be a good option. Otherwise, you can opt for passive management.

The current situation we are experiencing is a reflection of this struggle between emotion and reason. As we know, we are coming from a time when there has been the greatest divergence between value investing and growth investing, in terms of returns, in the last sixty years. Not only that, it has been the largest divergence in terms of profitability, but also in terms of duration. Never in the last sixty years has there been such a prolonged period of time when value has done worse. Given this, it is normal that our emotions begin to manifest themselves and we begin to ask ourselves, is value investing finished? Is it a good idea to sell and redirect my investment?

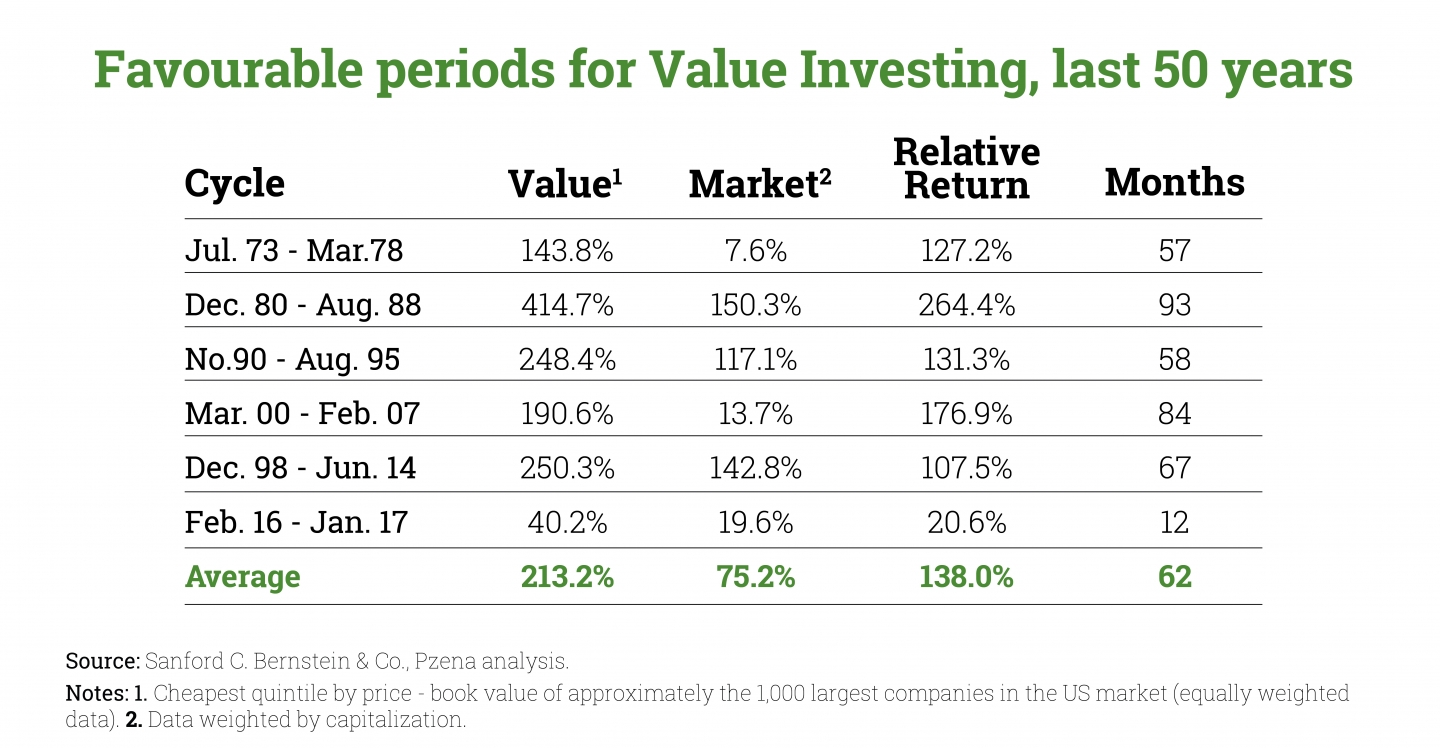

Our irrational self inevitably speaks to us. The important thing is to be able to use tools that help us to fight it, to rationalise the emotion. As I mentioned earlier, one of the tools in the face of irrationality is knowledge. The following table analyses all periods favourable to value investing over the last fifty years:

As we can see from the last line, these periods are characterised by far better aggregate market data. Moreover, the average length of time over which value investing does best is almost five years. This table with data allows us to put the current situation into perspective, with the market’s own oscillations (worse relative performance of the investment in value compared to the market) and to see that in the long term we will obtain the desired profitability. On this last point, we can see that in the last year value investing has regained traction, and while with markets you never know, there seem to be tailwinds in favour of this investment philosophy.

This adverse performance situation for value investing in terms of returns has also become a window for our investment team to build a portfolio that allows us to look to the future with optimism. Our investment team also needs to insulate itself from market noise and these irrational impulses. A clear investment methodology and philosophy (investing in quality businesses, with barriers to entry, with controlled net cash or debt and trading at a discount) has enabled them to meet the challenges as they arise, and to beat the market over a 30-year period.

Emotions are inherent to human beings and more than that, they are essential for our development and survival; however, in my opinion, it is important that in certain relevant aspects of our lives we do an exercise of introspection and confront emotion with reason. It is inevitable that in many aspects of our lives we drink Red Bull just in case we might sprout wings at some point. But in the case of our investment decisions, and now more than ever (I would like to take this opportunity to recommend the great documentary on the pension issue “Ni es Justicia, Ni es Social” produced by Value School, which you can find on its Youtube channel), how we manage our savings will determine to a large extent our purchasing power, our quality of life in old age or meeting the objective we have with that investment. I think these aspirations are more than enough to try to use whatever tools one has at one’s disposal, and to try to separate and clarify with them the blurred line that separates reason from emotion.

Did you find this useful?

- |