The performance of value investing over the last three years has recorded one of its worst periods in decades, but this is not the first time that value investing has had a rough couple of years, in fact, it has been somewhat of a recurring theme since the beginning of the 21st century.

If we go back to the origins of this value bubble, we can see that between 2008 and 2019 there was a huge distortion in prices between value assets and growth assets.

There are multiple reasons to explain this disparity in results. Evidently, the monetary policy implemented by the central banks and low interest rates are not conducive to good capital allocation on the securities market. This growth in credit leads to an indiscriminate inflow of equity resources, without taking into account the valuation of the companies.

Furthermore, the increased investment through ETFs and the disproportionate weight in FAANG stocks have caused the valuation differentials to become increasingly larger and last many years. Trends are very dangerous because markets tend to overreact.

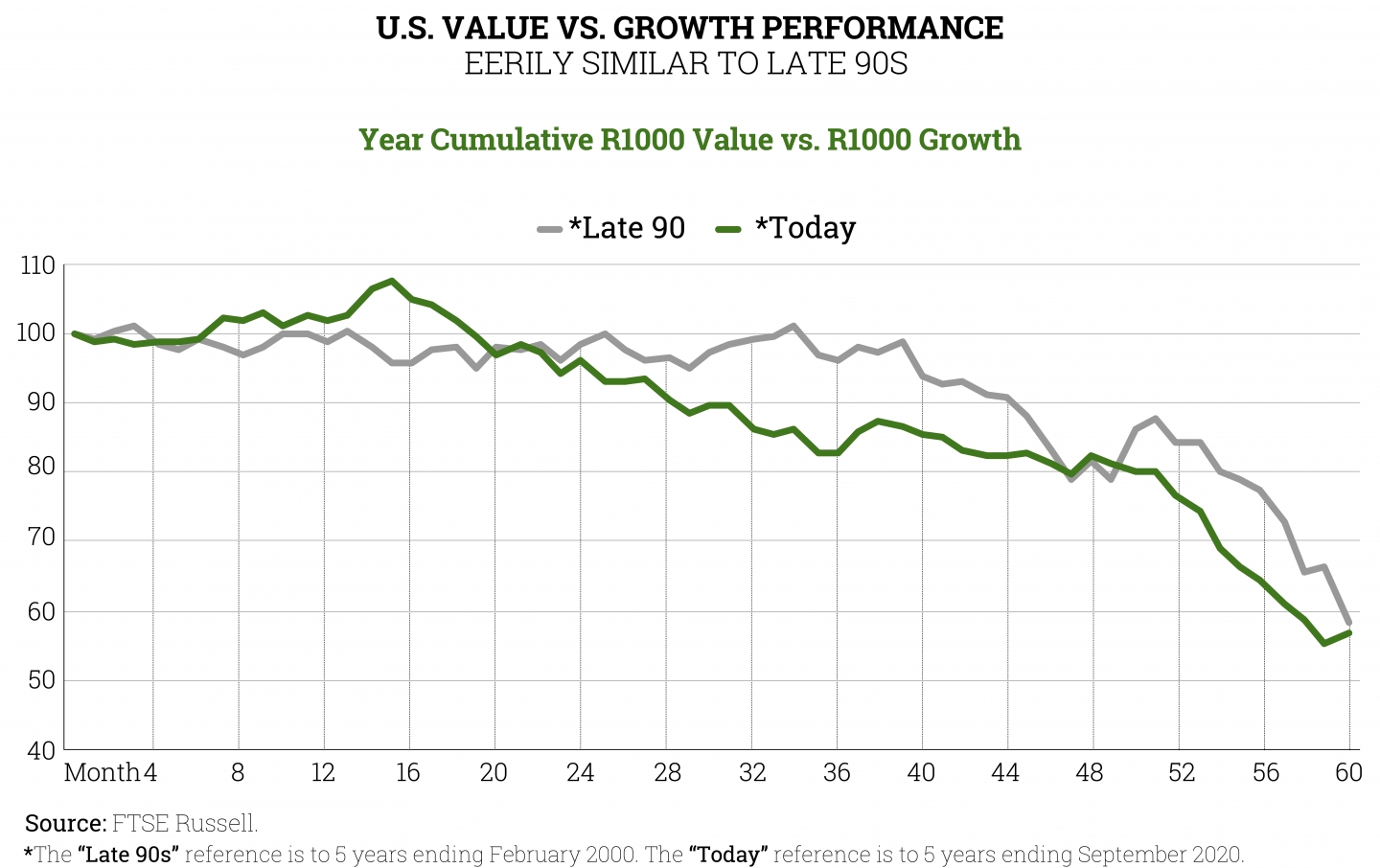

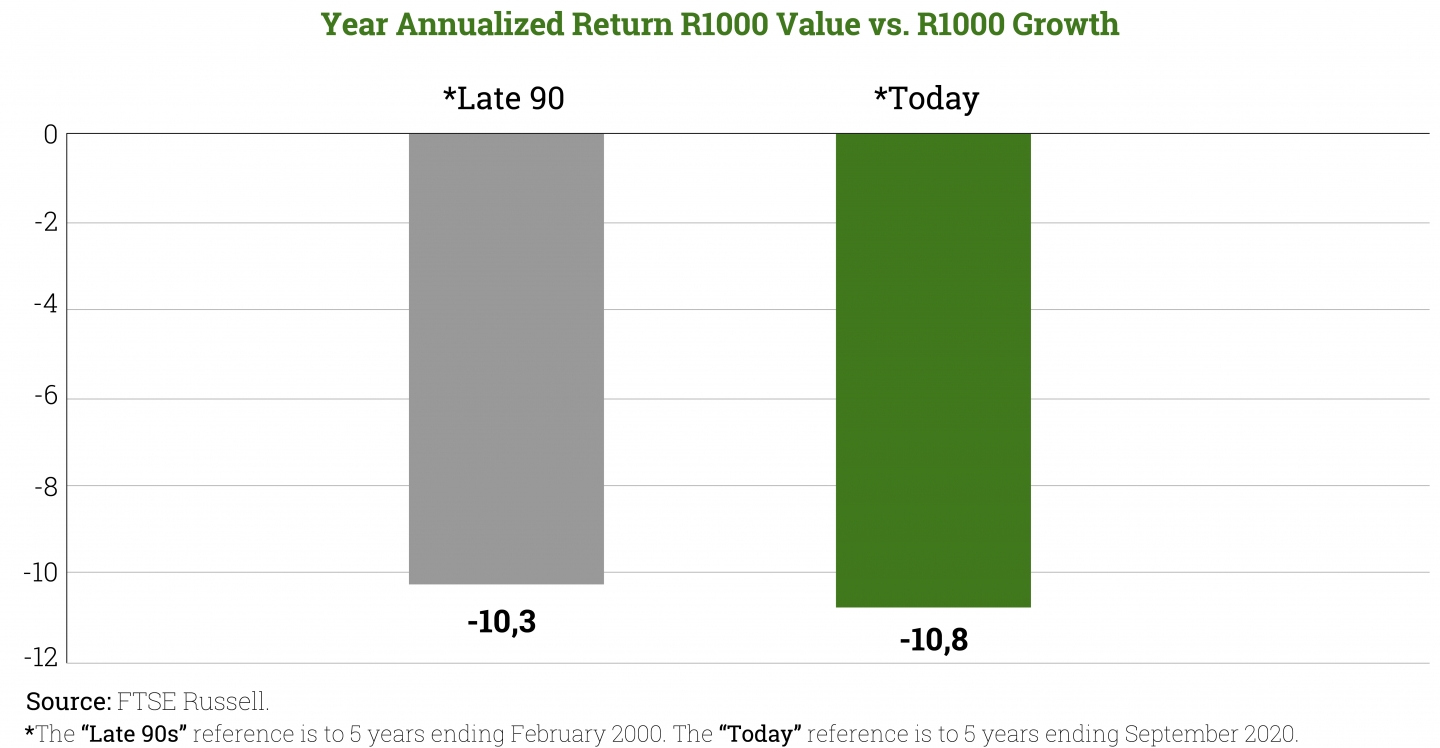

Luckily, or unluckily, this is not the first time we have had a situation like this. Towards the end of the 90s, value investing experienced a similar scenario and was left behind compared to growth securities for more than a decade. When it seemed that value investing had died, the mean reversion worked and value investing exceeded growth for more than 7 consecutive years. In spite of the initial uncertainty, investors were rewarded for their perseverance and between 1999 and 2006 achieved an accumulated growth of 99%.

So, if we have a look back, it appears that we have a scenario that is similar to that of 1999 and therefore, history could repeat itself.

Looking at the charts, we could ask ourselves whether what happened during the dotcom crisis could repeat itself. If that’s the case, are we looking at change in trend?

Well, it seems that value investing’s time has now arrived.

What is certain is that the data indicates that this could be one of the best moments for value investing based strategies.

Since November 2020, with the announcement of the Covid-19 vaccines, and the outlook regarding the end of the pandemic, we have observed a reversal of the trend, and the value portfolios are outstripping the performance of all other strategies. This means a strong rotation of assets in the market, favouring risk assets which have suffered the most since the beginning of the pandemic.

Investor confidence that there will be a recovery is driving the purchase of companies based on their fundamentals and the forecast global growth of 5% confirms that this trend we have been witnessing since November 2020 could continue to generate revaluations in line with the growth in earnings per share.

Furthermore, it was expected that the value differential between value companies and growth companies would narrow, because as we have witnessed in recent years, this was at a record high.

In relation to the above, since the beginning of the year we have been seeing how many of these growth companies are beginning to not meet expectations, whereas value companies are obtaining profits that are even into double digits. It is not absurd to think that many of these companies, which have been the most penalised, might continue with this substantiated rally.

Furthermore, there is the expectation of interest rate hikes once again harming growth companies because investors value them depending on their forecast future earnings and high interest rates would damage the value of these future earnings more than the value of the short-term earnings obtained.

It would appear that value investors have had a great start to the year, with February being the best month since March 2001, when the market was still recovering from the impact of the dotcom crisis. This trend is also continuing this month, but let’s not celebrate just yet, we are aware that there is still a long road ahead of us and we need an extraordinarily good year for value investing to recover all the ground it has lost.

At Cobas AM, we are convinced of the potential of our portfolios and that we are doubtlessly well-positioned for the market’s new direction.

Did you find this useful?

- |